Friday, July 12, 2019

Housing Market in Slovak Republic

From the IMF’s latest report on Slovak Republic:

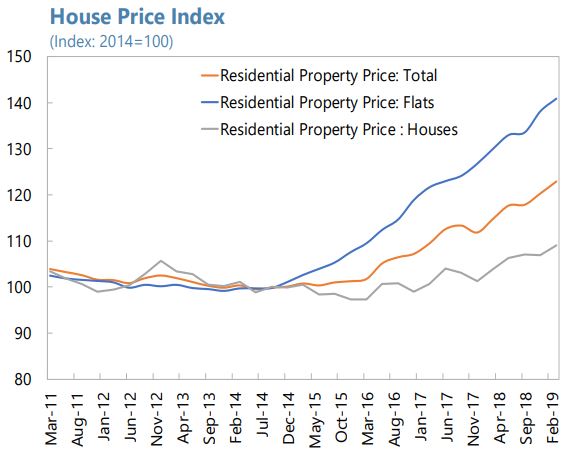

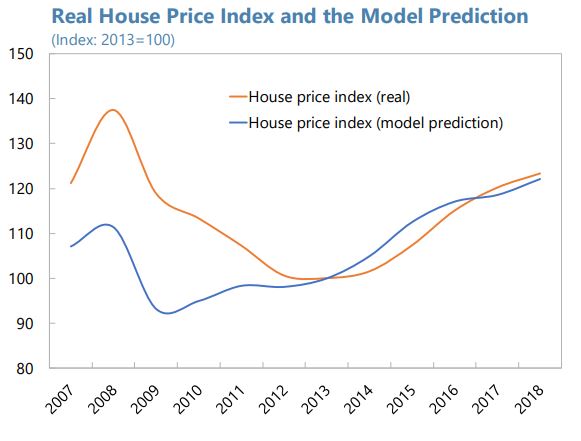

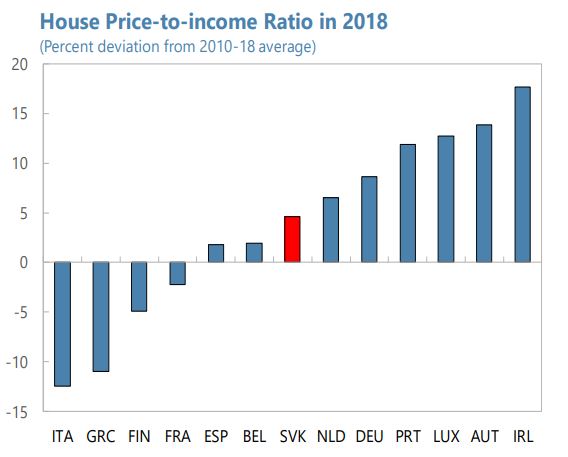

“There are early signs of a buildup of imbalances in the housing market. Overall house prices have increased in line with peers in the region. A regression-based assessment also shows that overall price increases since 2013 can largely be explained by economic fundamentals (…). Nonetheless, rising house price-to-income ratio shows a mild deviation from the historical average. Flat prices in urban areas have increased much more than the average house price, reflecting strong demand from domestic investors and migrant rural workers as well as supply constraints resulting from limited plot availability and lengthy processes to obtain construction permits. The underdevelopment of the rental housing market—counting only around 10 percent of the housing market— contributes to higher property prices.”

The authorities’ pro-active macroprudential policy stance is welcome and could be strengthened as follows.

- Reduce NPLs of less systemic institutions. The authorities’ initiative to require banks with high NPL ratios to develop an NPL reduction strategy is welcome and their efforts to reduce NPLs should be sustained. To contain credit risks, building societies should be required to increase the NPL coverage ratio. The recently introduced regulatory cap on the share of long-maturity loans in new loans extended by building societies (20 percent for loans with 20–30 years of maturity and 10 percent for loans with 25–30 years of maturity) should be complemented by a cap on the share of uncollateralized loans in total loans.

- Enhance capital buffers of weaker banks. Staff supported incremental use of the counter-cyclical capital buffers (CCyB) and supervisory (Pillar II) capital requirements to enhance resilience of banks to shocks and the authorities’ readiness to further increase the CCyB. In addition, considering the uneven asset quality across banks, the authorities should strongly consider imposing non-zero Pillar II capital guidance for less systemic institutions in 2019 taking into account supervisory stress test results.

- Allow the bank levy to expire. The bank levy, imposed on liabilities (less equity) of banks, weighs heavily on unprofitable banks—in some cases, claiming more than 30 percent of pre-tax income. As the initial targeted amount (EUR 750 million) has already been collected, the levy should be allowed to expire in 2021 as legislated to help these banks safeguard profitability and accumulate buffers.

- Better internalize mortgage credit risks. The average risk weights in the internal models of systemic foreign bank subsidiaries in Slovakia are lower than in most other EU peers reflecting historically low default rates. To discourage excessive risk taking, the authorities should strongly consider introducing a risk weight add-on on housing loans to require banks to better internalize credit risks, which can be complemented with a floor on risk weights on housing loans. The authorities should also be vigilant about possible risks that mortgage brokers may facilitate loosening lending standards of banks.

Considerations should be given to remove preferential tax treatment of housing related capital gains and link real-estate taxation to the market value of the property. These measures are expected to curb demand for real estate, particularly demand related to investment reasons, and add to fiscal revenues. Staff welcomed efforts to streamline regulatory procedures for construction permits, which could improve housing supply and ease price pressures. Legal frameworks governing the rental house market in Slovakia discourage the development of longterm rental market given strong protection of tenants’ rights for contracts beyond two years. Introducing a more balanced regulation of landlord-tenant rights could reduce demand for home ownership from over-leveraged or low-income households.

Continued efforts are needed to implement a robust AML/CFT framework. The authorities made efforts to transpose EU 4th AML Directive in 2018 and are now preparing the AML/CFT Action Plan 2019–22, based on the National Risk Assessment carried out in 2017–18. Sustained efforts are needed, including to improve disciplinary processes, step-up bank employee trainings, strengthen measures to support anti-corruption efforts, and enhance operational independence and effectiveness of the Financial Intelligence Unit.

Strong home-host cooperation should continue. Given the dominance of foreign banks in Slovak banking system, strong home-host cooperation including close engagements in Joint Supervisory Teams in SSM is critical. With limited domestic capacity to absorb bail-inable bonds, encouraging banks to have higher non-regulatory capital buffers may also help them meet minimum requirement for own funds and eligible liabilities (MREL). To fill the gaps identified at European level regulations by the recent euro area FSAP, the domestic regulatory regime should require banks to obtain authorities’ pre-approval in acquiring qualifying holdings of non-bank entities and to periodically report the ultimate beneficial owners of their qualifying holdings.”

Posted by at 10:12 AM

Labels: Global Housing Watch

Subscribe to: Posts