Showing posts with label Global Housing Watch. Show all posts

Tuesday, November 23, 2021

Some Eviction Economics

From a post by Conversable Economist:

“Part of the Coronavirus Aid, Relief, and Economic Security Act (the CARES Act) signed into law by President Trump on March 27, 2020, was a national moratorium on evictions. However, the moratorium was scheduled to end on July 24, 2020–although it effectively required an additional 30 days beyond that date before landlords could file notices to vacate. Congress did not vote to extend the moratorium. However, the Centers for Disease Control then announced a national eviction moratorium to start on September 4, 2020. The US Supreme Court held in August 2021 that the CDC lacked the power to make this policy decision without the passage of a law through Congress and signed by the president. Of course, the Supreme Court decision was not about whether the eviction moratoriums were good policy or had beneficial effects. Here, I set aside the legal questions and focus on what we know about the outcomes.

It’s worth saying at the start that data on rental evictions is not nationally centralized, and is not up-to-the-minute. Every study has its own sample. However, certain patterns do seem to emerge across studies. Jasmine Rangel, Jacob Haas, Emily Lemmerman, Joe Fish, and Peter Hepburn at The Eviction Lab at Princeton University provide evidence on overall eviction patterns in “Preliminary Analysis: 11 months of the CDC Moratorium” (August 21, 2021). Their project collects data from 31 cities and six full states, representing about one-fourth of all the renters in the country. Here’s their estimate based on the sites they trask of how the total number of evictions would have evolved starting in January 2020, compared to what actually happened. Evictions fall by about half starting in March 2020 , and the gap between expected and actual evictions continues to expand after the CDC moratorium is enacted in September 2020.”

Continue reading here.

From a post by Conversable Economist:

“Part of the Coronavirus Aid, Relief, and Economic Security Act (the CARES Act) signed into law by President Trump on March 27, 2020, was a national moratorium on evictions. However, the moratorium was scheduled to end on July 24, 2020–although it effectively required an additional 30 days beyond that date before landlords could file notices to vacate. Congress did not vote to extend the moratorium. However, the Centers for Disease Control then announced a national eviction moratorium to start on September 4,

Posted by at 10:36 AM

Labels: Global Housing Watch

Friday, November 19, 2021

Housing View – November 19, 2021

On cross-country:

- ECB warns of ‘exuberance’ in housing, junk bonds and crypto assets. Investors taking risks in search for yield has left markets ‘susceptible to correction’ – FT

- ECB sees rising risk that housing bubble will burst – Reuters

- The euro area housing market during the COVID-19 pandemic – European Central Bank

- As housing costs rocket, governments take aim at large investors. The approach is politically expedient, but it may not make housing cheaper – The Economist

- The oldest asset class of all still dominates modern wealth. Low interest rates in advanced countries have pushed money into real estate instead of business investment – FT

- Making Homes More Affordable in IDA Countries Through Expanded Mortgage Financing – World Bank

On the US:

- Fannie Mae, Freddie Mac to Back Home Loans of Nearly $1 Million as Prices Soar. Scheduled increase in loan limits is a boon for borrowers but also stokes debate over government’s role in housing market – Wall Street Journal

- A Housing Gift for Beverly Hills. Just what the economy doesn’t need: subsidies for $1 million mortgages. – Wall Street Journal

- Homes Now Typically Sell in a Week, Forcing Buyers to Take Risks. Buyers are often waiving traditional safeguards in fast-moving market where median price has climbed – Wall Street Journal and Quartz

- Democrats have no plan to fight housing inflation. Home prices have skyrocketed, and the White House’s plan will do basically nothing to stop it. – Vox

- Why building more affordable housing won’t solve the crisis – Yahoo

- Housing inflation is getting worse. Will Biden’s ‘Build Back Better’ program help renters and buyers? – MarketWatch

- States can improve housing well-being through thoughtfully designed policies – Brookings

- How the Pandemic Worsened a Housing Crisis in the Bronx. In a New York City borough where residents have long struggled to afford their homes, thousands are now threatened with eviction as state pandemic aid dwindles. – New York Times

- Mortgage Refinance Costs and a Better Adjustable-Rate Mortgage Contract – Richmond Fed

- Biased appraisals and the devaluation of housing in Black neighborhoods – Brookings

- Grown Kids Still Stuck at Home? Change Is on the Horizon. Someday, surely, all the young adults still living with their parents will form their own households, creating steady housing demand. But only if prices stop going up so fast. – Bloomberg

- Want More Affordable Housing and Health Care? Here’s a Fix. – New York Times

- Despite Supply Chain Issues, U.S. Builder Confidence Upticks in November – World Property Journal

- What Went Wrong With Zillow? A Real-Estate Algorithm Derailed Its Big Bet. The company had staked its future growth on its digital home-flipping business, but getting the algorithm right proved difficult – Wall Street Journal

- Research: Restricting Airbnb Rentals Reduces Development – Harvard Business Review

On China

- China home prices fall as property slowdown threatens economic outlook. Beijing introduced measures aimed at constraining borrowing at developers over asset bubble fears – FT

