Showing posts with label Global Housing Watch. Show all posts

Monday, January 10, 2022

Prime Real Estate Newsletter – January 2022

[embeddoc url=”https://unassumingeconomist.com/wp-content/uploads/2022/01/PR_2022_01-5.docx”] Read the full article…

Posted by at 4:12 PM

Labels: Global Housing Watch

Sunday, January 9, 2022

Should Blacks Apply for Mortgage Loans at the End of the Month?

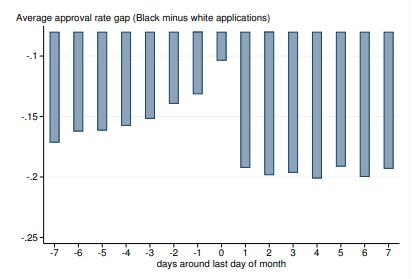

A new paper studies mortgage loan approval rates for white and blacks. “In the first seven days of the month, Black applicants have 20 percentage point lower approval rates than white applicants. The approval gap declines to just 10 percentage points on the last day the month,” as shown in the figure below. Why? The authors examine the hypothesis that this occurs because loan officers have monthly volume quotas, which gives “them less scope to apply subjective preferences” at the end of the month. They calculate “an upper bound for the costs of discrimination”: “if the Black approval gap on each day of the month was as small as it was on the last day, approximately 1.4 million more Black applicants would have been approved between 1994 and 2018,” corresponding to over $200 billion in total loan volume.

The figure reports approval rates, which we define as the fraction of loans that are originated out of the total number of applications (excluding withdrawn applications). We present the difference between the Black approval rate and the white approval rate on each day.

A new paper studies mortgage loan approval rates for white and blacks. “In the first seven days of the month, Black applicants have 20 percentage point lower approval rates than white applicants. The approval gap declines to just 10 percentage points on the last day the month,” as shown in the figure below. Why? The authors examine the hypothesis that this occurs because loan officers have monthly volume quotas, which gives “them less scope to apply subjective preferences” at the end of the month.

Posted by at 1:02 PM

Labels: Global Housing Watch

Friday, January 7, 2022

Housing View – January 7, 2022

On cross-country:

- How long can the global housing boom last? Three fundamental forces mean it could endure for some time yet – The Economist

On the US:

- ‘There may be a slight correction in pricing.’ Real estate attorneys and economists on what buyers need to know about the housing market in 2022 – Market Watch

- Home Values in Already Hot U.S. Market to Surge 14% This Year, Zillow Says. Tampa and Jacksonville in Florida and Raleigh in North Carolina are projected to be most in-demand. – Bloomberg

- Why Tampa will be 2022’s Hottest Market – Zillow

- Real estate market in 2022 will ‘remain very strong,’ expert says – Yahoo Finance

- AEI housing market indicators, December 2021 – American Enterprise Institute

- Home Ownership More Affordable Than Renting in Majority of U.S. Housing Markets – ATTOM

- What’s Going on With Housing Prices? A Deep Dive into the Discrepancy Between Home Price Indexes, Private Sector Rental Data, and Official CPI Rent Indexes – Apricitas

On China

- China Property Tax Trial Likely Delayed During Real Estate Slump – Bloomberg

On other countries:

- [Australia] As stimulus wanes, focus on productivity and house prices – Financial Review

- [Australia] Australia Housing Boom Fades as Melbourne, Sydney Pull Back – Bloomberg

- [Australia] Australia’s housing market faces headwinds as supply likely to outpace demand, analysts say – South China Morning Post

- [Ireland] The impact of COVID-19 on house prices in Northern Ireland: price persistence, yet divergent? – Journal of Property Research

- [New Zealand] New Zealand Average Home Price Exceeds NZ$1 Million for First Time – Bloomberg

- [Taiwan] Taiwan Central Bank Split on Using Rates to Rein in Housing Market – Bloomberg

On cross-country:

- How long can the global housing boom last? Three fundamental forces mean it could endure for some time yet – The Economist

On the US:

- ‘There may be a slight correction in pricing.’ Real estate attorneys and economists on what buyers need to know about the housing market in 2022 – Market Watch

- Home Values in Already Hot U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, January 4, 2022

How long can the global housing boom last?

From The Economist:

“The IMF’s global house-price index, expressed in real terms, is well above the peak reached before the 2007-09 financial crisis. American housebuilders’ share prices are up by 44% over the past year, compared with 27% for the overall stockmarket. Estate agents from Halifax’s mom-and-pop shops to the supermodel lookalikes on Netflix’s “Selling Sunset”, in Los Angeles, have never had it so good.

Now people are wondering whether the party is about to end. Governments are winding down stimulus. People no longer have so much spare cash to splurge on property, now that foreign holidays are back and restaurants are open. Central banks, worried about surging inflation, are tightening monetary policy, including by raising interest rates. In its latest financial-stability report the IMF warned that “downside risks to house prices appear to be significant”, and that, if these were to materialise, prices in rich countries could fall by up to 14%. In New Zealand, where prices have risen by 24% in the past year, the central bank is blunter. The “level of house prices”, it says, is “unsustainable”.

