Showing posts with label Global Housing Watch. Show all posts

Thursday, July 25, 2019

Housing Market in France

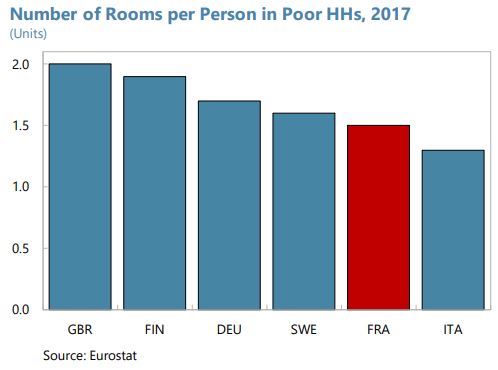

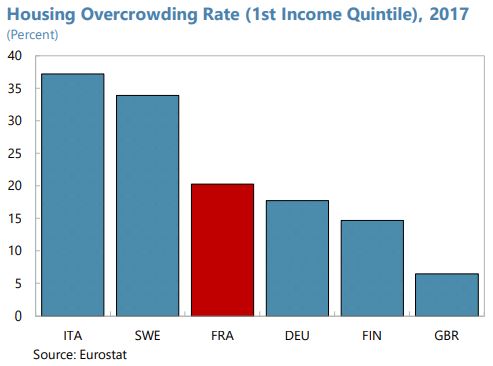

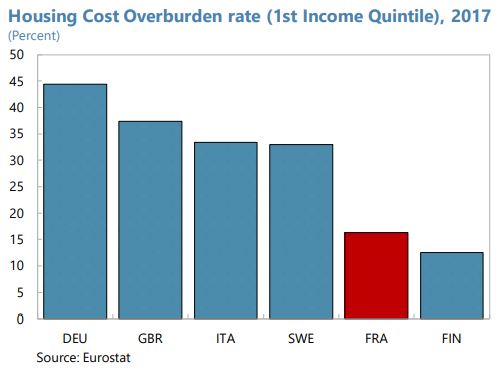

From the IMF’s latest report on France:

“Spending on housing is among the highest among European countries, with mixed outcomes for vulnerable groups (…). Similar to the UK, France spends 1.3 percent of GDP on housing development and housing benefits compared to 0.4 percent and 0.2 percent in Germany and Italy respectively. However, this is associated with mixed outcomes: while the overburden rate of poor households is among the lowest in France (16 percent compared to 37 percent in the UK), the number of rooms per person in poor households is lower in France than in the UK and in Germany, and houses of those at the lowest end of the income distribution in France are three times more overcrowded than in the UK.”

From the IMF’s latest report on France:

“Spending on housing is among the highest among European countries, with mixed outcomes for vulnerable groups (…). Similar to the UK, France spends 1.3 percent of GDP on housing development and housing benefits compared to 0.4 percent and 0.2 percent in Germany and Italy respectively. However, this is associated with mixed outcomes: while the overburden rate of poor households is among the lowest in France (16 percent compared to 37 percent in the UK),

Posted by at 4:31 PM

Labels: Global Housing Watch

Monday, July 22, 2019

Mapped: The Countries With the Highest Housing Bubble Risks

From Visual Capitalist:

“With a decade-long bull market and an ultra low interest rate environment globally, it’s not surprising to see capital flock to housing assets.

For many investors, real estate is considered as good of a place as any to park money—but what happens when things get a little too frothy, and the fundamentals begin to slip away?

In recent years, experts have been closely watching several indicators that point to rising bubble risks in some housing markets. Further, they are also warning that countries like Canada and New Zealand may be overdue for a correction in housing prices.

Key Housing Market Indicators

Earlier this week, Bloomberg published results from a new study by economist Niraj Shah as he aimed to build a housing bubble dashboard.

It tracks four key metrics:

- House Price-Rent Ratio

The ratio of house prices to the annualized cost of rent- House Price-Income Ratio

The ratio of house prices to household income- Real House Prices

Housing prices adjusted for inflation- Credit to Households (% of GDP)

Amount of debt held by households, compared to total economic outputRanking high on just one of these metrics is a warning sign for a country’s housing market, while ranking high on multiple measures signals even greater fragility.”