- Worst yet to come for China’s housing market as new home prices fall by most in 6 years. The average price across 70 cities dropped 0.25 per cent in October from the previous month, data shows, as analysts warn that doesn’t give the full picture. Developers are seeing a big slump in sales amid a credit crunch sparked by the debt crisis at China Evergrande – South China Morning Post

- How Wealth Products Helped Inflate China Real Estate – Quartz

- China’s real estate woes sap property investment products – Reuters

- China walks a tightrope on property clampdown – Reuters

On other countries:

- [Canada] Housing Market Heats Back Up in Canada With 8.6% Jump in Sales – Bloomberg

- [Israel] Bank of Israel Plans to Increase Competition in Mortgage Market – Bloomberg

- [Spain] If health and education are essential services in Spain, why not housing? A renters’ movement in Catalonia is saving families from eviction and trying to fill the gap left by the state – The Guardian

- [Spain] Spain takes on private equity landlords as cost of housing soars. Blackstone and others could face rent caps in bill championed by leftwing government – FT

- [Switzerland] The Local Effects of Relaxing Land Use Regulation on Housing Supply and Rents – SSRN

On cross-country:

- ECB warns of ‘exuberance’ in housing, junk bonds and crypto assets. Investors taking risks in search for yield has left markets ‘susceptible to correction’ – FT

- ECB sees rising risk that housing bubble will burst – Reuters

- The euro area housing market during the COVID-19 pandemic – European Central Bank

- As housing costs rocket, governments take aim at large investors.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, November 17, 2021

When Residential Real Estate Turned Commercial: Working from Home

From Conversable Economist:

“Everyone knows that lots of people have ended up working from home, either part-time or full-time, since the start of the pandemic. But I’m not sure many of us have appreciated how extraordinary that shift has been. In effect, an enormous amount of what economists would classify as “residential capital” was converted to commercial real estate almost overnight: that is, people used their places of residence along with capital that had often been installed at their place of residence mostly for other purposes (like entertainment) to do their work.

The size of the shift is remarkable. Janice C. Eberly, Jonathan Haskel and Paul Mizen discuss “Potential Capital: Working From Home, and Economic Resilience” (NBER Working Paper 29431, October 2021, subscription needed). They compare the drop in economic output from the workplace in the first two quarters of 2020 to the overall drop in economic output: in the US economy, for example, they find that output in the workplace fell by about 17%, but total economic output actually fell about 9%. Work done outside the conventional workplace made up the difference.

This built-in resilience of the economy may now seem pretty obvious, but it wasn’t obvious (at least to me) before the pandemic hit. The magnitudes here are enormous. According the US Bureau of Economic Analysis, the value of residential real estate in 2020 was almost $25 trillion. Privately owned nonresidential structures were worth almost $16 trillion, while the equipment in those structures was another $7 trillion. In short, trillions of dollars of residential capital replaced trillions of dollars of nonresidential capital in a very short time. The transition was far from seamless or painless, of course, but the fact that it happened at all is worth a gasp.”

Continue reading here.

From Conversable Economist:

“Everyone knows that lots of people have ended up working from home, either part-time or full-time, since the start of the pandemic. But I’m not sure many of us have appreciated how extraordinary that shift has been. In effect, an enormous amount of what economists would classify as “residential capital” was converted to commercial real estate almost overnight: that is, people used their places of residence along with capital that had often been installed at their place of residence mostly for other purposes (like entertainment) to do their work.

Posted by at 6:34 AM

Labels: Global Housing Watch

The post-war rise of popular wealth

From a VoxEU post by Daniel Waldenström:

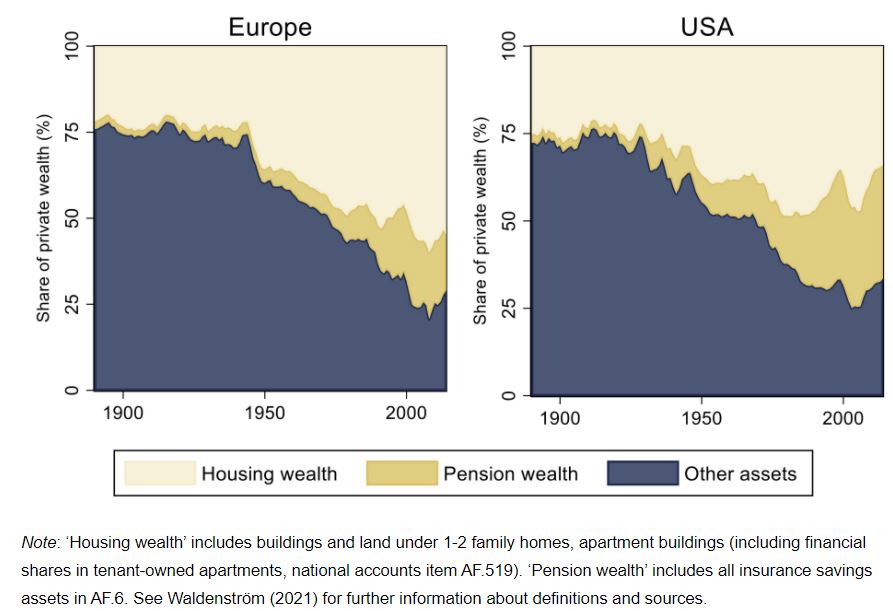

“Since 1950, private wealth-income ratios have grown steadily around the Western world, accelerating after 1990. Figure 3 examines this development by decomposing private wealth into three asset groups: housing wealth, pension wealth, and other wealth.

