Showing posts with label Macro Demystified. Show all posts

Friday, January 28, 2022

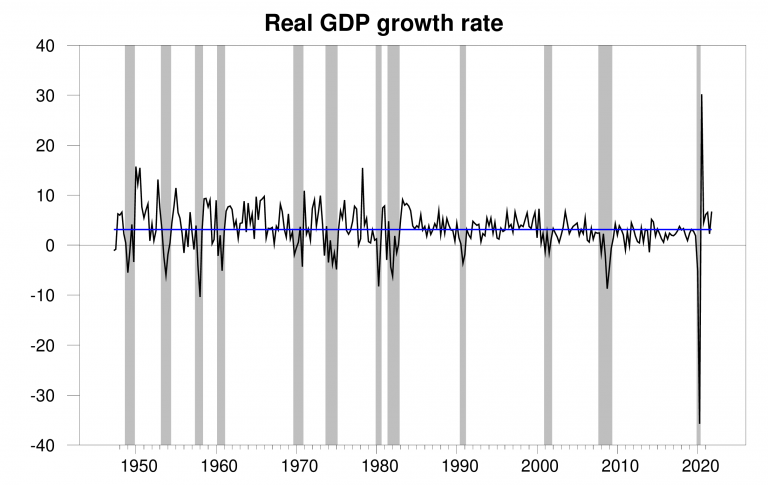

GDP almost back to potential

From Econbrowser:

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP grew at a 6.9% annual rate in the fourth quarter, more than twice the average growth rate the U.S. has seen since World War II.

The new data put the Econbrowser recession indicator index at 1.2%, historically a very low value and signalling an unambiguous continuation of the economic expansion. The number posted today (1.2%) is an assessment of the situation of the economy in the previous quarter (namely 2021:Q3). We use the one-quarter lag to allow for data revisions and to gain better precision. This index provides the basis for an automatic procedure that we have been implementing for 15 years for assigning dates for the first and last quarters of economic recessions. As we announced a year ago, the COVID recession ended in the second quarter of 2020. The NBER Business Cycle Dating Committee subsequently made the same announcement in July.

Continue reading here.

From Econbrowser:

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP grew at a 6.9% annual rate in the fourth quarter, more than twice the average growth rate the U.S. has seen since World War II.

The new data put the Econbrowser recession indicator index at 1.2%, historically a very low value and signalling an unambiguous continuation of the economic expansion.

Posted by at 12:13 PM

Labels: Macro Demystified

Thursday, January 27, 2022

African history through the lens of economics

From a VoxEU post by Nathan Nunn, Stelios Michalopoulos, Elias Papaioannou, and Léonard Wantchékon:

“Since the 2000s, a vibrant stream of research on African political economy and economic history has emerged that has produced a plethora of insights and has uncovered the shadow that Africa’s past casts on contemporary economic, social, and political development. This column introduces a free online course on “African History through the Lens of Economics”, which will bring together the considerable volume of work in the economics literature of the past decades. The course is open to students with a background and interest in economics, political science, history, cultural anthropology, and psychology.

Views about Africa are, were, and most likely will continue to be highly polarising. Some economists, finance professionals, multinational executives, global entrepreneurs, and businesspeople are bullish, as there are investment opportunities in infrastructure, manufacturing, and technology, coupled with a young population that is increasingly more educated and confident. However, many are less optimistic, concerned about misgovernance, conflict, weak state capacity, corruption and poor infrastructure. Pessimists point to Africa’s dark past, including the atrocities and exploitation during colonisation, and the slave trades.

In 2000, The Economist called Africa “the hopeless continent”. A decade later, after strong growth and institutional advancement, it renamed it “the hopeful continent”. A few years later, in 2016, the magazine described it in more nuanced terms as a land of “1.2 billion opportunities” – a reference to the potential market that its huge population constituted. Economics research has followed a similar train. In the 1970s, 1980s, and 1990s, only a handful of papers were published outside specialised outlets. But, since the 2000s, a vibrant stream of research on African political economy and economic history has emerged. The new economic history approach departs greatly from prevailing thinking in important ways.

First, scholars realised that ill-conceived, post-independence urban-rural agriculture and trade policies, authoritarianism, conflict, corruption, and lack of structural transformation (the foci of pre-2000 studies) often had deep roots stemming from colonial extraction, enslavement, the artificial design of country borders, underinvestment, and cash-crop specialisation during colonisation.

Second, the new economics research became more interdisciplinary. For example, applied research started scrutinising influential ideas proposed by historians, political scientists, sociologists, and even cultural anthropologists.

Third, the studies began moving beyond purely economic outcomes and drivers of development. They examined, for example, the origins and the implications of the vast differences in social capital, civicism, cultural preferences, and values. This more evolutionary approach to economic history has led to a fruitful dialogue between economics and the other social sciences; albeit one not without tension.”

