Showing posts with label Global Housing Watch. Show all posts

Monday, December 9, 2019

Views from housing market experts

This page compiles together 31 interviews with housing market experts. The interviews are organized by different topics.

On housing market developments across countries

- Enrique Martínez-García and Valerie Grossman (Federal Reserve Bank of Dallas), August 2016.

- Gabriela Inchauste (World Bank), February 2019.

- Ian Bright and Jessica Exton (ING), November 2018.

- Kate Everett-Allen (Knight Frank), September 2017.

- Marja C Hoek-Smit (HOFINET), March 2016.

- Paul Cheshire (London School of Economics), March 2019.

- Stephen Malpezzi (University of Wisconsin-Madison), March 2017.

On housing markets in Africa

- Issa Faye, El-Hadj M. Bah, and Zekebweliwai F. Geh (African Development Bank), April 2018.

- Kecia Rust (Centre for Affordable Housing Finance in Africa), February 2017 and November 2017.

- Riël C. D. Franzsen (University of Pretoria), October 2017.

On housing market in the US and other countries

- Frank Nothaft (CoreLogic, US), August 2017.

- Issi Romem (BuildZoom, US), July 2016.

- Keyes Christopher “KC” Hardin (Conservatorio SA, Panama), September 2018.

- Sock-Yong Phang (Singapore Management University, Singapore), April 2018.

On housing affordability

- Albert Saiz (Massachusetts Institute of Technology), September 2018.

- Matthias Helble (Asian Development Bank), November 2019.

- Shlomo Angel and Achilles Kallergis (New York University), September 2016.

- Stijn Van Nieuwerburgh (Columbia University), September 2019.

- Svenja Gudell (Zillow), October 2016.

On housing finance

- Sarah Quinn (University of Washington) November 2019.

- Susan Wachter (University of Pennsylvania), May 2019.

On housing policies

- Lars E.O. Svensson (Stockholm School of Economics), June 2015.

- Matthias Helble (Asian Development Bank Institute), November 2016.

- Nora Libertun de Duren [In Spanish] (Inter-American Development Bank), March 2018.

- Paavo Monkkonen ( University of California, Los Angeles), March 2018.

On housing supply

- Daniel Garcia (Federal Reserve Board) October 2019.

- Jan Mischke (McKinsey Global Institute), June 2017.

- Jordan Rappaport (Federal Reserve Bank of Kansas City), May 2017 .

- Joseph Gyourko (University of Pennsylvania), April 2017.

On globalization of housing markets

- Christian Hilber (London School of Economics), July 2018.

- Richard Ronald (University of Amsterdam), July 2017.

This page compiles together 31 interviews with housing market experts. The interviews are organized by different topics.

On housing market developments across countries

- Enrique Martínez-García and Valerie Grossman (Federal Reserve Bank of Dallas), August 2016.

- Gabriela Inchauste (World Bank), February 2019.

- Ian Bright and Jessica Exton (ING), November 2018.

- Kate Everett-Allen (Knight Frank), September 2017.

Posted by at 4:00 AM

Labels: Global Housing Watch

Friday, December 6, 2019

Local Capital Scarcity and Small Firm Growth: Evidence from Real Estate Booms in China

From a working paper by Harald Hau, and Difei Ouyang:

“In geographically segmented credit markets, local real estate booms can deteriorate the funding conditions for small manufacturing firms and undermine their competitiveness. Using exogenous variation in the administrative land supply across 172 Chinese cities, we show that higher predicted real estate prices cause higher borrowing costs for small manufacturing firms, reduce their bank lending, lower their investment rate and labor productivity, and reduce their output and TFP growth by economically significant magnitudes. These effects are absent in large and listed companies with access to the national capital market. The evidence highlights the benefits of financial market integration.”

From a working paper by Harald Hau, and Difei Ouyang:

“In geographically segmented credit markets, local real estate booms can deteriorate the funding conditions for small manufacturing firms and undermine their competitiveness. Using exogenous variation in the administrative land supply across 172 Chinese cities, we show that higher predicted real estate prices cause higher borrowing costs for small manufacturing firms, reduce their bank lending, lower their investment rate and labor productivity,

Posted by at 5:17 PM

Labels: Global Housing Watch

Housing View – December 6, 2019

On cross-country:

- The housing unaffordability crisis in Asia – Asian Development Bank

On the US:

- South and Midwest Regions are Gaining Larger Share of Homebuyers – National Association of Realtors

- Housing Booms and the U.S. Productivity Puzzle – Northwestern University

- These housing markets will feel the biggest impact from the ‘Silver Tsunami’ – MarketWatch

- Amazon’s HQ2 making waves in Washington-area housing – HousingWire

- New Mortgage Data Show Business Borrowing Is Key to Affordable Multifamily Housing – Urban Institute

- What’s Behind the Dramatic Improvement in the Federal Housing Administration’s MMI Fund? – Urban Institute

- Housing Finance At A Glance: A Monthly Chartbook, November 2019 – Urban Institute

- The sordid history of housing discrimination in America – VOX

On other countries:

- [Chile] Chile’s house prices remain strong – Global Property Guide

- [Chile] Law and Inclusive Urban Development: Lessons from Chile’s Enabling Markets Housing Policy Regime – The American Journal of Comparative Law

- [France] The impact of taxing vacancy on housing markets: Evidence from France – Journal of Public Economics

- [Hong Kong] What the protests mean for Hong Kong homeowners – Financial Times

- [Ireland] Irish Central Bank Leaves Mortgage-Lending Limits Unchanged – New York Times

- [Germany] New Zealand’s house price rises continue – Global Property Guide

- [Singapore] Singapore Property Glut May Curb Prices, Central Bank Says – Bloomberg

