Showing posts with label Global Housing Watch. Show all posts

Wednesday, February 19, 2020

House prices in Croatia

From the IMF’s latest report on Croatia:

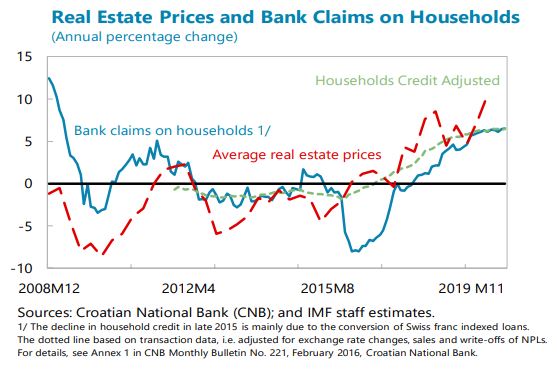

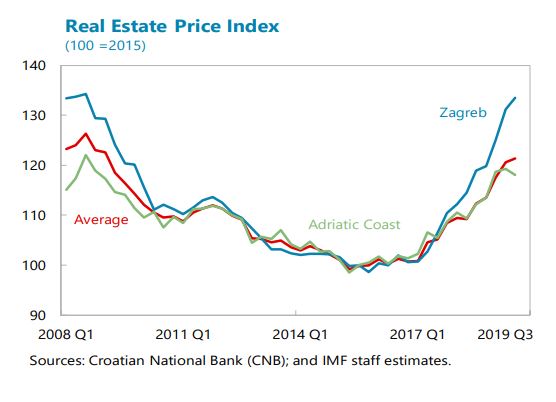

“Housing prices have begun to accelerate, mainly in the capital and coastal areas. Average housing prices grew 8.0 percent, but 12.2 percent in Zagreb (yoy, September 2019). This increase should be seen in context of higher real wages, better employment prospects, growing consumer confidence, as well as declining interest rates. Tourism is the main driver of real estate price developments in Zagreb and the coast. Investment properties for short-term rentals have grown rapidly. This is facilitated by a favorable flat-tax on short-term rentals compared to higher taxation on long-term rentals. Market observers note that some of these purchases are not loan-financed, but they still assume that the majority is financed by bank loans. The market has also been supported by the government’s housing loan subsidy program for young first-time house buyers introduced in 2017 and the reduction of the real estate transfer tax since 2019. According to the CNB’s housing price index, real estate prices are now beginning to reach pre-crisis levels. Staff recommended that housing prices should be monitored with a holistic approach taking into account mortgage lending, general purpose loans that might be diverted to real estate, as well as government housing subsidies on the demand side. Also, the impacts that the current tourism boom and tourism rental taxation policies have on the supply of housing for purchase need to be taken into consideration. The mission welcomed current research efforts of the CNB to better gauge housing affordability.”

From the IMF’s latest report on Croatia:

“Housing prices have begun to accelerate, mainly in the capital and coastal areas. Average housing prices grew 8.0 percent, but 12.2 percent in Zagreb (yoy, September 2019). This increase should be seen in context of higher real wages, better employment prospects, growing consumer confidence, as well as declining interest rates. Tourism is the main driver of real estate price developments in Zagreb and the coast.

Posted by at 10:03 AM

Labels: Global Housing Watch

Tuesday, February 18, 2020

Property price dynamics: domestic and international drivers

From BIS:

“Although residential and commercial real estate prices are increasingly moving in sync and the role of international investors is growing, this does not mean that there is a global real estate market, a report by the Committee on the Global Financial System finds.

Property price dynamics: domestic and international drivers documents recent trends in residential and commercial property prices in over 20 countries, gives an overview of key drivers of price developments and describes policy initiatives used to manage associated risks to the economy and financial stability.

Property prices have been rising, reaching record highs in many countries. As prices appear high in comparison to simple rule-of-thumb valuation benchmarks, such as rents and incomes, some central banks are concerned about the consequences of a potential correction. In many cases, however, current price developments can be largely explained by fundamental drivers such as interest rates and income, the report finds.

“A key takeaway is that even if prices (both residential and commercial) have become more synchronised over the past decade, this doesn’t imply that we now have a global real estate market,” said Study Group Chair Paul Hilbers, Director of Financial Stability at the Netherlands Bank.

“Significant differences in cross country price dynamics reflect the strength of local drivers. Some drivers are more important in some countries than in others.”