From a VoxEU post by Nathan Nunn, Stelios Michalopoulos, Elias Papaioannou, and Léonard Wantchékon:

“Since the 2000s, a vibrant stream of research on African political economy and economic history has emerged that has produced a plethora of insights and has uncovered the shadow that Africa’s past casts on contemporary economic, social, and political development. This column introduces a free online course on “African History through the Lens of Economics”,

Posted by at 10:54 AM

Labels: Macro Demystified

Monday, January 24, 2022

Data Sources Compendium [Updated]

From Econbrowser:

“Update of The Data Will Set You Free (in preparation for a new semester!)

In an era of easily accessible databases, am constantly amazed that people write stuff that is easily falsifiable. Or ask me for the “raw” data when it’s freely available via a aggregating database I’ve provided the hyperlink (most galling is when they then accuse me of misquoting data sources).

Just to remind the frequent commenters on this blog, freely available and documented data available here:

St. Louis Fed economic database Thousands of time series on economic activity, in an easily downloadable form.

IMF International Financial Statistics

IMF World Economic Outlook databases.

World Bank World Development Indicators.

DBnomics (a “European FRED”)

YCharts Macro and equity market data series.

ino.com Futures data.

Federal Reserve Board data Monetary, financial and output data collected by the Nation’s central bank.

Bureau of Economic Analysis, Dept. of Commerce Data on GDP and components (the national income and product accounts) as well as other macroeconomic data.

Bureau of the Census, Dept. of Commerce Data on the characteristics of the US population US firms, as well as other data.

Bureau of Labor Statistics, Dept. of Labor Data on wages, prices, productivity, and employment and unemployment rates.

Energy Information Agency, Dept. of Energy Data on energy (electricity, gas, petroleum) production, consumption and prices.

Economic Report of the President, various years. The back portion of this annual publication contains about 70 tables of government economic data.

Economic Indicators CEA and JEC Compilation of economic data in tabular form.

Economic Time Series page A large collection of economic time series.

NBER Data Specialized economic databases created by economists associated with the National Bureau of Economic Research.

Netherlands Bureau for Economic Policy Analysis World Trade Monitor

World Bank, A Global Database of Inflation.

Jordà-Schularick-Taylor Macrohistory Database

Usually I cite FRED or BEA and/or BLS via FRED, or from the above data sources. In certain cases, I have written papers using specialized data sources. Below are links to those data sources.”

Continue reading here.

From Econbrowser:

“Update of The Data Will Set You Free (in preparation for a new semester!)

In an era of easily accessible databases, am constantly amazed that people write stuff that is easily falsifiable. Or ask me for the “raw” data when it’s freely available via a aggregating database I’ve provided the hyperlink (most galling is when they then accuse me of misquoting data sources).

Posted by at 7:07 AM

Labels: Macro Demystified

Saturday, January 22, 2022

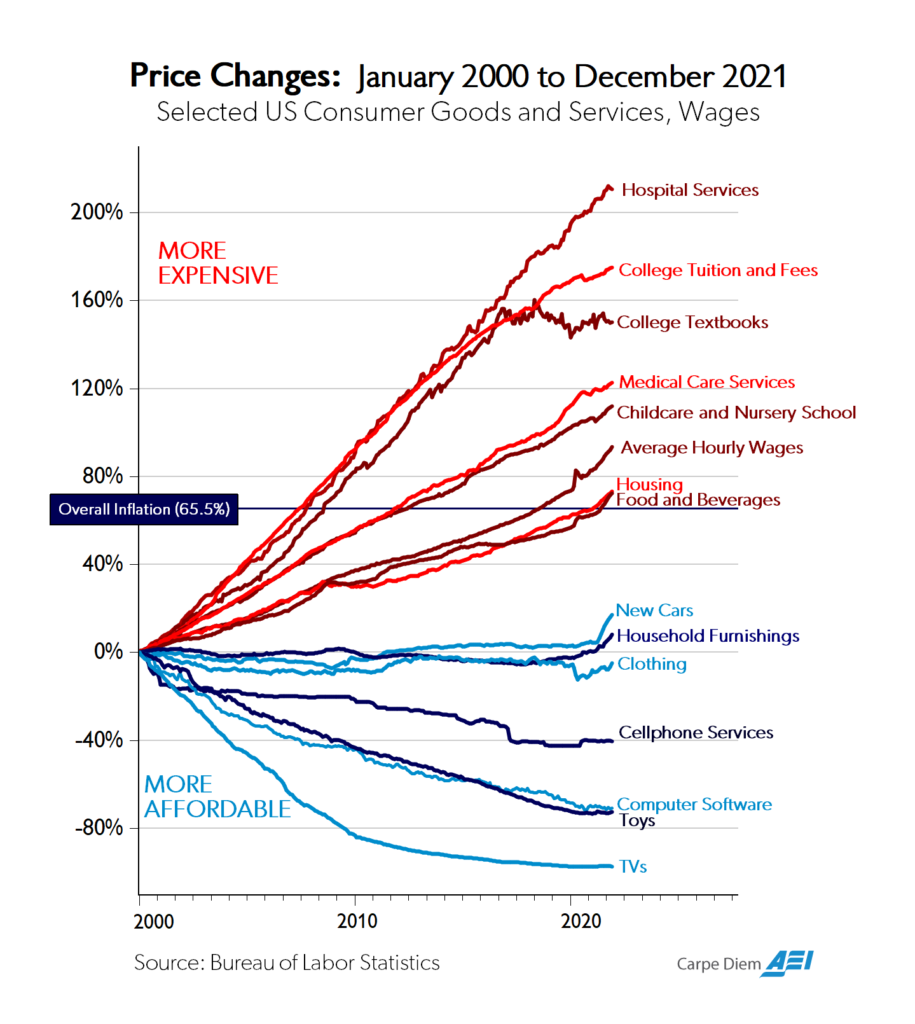

Chart of the day…. or century?