But is it? (…)

Fundamental forces may once again explain why house prices today are so high—and why they may endure. Three reasons stand out: robust household balance-sheets; people’s greater willingness to spend more on their living arrangements; and the severity of supply constraints.”

From The Economist:

“The IMF’s global house-price index, expressed in real terms, is well above the peak reached before the 2007-09 financial crisis. American housebuilders’ share prices are up by 44% over the past year, compared with 27% for the overall stockmarket. Estate agents from Halifax’s mom-and-pop shops to the supermodel lookalikes on Netflix’s “Selling Sunset”, in Los Angeles, have never had it so good.

Now people are wondering whether the party is about to end.

Posted by at 8:11 PM

Labels: Global Housing Watch

Sunday, December 19, 2021

Where Can Residential Real Estate Investors Find the Most Potential ROI?

From First American:

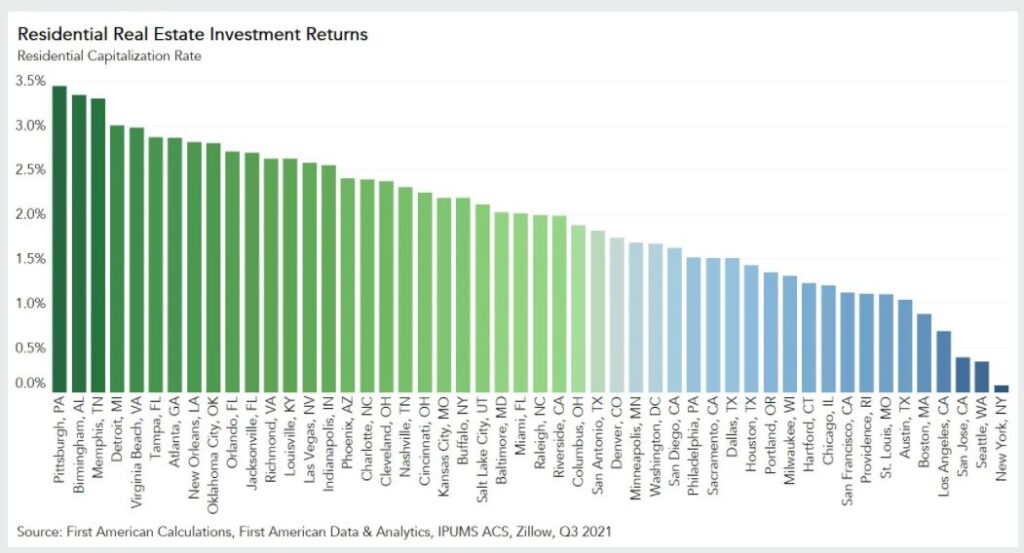

“Over the past year, increasing investor activity in residential real estate, particularly in single-family homes, has drawn a lot of attention. News of large institutional investors snapping up single-family homes underscored this summer’s historically hot housing market. Investors now own an estimated 2 percent of single-family rental housing units in the U.S., but investor activity varies significantly across markets. Adapting a metric commonly used for measuring the return on investment for commercial real estate can help identify the most attractive markets for residential real estate investors.

Housing’s Investment Return

Investors in commercial real estate often use a concept called the capitalization rate (cap rate) to calculate their potential rate of return on a real estate investment. The cap rate measures the net operating income of a property – its rental income less any operating costs, such as property taxes, insurance, and maintenance and repair costs – compared to the value of the property. Similar to the yield on a bond or the rate of return on an investment, the higher the cap rate, the more profitable the investment. While commonly calculated for commercial real estate transactions, it can be applied to residential real estate as well.

To calculate the typical market-level residential cap rate, take the median residential market rent and assume that the property will be vacant for three of the 12 months of the year (the typical vacancy assumption mortgage lenders use when underwriting a residential investment property), leaving an investor with nine months of collected rent. After accounting for property costs – property taxes, maintenance costs and annual homeowner’s insurance premium – we are left with estimated total rental income. Dividing the estimated total rental income by the median home sale price in each market yields a residential cap rate.

Which Markets Offer the Highest Return?

Breaking down the cap rate for the median single-family home in each of the top 50 U.S. markets reveals the residential housing markets that are potentially the most profitable from a real estate investment perspective. Of the top 50 U.S. markets, the five markets with the highest cap rates in the third quarter of 2021 were Pittsburgh (3.4 percent), Birmingham, Ala. (3.3 percent), Memphis, Tenn. (3.3 percent), Detroit (3 percent), and Virginia Beach, Va. (3 percent). The five markets with the lowest cap rates were New York (0.1 percent), San Jose, Calif. (0.3 percent), San Francisco (0.4 percent), Los Angeles (0.7 percent), and Boston (0.9 percent).”

Continue reading here.

From First American:

“Over the past year, increasing investor activity in residential real estate, particularly in single-family homes, has drawn a lot of attention. News of large institutional investors snapping up single-family homes underscored this summer’s historically hot housing market. Investors now own an estimated 2 percent of single-family rental housing units in the U.S., but investor activity varies significantly across markets. Adapting a metric commonly used for measuring the return on investment for commercial real estate can help identify the most attractive markets for residential real estate investors.

Posted by at 9:14 AM

Labels: Global Housing Watch

Subscribe to: Posts