Continue reading here.

From Visual Capitalist:

“With a decade-long bull market and an ultra low interest rate environment globally, it’s not surprising to see capital flock to housing assets.

For many investors, real estate is considered as good of a place as any to park money—but what happens when things get a little too frothy, and the fundamentals begin to slip away?

In recent years, experts have been closely watching several indicators that point to rising bubble risks in some housing markets.

Posted by at 9:54 AM

Labels: Global Housing Watch

Friday, July 19, 2019

Housing View – July 19, 2019

On cross-country:

- House prices up by 4.0% in both the euro area and the EU – Eurostat

On the US:

- Is rent control making a comeback? – Brookings

- Tackling zoning to help the middle class: 5 policy approaches – Brookings

- Survey Shows Decline in Foreign Investment in U.S. Residential Real Estate – National Association of Realtors

- 5 Lessons from Cities On Affordable Housing – Politico

- Can Robots Solve the Affordable Housing Crisis? – Politico

- Only Washington Can Solve the Nation’s Housing Crisis – New York Times

- Amazon HQ2 Is Upending Northern Virginia’s Already Unstable Housing Market – New York Times

- Property taxes stunt Chicago’s house price growth – Financial Times

- Is California’s apartment market broken? – Brookings

- Housing Affordability and Zoning Reform – Cato

- Wave of Hispanic Buyers Boosts U.S. Housing Market – Wall Street Journal

- A Home Builder Perspective on Housing Affordability and Construction Innovation – Harvard Joint Center for Housing Studies

- Gentrification ‘benefits local residents’, research finds – Financial Times

- Housing’s ‘Missing Middle’ Keeps Shrinking – Bloomberg

- Steep Slowdown Projected in Home Improvements – Harvard Joint Center for Housing Studies

On other countries:

- [China] When Affordable Housing in Shanghai Is a Bed in the Kitchen – Citylab

- [Netherlands] “Mortgage Interest Tax Deduction in the Netherlands: A Welcome Relief” – Netherlands Bank

- [Puerto Rico] Puerto Rico’s housing market improving – Global Property Guide

- [Qatar] Qatar’s housing market is recovering – Global Property Guide

- [United Arab Emirates] UAE’s property prices fall further – Global Property Guide

- [United States]S. housing market gradually cooling – Global Property Guide

*Please note that the Housing View will be on hiatus until September 8.

On cross-country:

- House prices up by 4.0% in both the euro area and the EU – Eurostat

On the US:

- Is rent control making a comeback? – Brookings

- Tackling zoning to help the middle class: 5 policy approaches – Brookings

- Survey Shows Decline in Foreign Investment in U.S. Residential Real Estate – National Association of Realtors

- 5 Lessons from Cities On Affordable Housing – Politico

- Can Robots Solve the Affordable Housing Crisis?