- [Switzerland] Swiss Government Leaves Mortgage Capital Requirements Unchanged – Reuters

- [United Kingdom] Housing – steps in the right direction – Institute for Global Change

- [United Kingdom] Britain’s housing market needs a permanent fix – Financial Times

On cross-country:

- The housing unaffordability crisis in Asia – Asian Development Bank

On the US:

- South and Midwest Regions are Gaining Larger Share of Homebuyers – National Association of Realtors

- Housing Booms and the U.S. Productivity Puzzle – Northwestern University

- These housing markets will feel the biggest impact from the ‘Silver Tsunami’ – MarketWatch

- Amazon’s HQ2 making waves in Washington-area housing – HousingWire

- New Mortgage Data Show Business Borrowing Is Key to Affordable Multifamily Housing – Urban Institute

- What’s Behind the Dramatic Improvement in the Federal Housing Administration’s MMI Fund?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, December 5, 2019

Accuracy and Determinants of Self-Assessed Euro Area House Prices

From an ECB working paper by Julien Le Roux and Moreno Roma:

“Using microdata from the second wave of the Household Finance and Consumption Survey, we investigate the accuracy of property values estimated by homeowners – so called “self-assessed” house prices – and explore the drivers of possible deviations of these prices from official hedonic house price indices. We find evidence that euro area homeowners overestimate the value of their properties by around 9%. Across the largest euro area countries, the overestimation lies in a range between 3.2% in Germany and 22% in Italy. Household characteristics, including the level of indebtedness, appear to explain significant discrepancies between hedonic and self-assessed house price indices, while the limited available data related to property characteristics are generally not affecting this gap. For the euro area, we find that higher self-assessed house prices are associated with a mild increase in consumption expenditures.”

From an ECB working paper by Julien Le Roux and Moreno Roma:

“Using microdata from the second wave of the Household Finance and Consumption Survey, we investigate the accuracy of property values estimated by homeowners – so called “self-assessed” house prices – and explore the drivers of possible deviations of these prices from official hedonic house price indices. We find evidence that euro area homeowners overestimate the value of their properties by around 9%.

Posted by at 3:42 PM

Labels: Global Housing Watch

Housing Market in Hungary

From the IMF’s latest report on Hungary:

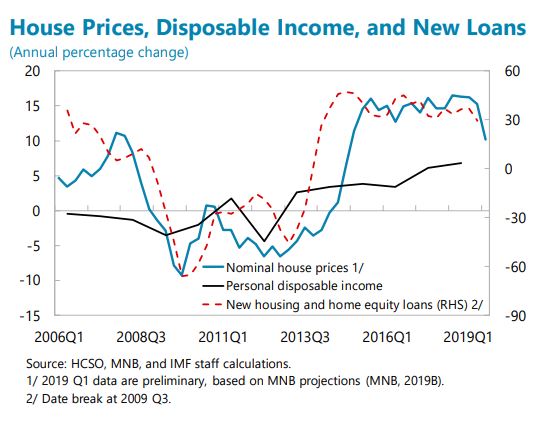

“Efforts to scale back house purchase incentives and to address supply constraints are needed to mitigate market pressures. In 2018, housing price growth was in double digits, especially in Budapest, partly supported by high wage growth, fiscal incentives, and labor scarcity in the construction sector (Figure 3). Budapest house prices appear high compared to fundamentals. Given that a large part of purchases is paid for with private savings, including by foreign citizens, and is done for investment purposes, tightening of macroprudential measures (loan-to-value and debt service-to-income (DSTI) may not be sufficient to contain house price inflation, but can reduce the likelihood of risky mortgages. Moderating price increases would therefore be helped by reviewing the various fiscal incentives for house purchases, basing them on means-testing and targeting, reducing impediments to doing business to spur construction, improving transportation network and commuting options, and improving urban planning to increase housing supply over time. In the context of money laundering risks in the sector, staff also encouraged the authorities to continue their AML/CFT efforts, as Hungary remains on enhanced follow-up based on Moneyval’s 2016 assessment, including by continuing to monitor large purchases of luxury real estate.

The authorities launched several initiatives to reduce the mortgage interest rate risk. While most new housing loans now have longer interest fixation periods—likely facilitated by the MNB Certified Consumer-Friendly Housing Loans and the DSTI requirements—there is still a high portion of existing housing loans with variable rates. The MNB thus agreed with banks that they inform their clients about the interest rate risk and offer to convert to fixed-rates.3 Thus far, the impact of this measure has been limited. To contain potential risks from FX exposure of some of the commercial real estate companies, the MNB has announced that beginning in 2020 a small riskweight would be also assigned to FX performing project loans when calculating the systemic risk buffer.

The authorities are monitoring housing prices, especially in Budapest, even though they are still much lower than in comparable cities in Western Europe. They also noted that assessment models do not capture the fact that many of these purchases are for investment and generate rental income. They agree that additional tightening of macro prudential measures is unlikely to have a significant impact. There is preliminary evidence that the introduction of the retail bond MÁP+ coincided with a decline in apartment sales transactions in Budapest. Some of the MNB’s proposals—included in the MNB’s Competitiveness Program, like tightening the rules for purchases of residences for investment purposes and expanding construction capacity, could help moderate the market.”

From the IMF’s latest report on Hungary:

“Efforts to scale back house purchase incentives and to address supply constraints are needed to mitigate market pressures. In 2018, housing price growth was in double digits, especially in Budapest, partly supported by high wage growth, fiscal incentives, and labor scarcity in the construction sector (Figure 3). Budapest house prices appear high compared to fundamentals. Given that a large part of purchases is paid for with private savings,

Posted by at 10:59 AM

Labels: Global Housing Watch

Subscribe to: Posts