Showing posts with label Global Housing Watch. Show all posts

Sunday, December 19, 2021

Interview with Edward Glaeser on Urban Evolution

From Conversable Economist:

“David A. Price interviews Edward Glaeser, with the subheading “On urbanization, the future of small towns, and “Yes In My Back Yard” (Econ Focus, Federal Reserve Bank of Richmond, Fourth Quarter 2021, pp. 19-23). Here are a few comments that caught my eye.

On centripetal and centrifugal forces in cities

I see urban growth as almost uniformly a dance between technologies that pull us together and ones that push us apart.

Technologies of the 19th century, like the skyscraper — which is really the combination of a steel frame and an elevator — the streetcar, the steam engine, all of these things enabled the growth of 19th century cities. They brought people together. This was a centripetal age.

In the mid-20th century, we had technologies that were major jumps forward in transportation cost. In transportation technology, like the car, and in technology for transporting ideas and entertainment — television and radio — these were centrifugal forces that basically flattened the Earth and made it easier to live in far-flung suburbs or even rural areas. Those centrifugal technologies … were the backdrop for the exodus of people from dense cities that had been built around streetcars and subways and to suburbs that were built around the car.

But then in the late 20th century and early 21st century, the tides turned again. … We’ve started to see the electronic cottages become a force during the pandemic, and suburbanization has continued, but downtowns are vastly stronger than they were in the 1980s. And I think the primary reason is that globalization and new technologies have radically increased the returns to being smart, and we are a social species that gets smart by being around other smart people. That’s why people are willing to pay so much to be in the heart of Silicon Valley and why they’re willing to pay so much for downtown real estate in Chicago or New York or London.

On the shift to a rental market in single family homes

Traditionally, single-family homes were overwhelmingly owner-occupied in the U.S. More than 85 percent, I think, of homes were owner-occupied. The usual view of the housing economics community was that the agency problems involved in renting them out were huge. There are estimates that suggest that renting out for a year involves a 1 percent decline in the value of the house, or something like that, because the renter just doesn’t treat it properly. By contrast, traditionally more than 85 percent of multi-family housing was rented, at least once you get to over five stories. It’s much easier to manage a multi-unit building when you have one owner. One roof, one owner, because otherwise you’ve got the problems of coordination of the condo association or the co-op board, which can be more fractious.

So those were the things, I think, that were responsible for tying ownership type and structure type so closely together. We are starting to see that break down, which is quite interesting. I don’t know if these buyers have fully internalized their difficulties with the maintenance that goes into rental houses as a long-run issue. Or if technology has changed in such a way that they think that they can actually solve that agency problem and that they can figure out ways to deal with the maintenance costs in some efficient fashion. I’m happy to see an emergence of a healthy rental market in single-family detached housing, but I’m keenly aware of the limitations and difficulties of doing that. So, we’ll have to see how this plays out. I can’t help thinking some part of it just has to be that investors are simply searching for new investment products.”

Continue reading here.

From Conversable Economist:

“David A. Price interviews Edward Glaeser, with the subheading “On urbanization, the future of small towns, and “Yes In My Back Yard” (Econ Focus, Federal Reserve Bank of Richmond, Fourth Quarter 2021, pp. 19-23). Here are a few comments that caught my eye.

On centripetal and centrifugal forces in cities

I see urban growth as almost uniformly a dance between technologies that pull us together and ones that push us apart.

Posted by at 7:49 AM

Labels: Global Housing Watch

Saturday, December 18, 2021

Buildings key to achieving Europe’s climate goals

From Social Europe:

“There are fears the revised directive on energy performance due from the European Commission will not be adequate to the task.

The revision of the Energy Performance of Buildings Directive (EPBD), expected from the European Commission today, as part of the Fit for 55 package, is a legislative milestone which cannot go under the radar.

In the bloc’s effort to achieve climate neutrality and fulfil its international climate commitments, the building sector has a systemic role to play. The EPBD is the main policy instrument regulating buildings across the European Union.