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, July 16, 2019

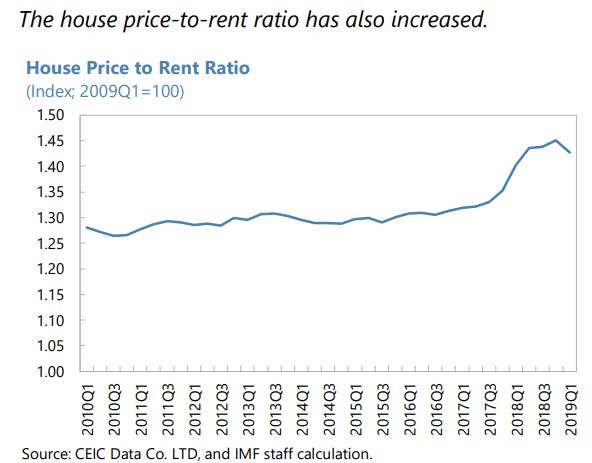

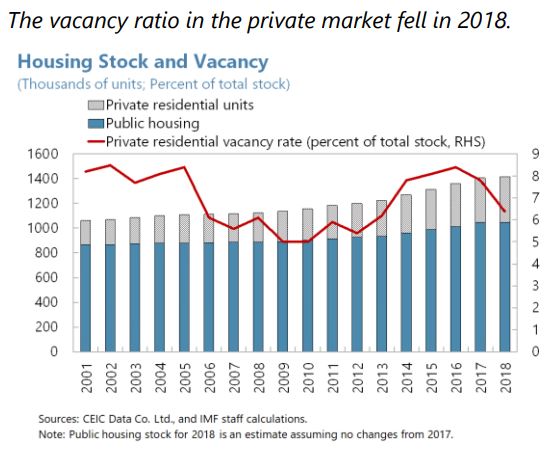

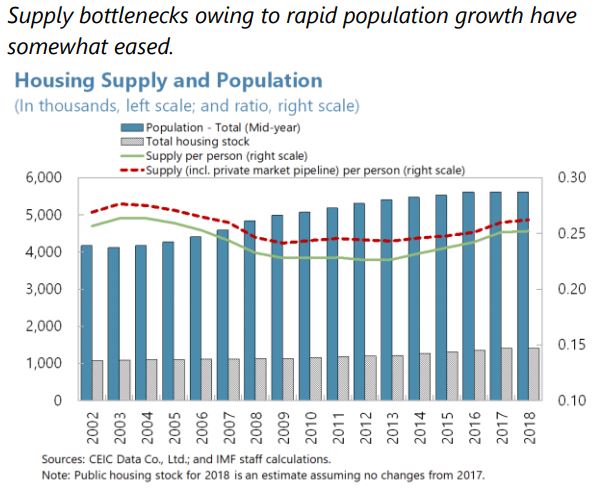

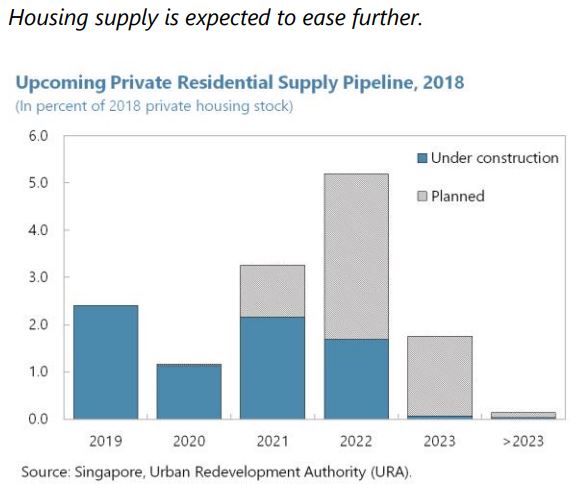

Housing Market in Singapore

From the IMF’s latest report on Singapore:

“The private housing market showed signs of overheating in 2017-18. Average monthly transactions increased by 35 percent in the year through June 2018, compared to the previous two years, and prices increased by 9.1 percent year-on-year in 2018Q2. Developer land purchase activity, including en-bloc purchases, in 2016-2018H1 led to high bidding activity (also implying a rising housing supply over the medium term). The number of foreigners purchasing properties, as well as the transactions values, increased significantly in 2017 and early 2018. In this context, the FSAP analysis found that foreigner residential property purchases had an upward effect on property prices (…).

The authorities tightened macroprudential measures in July 2018 to cool off a rapid increase in real estate prices. In view of rising house prices fueling overvaluation and raising the level of systemic risk, the authorities implemented a package of measures that tightened LTV limits and raised the Additional Buyer’s Stamp Duty (ABSD) for residential property purchases to reduce the risk of a destabilizing price correction. Specifically, for individuals, loan to value (LTV) ratio limits were lowered for all mortgages, and ABSD rates were raised by 5 percentage points, except for Singaporeans and permanent residents buying first properties. For non-individuals, LTVs were lowered and the ABSD was raised by 10 percentage points, with an additional 5 percentage points for housing developers. The differentiation between residents and non-residents in the ABSD was maintained. In response to these policies, house price growth slowed, transactions declined, especially in the private market, and mortgage credit edged down (though remaining high as a share of GDP). Nonetheless, property prices remained moderately overvalued.”

