Showing posts with label Global Housing Watch. Show all posts

Wednesday, February 16, 2022

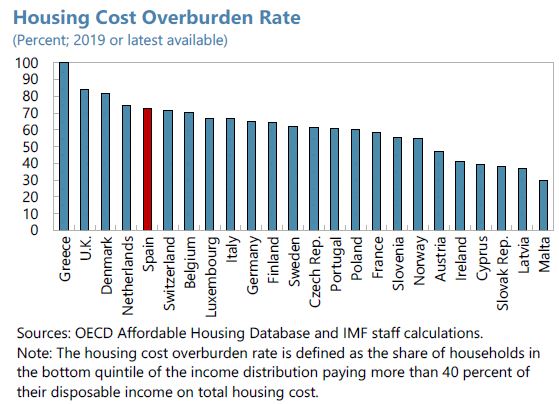

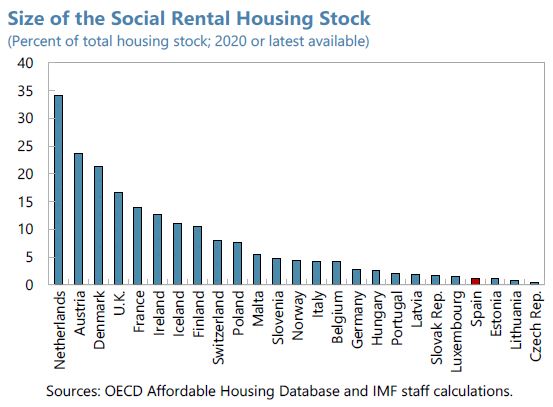

Housing Market in Spain

From the IMF’s latest report on Spain:

“Continued efforts to address housing affordability challenges would support growth, facilitate labor mobility across regions and reduce inequality. Prior to the pandemic, limited rental housing supply hampered by relatively inefficient building regulations contributed to a surge in rental prices, creating affordability problems and limiting labor mobility (especially for young people and other vulnerable groups). The draft housing law and the national housing plan aim to address the existing challenges. To limit increases in rent prices in stressed areas, the law introduces rent caps on large landlords and tax incentives for small landlords to keep rents low. While these may benefit tenants in the short term, rent caps could introduce inefficiencies and restrict the availability of properties for future tenants. Further evaluation of these measures would be useful to gauge their impact. The envisaged targeted rent support programs for vulnerable groups are welcome. However, they should be combined with effective supply measures to avoid further pressures on rent prices. The increase of taxes on empty properties and the expansion of the social housing stock, which are contemplated in the proposed reform, should help increase rent supply. The RTRP envisages €1 billion for the construction of new public social rental dwellings in 2022–23. Additional policies to increase housing supply could include simplifying land use regulations and accelerating licensing processes at the regional government level.”

From the IMF’s latest report on Spain:

“Continued efforts to address housing affordability challenges would support growth, facilitate labor mobility across regions and reduce inequality. Prior to the pandemic, limited rental housing supply hampered by relatively inefficient building regulations contributed to a surge in rental prices, creating affordability problems and limiting labor mobility (especially for young people and other vulnerable groups). The draft housing law and the national housing plan aim to address the existing challenges.

Posted by at 11:44 AM

Labels: Global Housing Watch

Saturday, February 12, 2022

Vulnerabilities in the residential real estate sectors of the EEA countries

From European Systemic Risk Board:

“In this report, the ESRB presents its medium-term assessment of vulnerabilities relating to the RRE sector across the EEA countries. In carrying out this assessment, the ESRB first performed an analysis of vulnerabilities across the EEA countries. For the 24 countries for which the vulnerabilities identified were more pronounced, an in-depth analysis was conducted. This analysis pointed also to the need to take into account or change other than macroprudential policies, for example by changing tax incentives or increasing the housing supply. A similar assessment was conducted by the ESRB in 2019, when 11 countries received either ESRB recommendations (Belgium, Denmark, Finland, Luxembourg, Netherlands and Sweden) or warnings (Czech Republic, Germany, France, Iceland and Norway).