The main result is that private wealth underwent a structural shift over the 20th century. Around 1900, wealth was dominated by agricultural estates and corporate wealth, assets predominantly held by the rich. During the post-war period, wealth accumulation came mainly in housing and funded pensions, which are assets held by ordinary people. This compositional trend had important distributional implications.”

Figure 3 Decomposing aggregate wealth-income ratios since 1890

Continue reading here.

From a VoxEU post by Daniel Waldenström:

“Since 1950, private wealth-income ratios have grown steadily around the Western world, accelerating after 1990. Figure 3 examines this development by decomposing private wealth into three asset groups: housing wealth, pension wealth, and other wealth.

The main result is that private wealth underwent a structural shift over the 20th century. Around 1900, wealth was dominated by agricultural estates and corporate wealth, assets predominantly held by the rich.

Posted by at 6:30 AM

Labels: Global Housing Watch

Monday, November 15, 2021

Housing Market in Netherlands

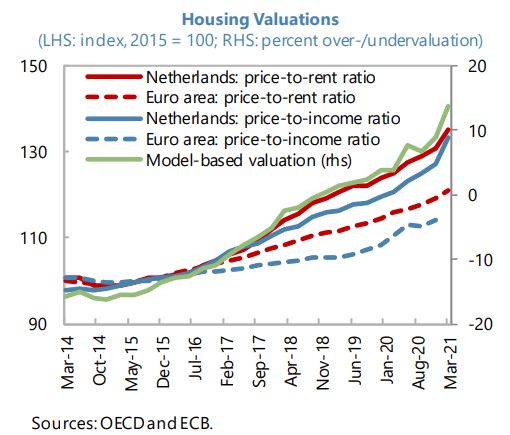

From the IMF’s latest report on Netherlands:

“Real estate markets call for heightened vigilance and the pursuit of policies to address near-term risks and long-term challenges confronting residential and commercial properties. Prices – and valuations – for housing have continued to soar during the pandemic (see chart), reflecting longstanding supply bottlenecks, low interest rates, and the favorable tax treatment of owner-occupied housing. Existing vulnerabilities have been exacerbated by a further rise in already elevated levels of mortgage debt, with some households exceedingly stretching their debt servicing capacity. Consequently, the activation of floors for risk weights applied to mortgage lending from 2022 is welcome and may be complemented by measures such as an additional reduction in eligible loan-to-value ratios, and reviewing the taxation of owner-occupied housing. In addition, efforts to improve the elasticity of the housing supply appear warranted, as structural rigidities, such as distorted planning incentives and restrictive building or zoning laws, maintain imbalances. Such policies will also support macroeconomic stability by lessening households’ exposure to house-price fluctuations, which can significantly affect consumer spending.

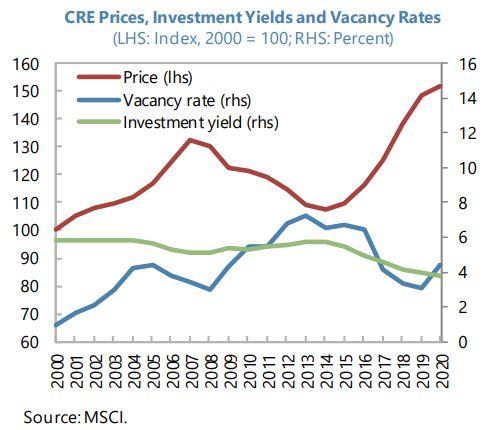

Vacancy rates for commercial properties have increased due to the recession yet with little effect on prices as investment yields have stayed attractive in relation to other assets. With banks maintaining comparatively large exposures, valuation has become a concern, especially since long-term structural change may prevent the full recovery of some property segments. The authorities should contemplate options to better steer the investment cycle of commercial real estate to avoid a build-up of financial stability risks, potentially modelled on policies in place for owner-occupied dwellings. Furthermore, incentivizing climate-friendly modernization or the rededication of obsolete structures should help preserve the value of existing buildings.”

From the IMF’s latest report on Netherlands:

“Real estate markets call for heightened vigilance and the pursuit of policies to address near-term risks and long-term challenges confronting residential and commercial properties. Prices – and valuations – for housing have continued to soar during the pandemic (see chart), reflecting longstanding supply bottlenecks, low interest rates, and the favorable tax treatment of owner-occupied housing. Existing vulnerabilities have been exacerbated by a further rise in already elevated levels of mortgage debt,

Posted by at 11:30 AM

Labels: Global Housing Watch

Subscribe to: Posts