From the IMF’s latest report on Singapore:

“The private housing market showed signs of overheating in 2017-18. Average monthly transactions increased by 35 percent in the year through June 2018, compared to the previous two years, and prices increased by 9.1 percent year-on-year in 2018Q2. Developer land purchase activity, including en-bloc purchases, in 2016-2018H1 led to high bidding activity (also implying a rising housing supply over the medium term). The number of foreigners purchasing properties,

Posted by at 1:32 PM

Labels: Global Housing Watch

Friday, July 12, 2019

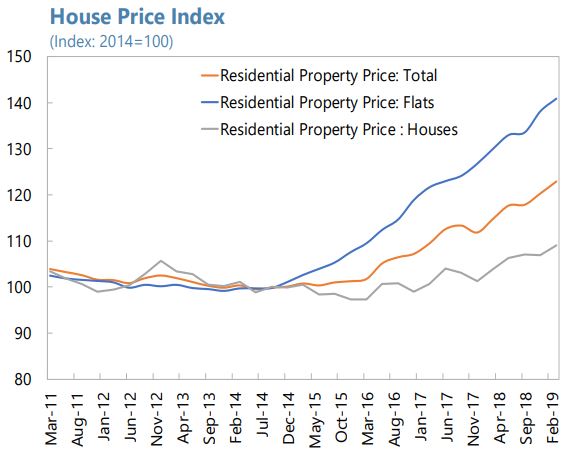

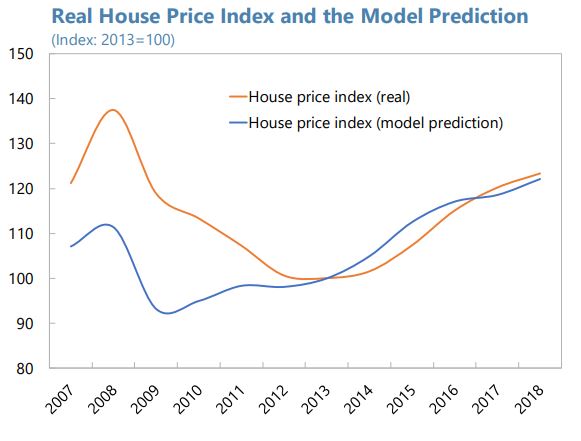

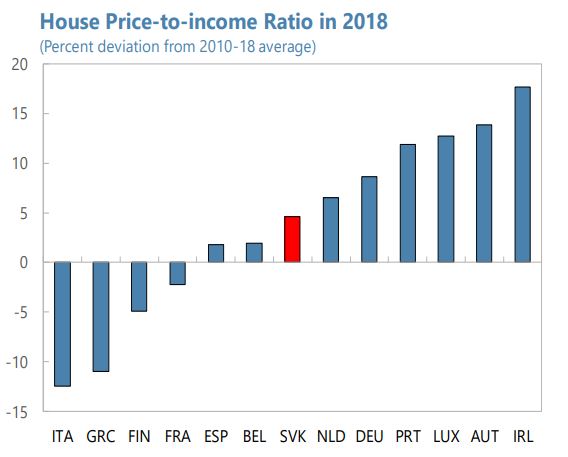

Housing Market in Slovak Republic

From the IMF’s latest report on Slovak Republic:

“There are early signs of a buildup of imbalances in the housing market. Overall house prices have increased in line with peers in the region. A regression-based assessment also shows that overall price increases since 2013 can largely be explained by economic fundamentals (…). Nonetheless, rising house price-to-income ratio shows a mild deviation from the historical average. Flat prices in urban areas have increased much more than the average house price, reflecting strong demand from domestic investors and migrant rural workers as well as supply constraints resulting from limited plot availability and lengthy processes to obtain construction permits. The underdevelopment of the rental housing market—counting only around 10 percent of the housing market— contributes to higher property prices.”