Since its first adoption in 2002, the legislation has been key to improving the energy performance of the European building stock, by fostering energy efficiency and aiming at long-term decarbonisation. But given the need to take decisive action in this decade to tackle the climate emergency, the time has come for a comprehensive revision, to fill gaps and raise ambition.

Profound transformations are urgently needed to decarbonise buildings, ensuring that the sector contributes to the efforts to limit temperature rise to 1.5C. Indeed, the homes and offices which surround us today are among the main culprits of the climate crisis, accounting for around 40 per cent of all energy consumed and 36 per cent of energy-related greenhouse-gas emissions in the EU.”

Continue reading here.

From Social Europe:

“There are fears the revised directive on energy performance due from the European Commission will not be adequate to the task.

The revision of the Energy Performance of Buildings Directive (EPBD), expected from the European Commission today, as part of the Fit for 55 package, is a legislative milestone which cannot go under the radar.

In the bloc’s effort to achieve climate neutrality and fulfil its international climate commitments,

Posted by at 7:15 AM

Labels: Global Housing Watch

Friday, December 17, 2021

Housing View – December 17, 2021

Please note that Housing View will be on hiatus for the last two week of December and will resume back in January 2022.

On cross-country:

- The laws of attraction: Economic drivers of inter-regional migration, the role of housing, and public policies – VoxEU

- Affordability the casualty amid ever-climbing global property prices – Reuters

On the US:

- A New Year Brings a New Surge in Housing Prices. People are ricocheting between skyrocketing rents and a red-hot home market, upending old seasonal patterns as job and wage growth drive a new economic cycle. – Bloomberg

- Millennials Are Supercharging the Housing Market. The generation that supposedly didn’t want to buy things now accounts for over half of all home-purchase loan applications; economists expect them to bolster demand for years – Wall Street Journal

- You Won’t be My Neighbor: Opposition to High Density Development – Urban Affairs Review

- Boom in Housing Prices Helps Hawaii More Than Any Other State – Bloomberg

- A Black couple had a White friend show their home and its appraisal rose by nearly half a million dollars – CNN

- What’s Behind the Racial Homeownership Gap in Philadelphia? – Philadelphia Fed

- Black homeownership is declining in Philly – NPR

- Biden taps Thompson for full term as top housing regulator. The move comes after Thompson allies on the Hill urged Biden to keep her at the helm amid reports he planned to replace Thompson this fall. – Politico

- A Refugee Crisis Runs Into a Housing Crisis. Thousands of Afghan refugees are being released from military bases to U.S. cities to rebuild their lives. Settling them into homes amid a rental shortage is proving to be a challenge. – New York Times

- How landlords thwart America’s attempts to house poor people. It is one thing to receive a housing voucher and quite another to successfully use it – The Economist

- As Home Prices Soar Elsewhere, California Starts to Seem Almost Reasonable – UCLA

On China

- The user cost of housing and the price-rent ratio in Shanghai – Regional Science and Urban Economics

- China struggles to shrug off weak consumer spending and property woes. New home prices decline at steepest rate since 2015 while retail sales come in below forecasts – FT

- Kaisa offshore investors in talks to buy group’s distressed loans. Creditors seek inroads into Chinese developers’ opaque restructurings after Evergrande collapse – FT

- China’s central bank urges backing for affordable housing in Shanghai – Reuters

- Private equity cuts back on China property as Evergrande hits stocks. A third of firms plan to reduce exposure to sector as developer’s default reverberates through market – FT

- China’s Coming Property Correction: A Managed Soft Landing – MacroPolo

- Abandoned Projects Shatter Confidence in China’s Home Market – Bloomberg

- U.S. Home-Price Surge Looks Much Tamer in Government CPI Report – Bloomberg

- China’s property slowdown sheds light on another worrying debt problem. Local-government financing vehicles, not just developers, are saddled with lashings of debt – The Economist

- China housing market slumps again as another developer runs into trouble. House prices, sales and construction all fell in November as Shimao Group shares plunge and Beijing assesses what to do with Evergrande – The Guardian

On other countries:

- [Australia] New Zealand has adopted a radical rezoning plan to cut house prices – could it work in Australia? Councils won’t be able to block townhouses or apartments under a sweeping reform aimed at improving affordability – but will it work? And could the idea cross the Tasman? – The Guardian

- [Canada] Canadian Home Prices Surge a Record 25% Amid Persistent Shortage – Bloomberg

- [Germany] Temporal dynamics of rent regulations – The case of the German rent control – Regional Science and Urban Economics

- [Germany] As COVID-19 continues, other issues are coming to the fore – Savills

- [Ireland] Sharon Donnery: The role of central banks in housing markets – Central Bank of Ireland

- [Singapore] Singapore tightens curbs to cool buoyant property market – Reuters

- [United Kingdom] House price push by Bank of England is oddly timed. The central bank has suggested removing one of the post-financial crisis guardrails against runaway mortgage debt – FT

- [United Kingdom] ‘Piecemeal’ rental housing policy fails tenants, warns UK watchdog. The National Audit Office calls for overarching strategy to help renters in difficulties – FT

- [United Kingdom] U.K.’s Fixed Mortgages Mean Faster BOE Rate Rises May Be Needed – Bloomberg

- [United Kingdom] U.K. Housing Loses Momentum With Second Drop in Asking Prices – Bloomberg

- [United Kingdom] U.K.’s House Price Boom Driven by ‘Race for Space’, BOE Says – Bloomberg

- [Uruguay] Spillover effects from new housing supply – Regional Science and Urban Economics

Please note that Housing View will be on hiatus for the last two week of December and will resume back in January 2022.

On cross-country:

- The laws of attraction: Economic drivers of inter-regional migration, the role of housing, and public policies – VoxEU

- Affordability the casualty amid ever-climbing global property prices – Reuters

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, December 13, 2021

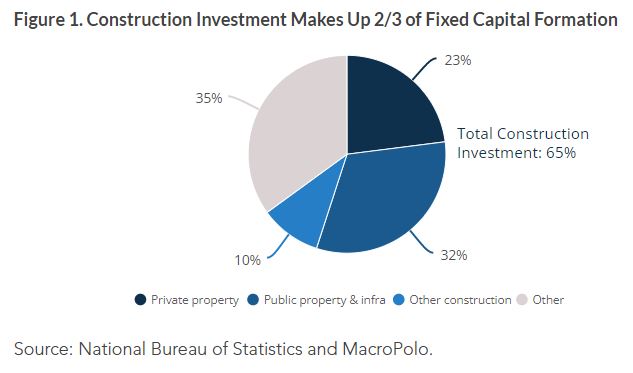

China’s Coming Property Correction: A Managed Soft Landing

From MacroPolo:

“With China’s Evergrande moving into what appears to be a managed default process, as we had previously anticipated, it’s time to look at the future of the property sector. Even without the Evergrande crisis, the property sector is bound to see a correction. The crisis simply made the writing on the wall clearer. Such a correction means that China’s notoriously outsized investment-driven model will have to be “right-sized.”

The right-sizing of investment, which mainly refers to fixed-capital formation that makes up about 43% of GDP, will inevitably hurt growth (see Figure 1). Getting a handle on the magnitude of the growth impact, therefore, will be key to any analysis of China’s economic future. To do so requires examining construction-related investment, which is composed mainly of private property investment and local government investment (including public housing and infrastructure).

Our baseline scenario assumes a 30% decline in private property construction through 2025. In total construction volume terms, that means a correction from 100 million units to roughly 70 million units. Such a correction will lead to annual property sales falling from 15% to 10% of GDP by 2025, which is basically the same level as in 2010. In other words, China intends to roll back the decade of rapid property sector growth in the next five years.

As a result, local government investment, which is basically public spending on infrastructure that depends largely on land revenue derived from private property investment, will likely decline by 3% of GDP over the same period. Combined with the property correction, we expect overall construction investment to be down by 6% of GDP.”