From Mark J. Perry (AEI):

“As I wrote in the summer of 2018 on CD, I’ve probably created and posted more than 3,000 graphics on CD, Twitter, and Facebook including charts, graphs, tables, figures, maps, and Venn diagrams over the last 16 years. Of all of those graphics, I don’t think any has gotten more attention, links, re-Tweets, re-posts, and mentions than previous versions of the chart above, which was once referred to as “the Chart of the Century.” Here are some examples of the attention that past versions of the chart above have gotten:

*Marketwatch has featured the chart twice here and here and made this comment “When this chart’s creator, econ professor Mark Perry and the man behind the Carpe Diem blog, first posted it on Twitter, it was hailed as “stunning” and “one of the most important charts about the economy this century.“

*Barry Ritholz has featured various versions of the chart three times on his Big Picture Blog here, here, and here.

*Bloomberg published an article in July 2018 titled “Chart of Century Gives Powell Gloomy Glimpse of Trade-War World,” with this opening:

A multi-colored graphic that’s made the rounds at the Federal Reserve hints at what Chairman Jerome Powell could face if President Donald Trump succeeds in throwing globalization into reverse: Higher prices for many goods and potentially faster inflation.

Plugged as possibly the chart of the century by economist and originator Mark Perry, it shows that prices of goods subject to foreign competition — think toys and television sets — have tumbled over the past two decades as trade barriers have come down around the world. Prices of so-called non-tradeables — hospital stays and college tuition, to name two — have surged.”

From Mark J. Perry (AEI):

“As I wrote in the summer of 2018 on CD, I’ve probably created and posted more than 3,000 graphics on CD, Twitter, and Facebook including charts, graphs, tables, figures, maps, and Venn diagrams over the last 16 years. Of all of those graphics, I don’t think any has gotten more attention, links, re-Tweets, re-posts, and mentions than previous versions of the chart above, which was once referred to as “the Chart of the Century.” Here are some examples of the attention that past versions of the chart above have gotten:

*Marketwatch has featured the chart twice here and here and made this comment “When this chart’s creator,

Posted by at 1:09 PM

Labels: Macro Demystified

Modelling Okun’s Law – Does non-Gaussianity Matter?

From a paper by Tamás Kiss, Hoang Nguyen and Pär Österholm:

“In this paper, we have analysed the relevance of taking non-Gaussianity into account when empirically modelling Okun’s law in Australia, the euro area, the United Kingdom and the United States. Our results based on Bayesian VAR models with stochastic volatility suggest that heavier-than-Gaussian tails find support in some cases. Taking skewness into account is, however, less beneficial in this context considering our baseline sample. Our results confirm that it is important to account for heavy tails in the distribution of macroeconomic variables, an argument put forward by Fagiolo et al. (2008) and Ascari et al. (2015) among others.

It should be noted though that our results to some extent depend on whether data from the corona pandemic are included or not. We believe that including them might be problematic since they should probably be treated as outliers (see the discussion in Carriero et al., 2021). If they nevertheless are treated as regular observations, our analysis indicates that the evidence of non-Gaussianity strengthens. In addition, it can be noted that accounting for non-Gaussianity not only improves the model fit in several cases but it also captures the large swings in the variables without causing large swings in the stochastic volatility.

Apart from the modelling perspective, our analysis has also provided updated international empirical evidence concerning Okun’s law. We find that the dynamic relationship between the variables in all four economies is such that a shock to GDP growth has robustly negative effects on the change in the unemployment rate. This finding is robust to whether we include the period associated with the corona pandemic or not. It confirms Ball et al. (2017) and Ball et al. (2019) who argue that Okun’s law continues to be a robust relationship in empirical macroeconomics. This should be highly relevant information to the central banks of the economies studied here, suggesting that Okun’s law – which has been an important empirical relationship when modelling the economy continues to be useful regardless of modelling choices and time periods.”

From a paper by Tamás Kiss, Hoang Nguyen and Pär Österholm:

“In this paper, we have analysed the relevance of taking non-Gaussianity into account when empirically modelling Okun’s law in Australia, the euro area, the United Kingdom and the United States. Our results based on Bayesian VAR models with stochastic volatility suggest that heavier-than-Gaussian tails find support in some cases. Taking skewness into account is, however, less beneficial in this context considering our baseline sample.

Posted by at 9:50 AM

Labels: Macro Demystified

Subscribe to: Posts