The risk assessment concluded that, in five countries which received ESRB recommendations or warnings in 2019 (Denmark, Luxembourg, Netherlands, Norway and Sweden) the vulnerabilities relating to residential real estate markets remained high, while in six countries (Belgium, Czech Republic, Germany, Finland, France and Iceland) the vulnerabilities were assessed as medium. Among other EEA countries, 13 (Austria, Bulgaria, Estonia, Croatia, Hungary, Ireland, Liechtenstein, Lithuania, Malta, Poland, Portugal, Slovenia and Slovakia) were identified as facing medium risks.

The policy assessment found that in five countries which received ESRB recommendations or warnings in 2019 (Belgium, Czech Republic, France, Iceland and Norway), policies were assessed as appropriate and sufficient to mitigate the vulnerabilities identified. In two countries (the Netherlands and Sweden), policies were assessed as being appropriate but partially sufficient, while in four of the countries (Germany, Denmark, Finland and Luxembourg), policies were assessed as partially appropriate and partially sufficient. Among the rest of the EEA countries analysed in this report, in one country (Slovakia) policies were identified as appropriate and partially sufficient, while in five countries (Austria, Bulgaria, Hungary, Croatia and Liechtenstein) policies were found to be partially appropriate and partially sufficient.

In countries in which the policies were assessed as only partially sufficient to mitigate the identified vulnerabilities, the ESRB suggested various macroprudential measures to be considered by the national authorities. In particular, the ESRB pointed out that a number of countries should either introduce additional borrower-based measures or tighten existing ones to mitigate the existing vulnerabilities more effectively or prevent a further build-up of vulnerabilities. Countries with accumulated vulnerabilities should also ensure that capital is preserved until a possible materialisation of risks or consider (re)introducing capital-based measures once the economic recovery is on a firm footing. However, taking into account the economic uncertainty related to the pandemic, any policy actions should be carefully assessed to ensure that they contribute towards mitigating RRE vulnerabilities, while aiming to avoid procyclical effects on the real economy and the financial system. In the near term, it is particularly important for all countries that banks make adequate provision for expected losses. Finally, the analysis notes that, in some countries in which the systemic risk levels identified remain high, interventions in other policy areas may be required to complement macroprudential policy.”

From European Systemic Risk Board:

“In this report, the ESRB presents its medium-term assessment of vulnerabilities relating to the RRE sector across the EEA countries. In carrying out this assessment, the ESRB first performed an analysis of vulnerabilities across the EEA countries. For the 24 countries for which the vulnerabilities identified were more pronounced, an in-depth analysis was conducted. This analysis pointed also to the need to take into account or change other than macroprudential policies,

Posted by at 6:29 AM

Labels: Global Housing Watch

Friday, February 11, 2022

Housing View – February 11, 2022

On cross-country:

- Property ladder too high for central Europe’s first-time buyers – Reuters

On the US:

- The Housing Boom May Be About to Go Bust. A new generation of buyers is jumping into the market at what may be the worst possible time. – Bloomberg

- The Housing Party Is Starting to Wind Down. Builders are ramping up supply just as a record low percentage of Americans say it’s a good time to buy a home. – Bloomberg

- In Covid-19 Housing Market, the Middle Class Is Getting Priced Out. Surging demand and shrinking supply combine to make home buying more difficult, as affordability worsens for many – Wall Street Journal

- It’s Time to Put Cities at the Top of America’s Economic Agenda. The U.S. economy today is actually a collection of regional economies. We need a national place-based strategy that recognizes local differences. – Bloomberg

- National and Metro Housing Market Indicators – AEI

- Zillow: Our 2022 housing forecast is way off—home prices now set to spike 16% – Fortune

- Inequality in the Time of COVID-19: Evidence from Mortgage Delinquency and Forbearance – Philadelphia Fed

- Is the ‘American Dream’ of Homeownership a False Promise? In “Owned: A Tale of Two Americas,” director Giorgio Angelini traces the origins of a discriminatory housing market. – Bloomberg