From MacroPolo:

“With China’s Evergrande moving into what appears to be a managed default process, as we had previously anticipated, it’s time to look at the future of the property sector. Even without the Evergrande crisis, the property sector is bound to see a correction. The crisis simply made the writing on the wall clearer. Such a correction means that China’s notoriously outsized investment-driven model will have to be “right-sized.”

The right-sizing of investment,

Posted by at 8:10 AM

Labels: Global Housing Watch

Saturday, December 11, 2021

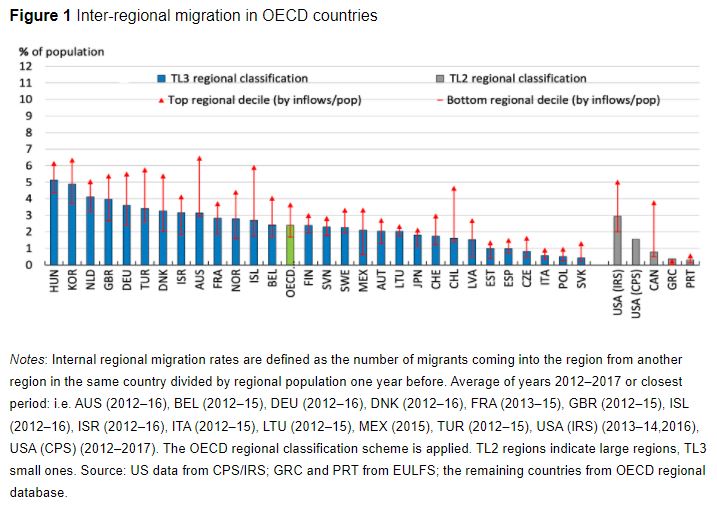

The laws of attraction: Economic drivers of inter-regional migration, the role of housing, and public policies

From a VoxEU post by Orsetta Causa, Maria Chiara Cavalleri, Michael Abendschein, and Nhung Luu:

“The capacity of workers to move regions in response to local economic shocks is a key dimension of labour market dynamism that could contribute to recovery from the COVID-19 crisis and support the green transition. This column presents new empirical evidence on how policies can shape the responsiveness of inter-regional migration to regional economic conditions, with a particular focus on housing markets, social policies, and business regulations. It highlights the need for articulating place-based policies to help prospective movers as well as stayers

Inter-regional migration can contribute to the smooth and inclusive recovery from the COVID-19 crisis (for instance, by helping to match workers and jobs) as well to the green transition (for instance, by helping labour reallocation towards low-carbon activities). Mobility across regions can also contribute to upward social mobility, for instance by allowing workers to move out of disadvantaged areas or declining sectors. While promoting mobility is not an end in itself, managing mobility is an important policy challenge, especially in countries with large and persistent spatial disparities between regions.

Recent work by the OECD (Causa et al. 2021, Cavalleri et al. 2021, OECD 2021a) examines the levels and trends of inter-regional migration within and across OECD countries. It presents novel cross-country and country-specific empirical evidence on economic and housing-related factors affecting people’s decisions to move to a different region within the same country. This work shows how policies influence the responsiveness of regional migration to regional economic conditions and shocks. It also contributes to the renewed interest in regional inequalities and placed-based policies (Siegloch et al. 2021, Ku et al. 2020, Iammarino et al. 2019).

We find that inter-regional migration varies significantly across OECD countries (Figure 1). In high-mobility countries, such as Hungary and Korea, around 5% of the population moves to another region each year. By contrast, mobility rates are below 1% in some Eastern and Southern European countries, such as Slovakia, Poland and Italy.”

Continue reading here.

From a VoxEU post by Orsetta Causa, Maria Chiara Cavalleri, Michael Abendschein, and Nhung Luu:

“The capacity of workers to move regions in response to local economic shocks is a key dimension of labour market dynamism that could contribute to recovery from the COVID-19 crisis and support the green transition. This column presents new empirical evidence on how policies can shape the responsiveness of inter-regional migration to regional economic conditions,

Posted by at 7:29 AM

Labels: Global Housing Watch

Subscribe to: Posts