A third highlight is evidence of the growing role of international investors in many markets. Policymakers have found they need alternative tools to deal with foreign buyers. These investors do not fund their purchases through local banks, so fiscal tools like higher stamp studies may be more effective than macroprudential policy.

The CGFS is a central bank forum for the monitoring and analysis of broad financial system issues. It supports central banks in the fulfilment of their responsibilities for monetary and financial stability by contributing appropriate policy recommendations.”

From BIS:

“Although residential and commercial real estate prices are increasingly moving in sync and the role of international investors is growing, this does not mean that there is a global real estate market, a report by the Committee on the Global Financial System finds.

Property price dynamics: domestic and international drivers documents recent trends in residential and commercial property prices in over 20 countries,

Posted by at 9:15 AM

Labels: Global Housing Watch

What makes capital cities the best places to live?

From Eurofund paper by Tadas Leončikas and Sevinç Rende:

- “In Europe, people living in the capital city generally have a better quality of life than people living in other parts of a country. On this basis, it seems that capital cities are indeed the best places to live.

- For most countries, residents of the capital city score higher on life satisfaction on average than people living outside the capital.

- Life satisfaction in a capital city for the most part is closer to the national average than to the averages of other capital cities. This finding suggests that, despite concerns that capitals increasingly operate independently of their nations, national-level factors are still important in shaping differences in well-being both between countries and between capital cities.

- Capital cities have, by and large, larger proportions of people who report feeling resilient – able to cope during times of hardship – compared to other urban centres and rural regions in the same country. Some characteristics of city populations – such as a younger age profile and higher educational attainment – contribute to resilience, while others, such as housing insecurity, erode it. The findings suggest that some other latent factor, possibly related to opportunities for economic advancement and improving one’s living standards, could underlie the extra resilience that capital cities provide.

- Capital city residents tend to be more satisfied with how democracy works in their country compared to the population outside the capital. This difference is largely associated with socioeconomic background, which on average is more advantageous in capital cities. Capital city residents also tend to have greater trust in national institutions and be more critical of local or municipal authorities than people in the rest of the country.”

From Eurofund paper by Tadas Leončikas and Sevinç Rende:

- “In Europe, people living in the capital city generally have a better quality of life than people living in other parts of a country. On this basis, it seems that capital cities are indeed the best places to live.

- For most countries, residents of the capital city score higher on life satisfaction on average than people living outside the capital.

Posted by at 9:10 AM

Labels: Global Housing Watch

Friday, February 14, 2020

Housing View – February 14, 2020

On cross-country:

- ECB’s house price headache too big to solve – Reuters

- Guidelines for the Implementation of the Right to Adequate Housing – UN

- Are current measures of housing affordability fit for purpose? – Housing Europe

- Smashed avocado on toast and the housing market – ING

- What are macroprudential tools? – Brookings

On the US:

- S. Homeowners Four Times As Likely To Be Equity-Rich Than Seriously Underwater – ATTOM

- How to Make Housing Markets Fairer for All – E21

- The Fed Faces a Housing Conundrum – Bloomberg

- San Jose’s Severe Housing Shortage Is Easy to Fathom – Wall Street Journal

- Are you waiting for house prices to drop during the next recession to buy a home? Why you could have a very a long wait – MarketWatch

- History of Housing Policy in the United States – Portland State University

- Housing Sentiment Nears Survey High as More Consumers Expect Mortgage Rates to Remain Favorable – Fannie Mae

- The Geography of Housing Market Liquidity During the Great Recession – Federal Reserve Bank of St. Louis

- The GSEs and the Economic Cycle: Realistic Expectations – Harvard Joint Center for Housing Studies

On other countries:

- [Rwanda] Housing policies in Rwanda – International Growth Centre

- [United Kingdom] Where are we in the property cycle? – Financial Times

- [United Kingdom] Britons Priced Out of Housing Market Face Renting Into Old Age – Bloomberg

- [United Kingdom] K. Housing Market Sees Renewed Optimism in January, RICS Says – Bloomberg

On cross-country:

- ECB’s house price headache too big to solve – Reuters

- Guidelines for the Implementation of the Right to Adequate Housing – UN

- Are current measures of housing affordability fit for purpose? – Housing Europe

- Smashed avocado on toast and the housing market – ING

- What are macroprudential tools? – Brookings

On the US:

- S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, February 12, 2020

Construction Activity Can Signal When Credit Booms Go Wrong

From a new IMF research paper by Giovanni Dell’Ariccia, Ehsan Ebrahimy, Deniz O Igan, and Damien Puy:

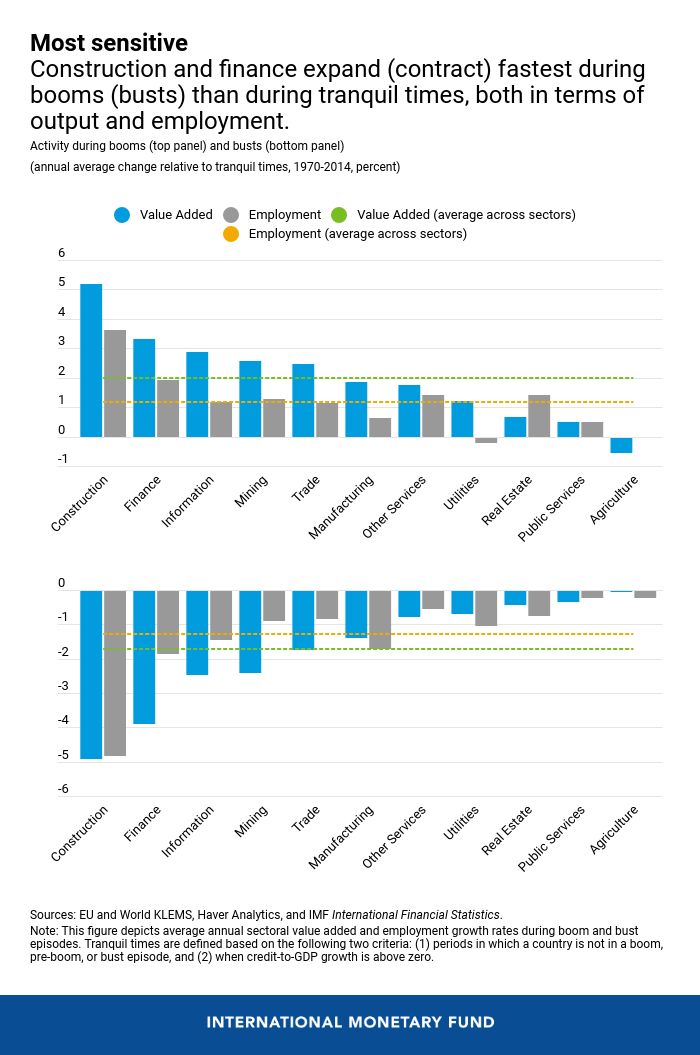

“In Spain, private sector credit as a share of GDP almost doubled between 2000 and 2007. This increase was accompanied by a boom in housing prices—which doubled in real terms over the same period. The economy as a whole also grew at a record pace.

But then in 2008, Spain’s credit bubble burst, and with it came loan defaults, bank failures, and a prolonged economic slowdown.

A less-noticed development in Spain was in the construction sector, where employment grew by an astounding 47 percent, compared to the economy-wide increase of 27 percent.

New IMF staff research, based on a large sample of advanced and emerging market economies since the 1970s, shows that long-lasting credit booms that featured rapid construction growth never ended well.

New evidence on credit booms

Rapid credit growth—known as “credit booms”—presents a trade-off between immediate, buoyant economic performance and the danger of a future crisis. The risk of a “bad boom”—where a rapid credit growth episode is followed by a financial crisis or subpar economic growth—increases when there is also a boom in house prices.

Our research shows that the experience with the dangerous combination of credit booms and rapid expansion in the construction sector goes beyond the Spanish borders and extends to time periods not related to the global financial crisis.

We find that signals from construction activity may help to tell apart the dangerous booms, which need to be controlled, from the episodes of buoyant but healthy credit growth (“good booms”).

Credit booms do not lift all boats alike

During booms, output and employment expand faster. But not all sectors behave the same. Most of the extra growth is concentrated in a few industries—specifically, construction and, at a distant second, finance.

However, the same industries that benefit the most during booms experience the most severe downturns during busts. This implies that credit booms tend to leave few long-term footprints on a country’s industrial composition.”

Continue reading here.

From a new IMF research paper by Giovanni Dell’Ariccia, Ehsan Ebrahimy, Deniz O Igan, and Damien Puy:

“In Spain, private sector credit as a share of GDP almost doubled between 2000 and 2007. This increase was accompanied by a boom in housing prices—which doubled in real terms over the same period. The economy as a whole also grew at a record pace.

But then in 2008, Spain’s credit bubble burst,

Posted by at 10:49 AM

Labels: Global Housing Watch

Subscribe to: Posts