The authorities’ pro-active macroprudential policy stance is welcome and could be strengthened as follows.

- Reduce NPLs of less systemic institutions. The authorities’ initiative to require banks with high NPL ratios to develop an NPL reduction strategy is welcome and their efforts to reduce NPLs should be sustained. To contain credit risks, building societies should be required to increase the NPL coverage ratio. The recently introduced regulatory cap on the share of long-maturity loans in new loans extended by building societies (20 percent for loans with 20–30 years of maturity and 10 percent for loans with 25–30 years of maturity) should be complemented by a cap on the share of uncollateralized loans in total loans.

- Enhance capital buffers of weaker banks. Staff supported incremental use of the counter-cyclical capital buffers (CCyB) and supervisory (Pillar II) capital requirements to enhance resilience of banks to shocks and the authorities’ readiness to further increase the CCyB. In addition, considering the uneven asset quality across banks, the authorities should strongly consider imposing non-zero Pillar II capital guidance for less systemic institutions in 2019 taking into account supervisory stress test results.

- Allow the bank levy to expire. The bank levy, imposed on liabilities (less equity) of banks, weighs heavily on unprofitable banks—in some cases, claiming more than 30 percent of pre-tax income. As the initial targeted amount (EUR 750 million) has already been collected, the levy should be allowed to expire in 2021 as legislated to help these banks safeguard profitability and accumulate buffers.

- Better internalize mortgage credit risks. The average risk weights in the internal models of systemic foreign bank subsidiaries in Slovakia are lower than in most other EU peers reflecting historically low default rates. To discourage excessive risk taking, the authorities should strongly consider introducing a risk weight add-on on housing loans to require banks to better internalize credit risks, which can be complemented with a floor on risk weights on housing loans. The authorities should also be vigilant about possible risks that mortgage brokers may facilitate loosening lending standards of banks.

Considerations should be given to remove preferential tax treatment of housing related capital gains and link real-estate taxation to the market value of the property. These measures are expected to curb demand for real estate, particularly demand related to investment reasons, and add to fiscal revenues. Staff welcomed efforts to streamline regulatory procedures for construction permits, which could improve housing supply and ease price pressures. Legal frameworks governing the rental house market in Slovakia discourage the development of longterm rental market given strong protection of tenants’ rights for contracts beyond two years. Introducing a more balanced regulation of landlord-tenant rights could reduce demand for home ownership from over-leveraged or low-income households.

Continued efforts are needed to implement a robust AML/CFT framework. The authorities made efforts to transpose EU 4th AML Directive in 2018 and are now preparing the AML/CFT Action Plan 2019–22, based on the National Risk Assessment carried out in 2017–18. Sustained efforts are needed, including to improve disciplinary processes, step-up bank employee trainings, strengthen measures to support anti-corruption efforts, and enhance operational independence and effectiveness of the Financial Intelligence Unit.

Strong home-host cooperation should continue. Given the dominance of foreign banks in Slovak banking system, strong home-host cooperation including close engagements in Joint Supervisory Teams in SSM is critical. With limited domestic capacity to absorb bail-inable bonds, encouraging banks to have higher non-regulatory capital buffers may also help them meet minimum requirement for own funds and eligible liabilities (MREL). To fill the gaps identified at European level regulations by the recent euro area FSAP, the domestic regulatory regime should require banks to obtain authorities’ pre-approval in acquiring qualifying holdings of non-bank entities and to periodically report the ultimate beneficial owners of their qualifying holdings.”

From the IMF’s latest report on Slovak Republic:

“There are early signs of a buildup of imbalances in the housing market. Overall house prices have increased in line with peers in the region. A regression-based assessment also shows that overall price increases since 2013 can largely be explained by economic fundamentals (…). Nonetheless, rising house price-to-income ratio shows a mild deviation from the historical average. Flat prices in urban areas have increased much more than the average house price,

Posted by at 10:12 AM

Labels: Global Housing Watch

Subscribe to: Posts