- Record-High Prices and Record-Low Inventory Make It Increasingly Difficult to Achieve Homeownership, Particularly for Black Americans – NAR

- Want Affordable Housing? Strengthen Regional Governments. Most Americans live in metropolitan areas, and it takes a metropolitan regional government to coordinate the growth in housing, transit, and employment that makes the region livable. – The American Prospect

- The Housing Situation Is Dire. But Progress Is Still Possible. In the South Bronx, developers found ways to build an array of sleek, affordable apartments in two subsidized housing developments. Is this a way forward? – New York Times

- There are hardly any houses left to buy – Axios

- US Housing Supply Gap Expands in 2021 – Realtor.com

- Diverse neighborhoods are made of diverse housing – Brookings

- U.S. Housing Costs Surge, With No End In Sight. Locked out of the supply-constrained home-buying market, more households are crowding the rental market, driving up rents and stressing housing support programs. – Bloomberg

- How Rent Hikes Make Buying a House Even Harder. Rising rents are pushing many to buy a home even if the housing market is already tough – Wall Street Journal

- Where Are Rents Rising the Most? In 2021, rents rebounded from pandemic lows in nearly all of the 100 largest American cities. – New York Times

- What Freddie Mac is Doing About the Rental Affordability Crisis – Freddie Mac

- Millennial Demand is Driving up Prices in Family-Friendly Neighborhoods – Zillow

- How strip malls could help solve the housing shortage. There’s a lot of space for apartments above the commercial real estate on main suburban streets – Fast Company

- California’s Free-Market Housing Fix. A new state law allows landowners to build four units on most lots zoned currently for one unit. – Wall Street Journal

- They Rushed to Buy in the Pandemic. Here’s What They Would Change. A frenzied sellers’ market led some people to make harried decisions when buying their homes that they now regret. – New York Times

- Homeownership in old age and at the time of death – Economics Letters

- How New York’s housing market got even more ridiculous. For a brief moment, dream apartments seemed possible – but then it all came crashing down – The Guardian

- American Protectionism and Construction Materials Costs. Tariffs imposed by the U.S. government on materials used by the domestic construction sector cause a significant increase in the cost of those goods. – Cato Institute

- The Sustainable City Podcast: Where the Suburbs End. Join us as we discuss California’s audacious effort to deconstruct single-family zoning – New York Times

On China

- Chinese property group Shimao feels chill of sector’s liquidity crisis. Developer sucked into bond market sell-off following Evergrande collapse – FT

- China’s Taking on a Risky Bubble Deflation Experiment. Property investors, like Wile E. Coyote, may feel wobbly if they look down. – Bloomberg

- China Eases Property Loan Curbs as Housing Market Slumps. Loans to fund public rental housing become exempt from limits. PBOC’s move is latest softening of real estate clampdown – Bloomberg

On other countries:

- [Canada] Canadians Deepen Faith in Red-Hot Housing While Rate Hikes Loom. 64% expect real-estate prices to rise over next half year. Jump in sentiment comes amid central bank, regulatory warnings – Bloomberg

- [Iceland] Europe’s Hottest Housing Boom May Prompt Bigger Hike in Iceland. Central bank might raise key interest rate by 0.75% this week. House prices on Atlantic island have risen 150% since 2010 – Bloomberg

- [United Kingdom] Why are there so few homes for sale in the UK? A supply crunch has left many prospective buyers struggling to find the right property – FT

- [United Kingdom] Most Tory voters want more affordable housing stock, finds poll. YouGov study also finds most Conservative supporters in favour of higher taxes on second homes – The Guardian

- [United Kingdom] Residential rents rise at fastest pace in 13 years. Tenants under pressure to find affordable urban homes as workplaces reopen – FT

- [United Kingdom] U.K. Builder Says House Prices Outpacing Cost-Inflation Surge – Bloomberg

- [United Kingdom] These Are Britain’s Property Hotspots. The North-South divide is stark in a new analysis of property price growth over the past decade, with southern England values almost doubling in several places. – Bloomberg

On cross-country:

- Property ladder too high for central Europe’s first-time buyers – Reuters

On the US:

- The Housing Boom May Be About to Go Bust. A new generation of buyers is jumping into the market at what may be the worst possible time. – Bloomberg

- The Housing Party Is Starting to Wind Down. Builders are ramping up supply just as a record low percentage of Americans say it’s a good time to buy a home.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, February 8, 2022

Residential mobility and unemployment in the UK

From a new paper by Monica Langella and Alan Manning:

“The UK has suffered from persistent spatial differences in unemployment rates for many decades. A low responsiveness of internal migration to unemployment is often argued to be an important cause of this problem. This paper uses UK census data to investigate how unemployment affects residential mobility using small areas as potential destinations and origins and four decades of data. It finds that both in- and out-migration are affected by local unemployment – but also that there is a very high ‘cost of distance’, so most moves are very local. We complement the study with individual longitudinal data to analyse individual heterogeneities in mobility. We show that elasticities to local unemployment are different across people with different characteristics. For instance, people who are better educated are more sensitive, the same applies to homeowners. Ethnic minorities are on average less sensitive to local unemployment rates and tend to end up in higher unemployment areas when moving.”

From a new paper by Monica Langella and Alan Manning:

“The UK has suffered from persistent spatial differences in unemployment rates for many decades. A low responsiveness of internal migration to unemployment is often argued to be an important cause of this problem. This paper uses UK census data to investigate how unemployment affects residential mobility using small areas as potential destinations and origins and four decades of data. It finds that both in- and out-migration are affected by local unemployment –

Posted by at 11:13 AM

Labels: Global Housing Watch

Friday, February 4, 2022

Housing View – February 4, 2022

On cross-country:

- Housing Returns in Big and Small Cities – New York Fed

- Large investors drive up house prices in Europe’s cities, study finds. Housing is increasingly attractive asset for institutional investors due to near zero interest rates – The Guardian and link to report

- Crypto Kings Are the Real-Estate Industry’s Newest Whales. People who have made fortunes investing in digital currency, or who helped build the vast crypto industry, are the new darlings of the high-end residential property market – Wall Street Journal

- Real estate prices are rising at record speed in US, UK and Australia, as WFH and the pandemic pushed families out of big cities in 2021 – are new homes still a good investment? – South China Morning Post

On the US:

- How the Fed’s Policy Shift Is Rippling Through the Housing Market. The central bank had been the biggest buyer of mortgage bonds, but now it is stepping back and borrowing costs are rising – Wall Street Journal

- Wonking Out: Are We in Another Housing Bubble? – New York Times

- Why, and Where, are Housing Prices Rising? – Econofact

- The Simple Reason Why So Many Can’t Afford Housing – Barron’s

- It’s Harder to Find a Home Than Love When Housing Markets Are This Hot. Bidding wars, low inventory and huge price hikes have turned homebuying into an ordeal for many house hunters over the past two years. – Bloomberg

- Would Housing Cost Less If It Were Easier to Build New Homes? Surprisingly, Not Much. A new study suggests that supply and demand are only part of a complex problem – Kellogg Insight

- New York’s ideas for zoning reform offer many paths to tackling the housing crisis – Brookings

- Newly Built Homes Make Up Record Share of U.S. Housing Supply – Bloomberg

- Rents are up 40 percent in some cities, forcing millions to find another place to live – Washington Post

- Wall Street’s $85 Billion Housing Bet Intensifies U.S. Land Boom. Investors are snapping up lots to build an empire of suburban rental homes. – Bloomberg

- What Financial Resources Have Renters Tapped During the Pandemic? – Harvard Joint Center for Housing Studies

- Report: Owning more affordable than renting in most housing markets – Washington Post

- December Rental Data: Rents Surged by 10.1% in 2021 – Realtor.com

- The Record-Breaking Rental Market – Harvard Joint Center for Housing Studies

- ‘It’s anguish, it’s pain, it’s agony’ – here’s what it’s like to shop for a home in today’s tight housing market – CNBC

- Measuring America’s Affordability Problem: Comparing Alternative Measurements of Affordable Housing – Housing Policy Debate

- When Will Be a Good Time to Buy a House? There won’t be a perfect moment anytime soon—but that shouldn’t stop you if you’re ready. – The Atlantic

- AEI housing market indicators, January 2022 – AEI

- Where to build in a state on fire? California housing projects face growing challenges – The Guardian

- Regulation and the Housing Affordability Crisis. Government regulations account for nearly 25% of the price of building a single-family home. – Wall Street Journal

- Why Are Residential Property Tax Rates Regressive? – Federal Reserve Bank of Philadelphia

- Q4 Homeownership Rate Reflects Slight Growth, Demographic Disparities – Realtor.com

- Exploring Climate Change in U.S. Housing Policy – Housing Policy Debate

- The Role of 421-a during a Decade of Market Rate and Affordable Housing Development – NYU Furman Center

On China

- Beijing has shortcut to prop up real estate – Reuters

- Understanding the Resurgence of the SOEs in China: Evidence from the Real Estate Sector – NBER

- China Home Sales Slump Deepened in January in Blow to Economy – Bloomberg

On other countries:

- [Australia] Regional house prices surge as Melburnians flood coastal and tree-change hotspots – The Sydney Morning Herald

- [Australia] Australia Home Prices Edge Up, Further Sign of Cooling Boom – Bloomberg

- [Brazil] The financialisation of housing by numbers: Brazilian real estate developers since the Lulist era – Housing Studies

- [Canada] This is what a rate hike will cost homeowners – Globe and Mail

- [Canada] Bank of Canada ‘no hike’ leaves housing fire burning, say market watchers – Reuters

- [Canada] Housing Market in a ‘Speculative Fever,’ Canada Regulator Says – Bloomberg

- [Israel] New plan aims to entice cities to construct housing with NIS 60 million bait. To resolve housing crisis, government will reward 12 high-demand municipalities with cash for each apartment approved; project could add 30,000 new units in the next three years – The Times of Israel

- [Netherlands] Sentiment in the Housing Market – University of Groningen

- [Singapore] Singapore House Prices Surge Most in Decade as Curbs Test Market – Bloomberg

- [Spain] Housing prices in Spain: convergence or decoupling? – Central Bank of Spain

- [Spain] Spain’s new “right to housing” law enshrines rent control nationwide – Quartz

- [Switzerland] Swiss banks criticise steps to cool runaway property market – Reuters

- [United Kingdom] Demand Is Surging for Flats Outside London. Price increases for apartments have been relatively modest compared to other types of property, according to Zoopla. – Bloomberg

- [United Kingdom] The plight of the UK’s first-time buyers. The immediate pressures of the pandemic may have eased, but prospective homeowners must now contend with record prices and a looming cost of living crisis – FT

- [United Kingdom] Failure to help struggling households will cost Tories dear. Rising housing and energy costs plus higher taxes mean ministers have to come up with something – The Guardian

- [United Kingdom] UK homeowners secure £800bn windfall with house price rise. Average property values increased more than 10 per cent last year, according to new analysis – FT

- [United Kingdom] UK house prices show strongest start to year since 2005. Property price index rises by annual rate of 11.2% in January surpassing economists’ expectations – FT

- [United Kingdom] Mortgage lenders cut 10-year fixed rates ahead of Bank rate decision. Borrowers seeking long-term fixed-rate loans amid rising rates and inflation – FT

On cross-country:

- Housing Returns in Big and Small Cities – New York Fed

- Large investors drive up house prices in Europe’s cities, study finds. Housing is increasingly attractive asset for institutional investors due to near zero interest rates – The Guardian and link to report

- Crypto Kings Are the Real-Estate Industry’s Newest Whales. People who have made fortunes investing in digital currency,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts