Showing posts with label Global Housing Watch. Show all posts

Tuesday, March 29, 2022

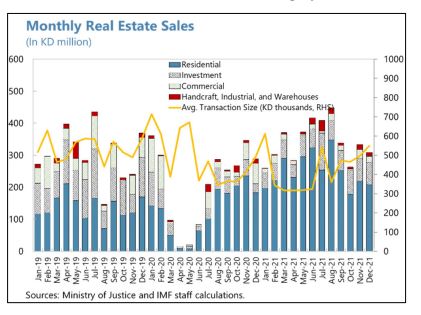

Housing Market in Kuwait

From the IMF’s latest report on Kuwait:

“The residential real estate market quickly recovered, but investment and commercial real estate continue to lag. The value of real estate transactions stalled at the onset of the pandemic but strongly recovered thereafter, driven by favorable financing conditions. Residential sales recovered faster than investment and commercial components, which lag in the volume and value of transactions. Average transaction value has been volatile but trending up in recent months.”

From the IMF’s latest report on Kuwait:

“The residential real estate market quickly recovered, but investment and commercial real estate continue to lag. The value of real estate transactions stalled at the onset of the pandemic but strongly recovered thereafter, driven by favorable financing conditions. Residential sales recovered faster than investment and commercial components, which lag in the volume and value of transactions. Average transaction value has been volatile but trending up in recent months.”

Posted by at 5:28 PM

Labels: Global Housing Watch

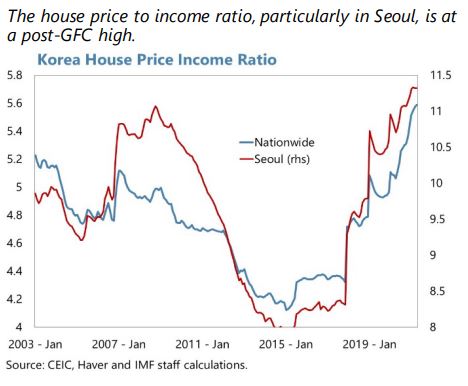

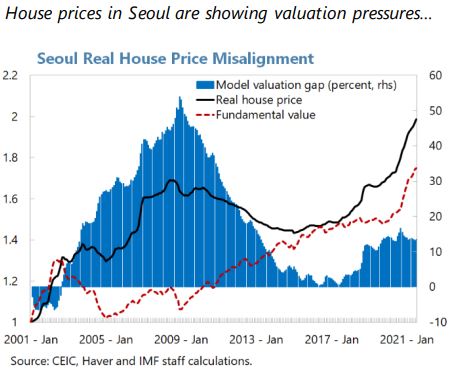

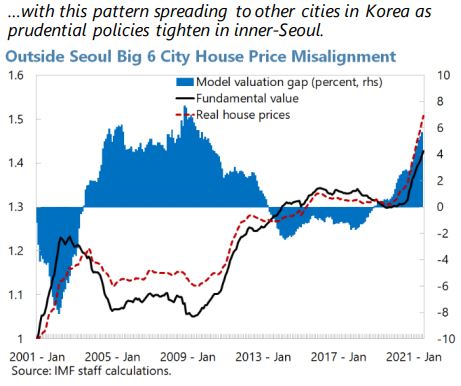

Housing Market in Korea

From the IMF’s latest report on Korea:

“The pandemic magnified a chord of pre-COVID trends that included rising of already elevated household debt and rapid house price growth, raising macro-financial risks and social tension. These trends require coordinated policy action, including tightening of borrower-based macroprudential policies, raising real-estate taxes, and housing supply.

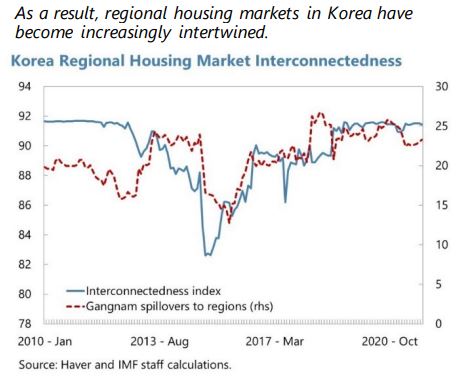

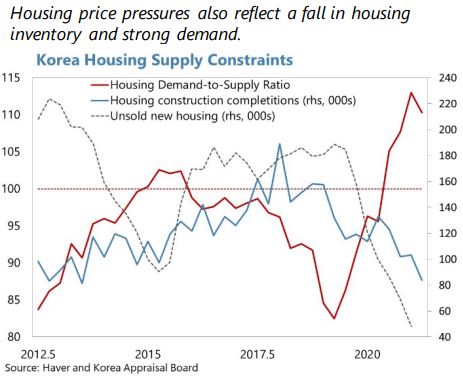

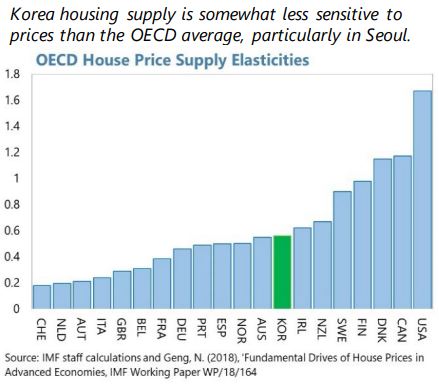

Real estate prices grew at an unprecedented rate during the pandemic, with the house price-to-income ratio at a multi-decadal high. Since the pandemic the confluence of a decline in mortgage rates, shifts in household formation, and longer-term structural factors linked to demography has fueled rapid growth in house prices. The strong real-estate demand surpassed new housing supply that has come on the market in recent years, particularly in Seoul. Historically low mortgage rates have fueled speculative behavior in the housing market, with house prices in the major cities now showing significant valuation pressures (Annex VIII and Figure 10). Prices have also significantly outpaced wages and widened inequality. House price growth is beginning to slow on the back of tighter prudential and monetary policies, but affordability will remain a concern going forward.

While housing supply has expanded in recent years, it has been surpassed by strong housing demand since the pandemic. Housing supply has grown by 30 percent in Seoul over the last decade, but the home ownership ratio remains relatively unchanged and lower than peer countries. To continue improving supply and improve affordability, particularly in urban areas, a number of welcome measures have been introduced: the easing of brownfield density restrictions for redevelopment projects; a fast track one-stop review process for redevelopment projects; allowance of pre- pre-sale of new apartments to facilitate housing access to first-time buyers. 10 Efforts are also underway to upgrade transportation links to greenbelt developments on the outskirts of Seoul. Over the medium term, the supply of new dwellings will need to consider Korea’s projected decline in population to avoid the potential risk of boom-bust cycles in the housing market.

Real-estate demand drove very strong growth in household debt during the pandemic, but vulnerabilities are mitigated. The tight borrower-based macroprudential stance has supported low NPLs and debt servicing ratios, and lending remains concentrated among high credit score individuals (Figure 11). Moreover, average LTVs are around 40 percent and household income is expected to remain stable which further contains balance sheet risks (Figure 12). FSAP and more recent Bank of Korea stress tests—applying a more severe economic shock than the pandemic downturn—showed that risks from household balance sheets are contained.

Some post-pandemic household lending developments may pose risks going forward. In contrast to pre-COVID trends, a larger share of new bank loan origination has been unsecured lending linked to floating interest rates, which is being used to top up lending and meet tight LTV requirements. There has also been strong growth in bullet loans, linked to the Jeonse market, which raises rollover risks. In turn, some subprime borrowers are resorting to non-banks to increase their financing. This suggests that borrower-based restrictions have been effective, but some mortgage prudential requirements can be circumvented. Moreover, while lending is concentrated among high credit score individuals, credit risks from the uplift in scores is susceptible to economy-wide credit cycles.

Household assets are concentrated in real-estate and closely intertwined with demographic challenges, which may also pose risks going forward. Korean households tend to self-insure for retirement by accumulating real-estate over their life cycle; the equity of which could be withdrawn in the reverse mortgage market. 12 Therefore, unlike in other advanced economies, engagement with the credit market does not decline with age.13 These risks could be further exacerbated in the future by the rapid demographic transition in Korea. 14 On both the assets (via real estate investment) and liabilities side (via Jeonse deposit), Korea household balance sheets are significantly exposed to real estate price fluctuations when compared to other advanced economies.

Policy Package to Contain Vulnerabilities

Given rising risks, housing and household debt vulnerabilities need to be closely managed. With due consideration on financial inclusion, a broad package of policies could help reduce financial risks from housing and household debt:

Macroprudential policies. Borrower-based prudential measures have been effective and recent measures, including the individual based DSR ceiling, are welcomed. 16 However, some prudential requirements on mortgage are being circumvented. Additional measures may be required, as recommended in the 2020 FSAP, including: (i) a sectoral counter cyclical capital buffer (sCCyB) to ensure banking sector resilience; (ii) introducing a stressed DSR ratio to moderate borrowing risk in the event there is a snapback in lending rates; (iii) formalizing the unsecured debt-to-annual income ratio ceiling that is currently a supervisory recommendation for both banks and nonbanks, (iv) incentivizing banks to lower the share of new unsecured floating rate lending via higher risk weights applied to unsecured loans. 17 The authorities should also review remaining gaps in lending-related regulations between banks and non-banks (e.g., DSR ceilings and loan-to-deposit ratio prudential requirements) to avoid individuals borrowing from multiple institutions to circumvent mortgage prudential requirements.

Tax policies: Tax measures implemented to contain housing demand include raising the Comprehensive Real Estate Holding Tax (CRET) for multiple-home owners and a transfer tax on short-term capital gain. The effectiveness of these measures should continue to be assessed against housing market outcomes. The higher CRET likely helped to expand supply by raising the holding costs for multiple-home owners, which could be broadened and raised to foster increased supply. However, the capital gains tax hike on multiple-home owners, while designed to reduce speculative demand, may have also reduced existing-housing supply, at least in the short term, by disincentivizing multiple-home owners from selling real-estate and should be reassesed as experience on its effectivenes is gained.

Housing supply. Current market valuations provide strong incentives for private sector developers to expand the supply of dwellings. However, private sector incentives are distorted by the regulatory and tax treatment of real estate, including price caps on new pre-construction apartment sales and excess capital gains on redevelopment projects, which should be reviewed to increase private housing supply. Moreover, further efforts should be made to accelerate the process of repurposing commerical land to residential usage in urban areas through encouraging greater coordination between governmental agencies and local councils. In this regard, the setting up of a public private task force composed of the Ministry of Land and Infrastructure, local governments, and industry is welcome.

A combination of housing supply measures and higher property taxes would help contain housing prices over the medium-term. Staff analysis suggests that reforms that increase the elasticity of the supply of housing and higher property taxes would result in lower nationwide house prices (with the impact likely to be greater in Seoul).19 A combined policy package, together with the normalization of monetary policy conditions, would strengthen the effectiveness of these measures to reduce the growth of housing prices over the medium-term.

Authorities’ Views

(…)

The authorities view raising housing supply, particularly in Seoul, as an important step in making housing more affordable. The government announced a ‘30-80 plus’ project that aims to increase housing supply by 300 thousand homes in Seoul and 800 thousand homes nationwide over the next decade. While focusing on easing of building codes to accelerate the overall housing supply, the government will first increase the supply of office-tel apartments, which can be built more speedily due to a less onerous building code. The government will also directly purchase 35 thousand new development properties in Greater Seoul that will be repurposed as rental housing for lower income households. Reforms have also focused on increasing private sector engagement by raising the cap on loans to finance housing projects. The authorities are also reviewing stronger financial support for small and mid-sized construction companies by alleviating construction prerequisites for project financing loan guarantees. The authorities do not share staff’s view that the capital gains tax hike may have reduced housing supply, as the number of housing units for sale began to rise in September 2021 after a temporary decline since June.

The authorities deem the pre-sale apartment price and excess gain caps as necessary to maintain house price affordability. The authorities view the price cap as stabilizing house prices for actual buyers. Increasing the ceiling of pre-sale apartment prices would fuel inflation in existing apartments in the surrounding area. The excess gain cap is required to ensure that the gains of private sector led redevelopment contribute to the public good.”

From the IMF’s latest report on Korea:

“The pandemic magnified a chord of pre-COVID trends that included rising of already elevated household debt and rapid house price growth, raising macro-financial risks and social tension. These trends require coordinated policy action, including tightening of borrower-based macroprudential policies, raising real-estate taxes, and housing supply.

Real estate prices grew at an unprecedented rate during the pandemic, with the house price-to-income ratio at a multi-decadal high.

Posted by at 5:23 PM

Labels: Global Housing Watch

Friday, March 25, 2022

What Have They Been Thinking? Homebuyer Behavior in Hot and Cold Markets – A Ten-Year Retrospect

From a new paper by Robert J. Shiller and Anne K. Thompson:

“Questionnaire surveys undertaken in 1988 and annually from 2003 through 2021 of recent homebuyers in each of four U.S. metropolitan areas shed light on their expectations and reasons for purchasing during the housing boom, collapse and recovery. We find that homebuyers were generally well informed, and that their short-run expectations if anything underreacted to the year-to-year change in actual home prices. Housing bubbles can be seen in their long-term (annualized 10-year) home price expectations, the long boom that preceded the 2007-09 crisis was associated with changing public understanding of speculative bubbles. During the early years of this decade-long rebound both short and long-term expectations were out of line with actual changes in prices. Since 2014 long-term expectations have converged with short term expectations and actual price changes and all three series have moved in synch. With the onset of Covid-19, actual and anticipated appreciation diverged once again. Buyers presumed a coming slowdown in the market that has yet to materialize.”

Also see summary of the paper, presentation, and discussion of the paper by Adam Guren and Joseph Gyourko.

From a new paper by Robert J. Shiller and Anne K. Thompson:

“Questionnaire surveys undertaken in 1988 and annually from 2003 through 2021 of recent homebuyers in each of four U.S. metropolitan areas shed light on their expectations and reasons for purchasing during the housing boom, collapse and recovery. We find that homebuyers were generally well informed, and that their short-run expectations if anything underreacted to the year-to-year change in actual home prices.

Posted by at 7:15 AM

Labels: Global Housing Watch

Housing View – March 25, 2022

On cross-country:

- Could housing crack before inflation does? And a contrarian view on oil – FT

On the US:

- The Red Hot Housing Market: the Role of Policy and Implications for Housing Affordability – Fed

- Biden administration to fight racial bias in U.S. real estate appraisals – Reuters

- Treasury Shifts $377 Million Among States as Pandemic Housing Aid Dries Up. The Biden administration pulled back the aid from states and counties with unspent funds and diverted it to four states pressing for more: California, New York, New Jersey and Illinois. – New York Times

- Warning lights start to flash on US housing – ING

- Housing finance reform: The path forward gets rolling – Brookings

- Houses and Cars Have Taken Over the Economy. People are milking both bubbles for cash while the sun shines. – Bloomberg

- Falling home prices? It’s only likely in these 13 housing markets, says CoreLogic – Fortune

- How the pandemic housing market spurred buyer’s remorse across America – NPR

- What’s Driving Home Price Growth in 2022? The housing market has been red hot, but if you’re looking to buy in 2022, there is good news: the market may cool down slightly. – Freddie Mac

- Housing Crunch Turns Employers Into Landlords. It’s a new twist on the old concept of company towns. “If you call anybody, they’re all buying houses for their staff,” says Kim Jensen, a Wisconsin restaurateur. – Bloomberg

- When It Comes to Inflation, Our Focus Should Be On the Cost of Housing. The Federal Reserve is raising interest rates — but Congress has a chance to bring real relief. – Politico

- There still aren’t enough houses – Axios

- Can We Untie Real Estate and Employment? – The Big Picture

- San Francisco Rents Barely Changed During Covid Housing Boom. NYC also saw modest rent growth, at about 4%: Zillow data. Renters in major cities still pay well above national average – Bloomberg

- Billionaire MacKenzie Scott gives $436m for US affordable housing. Scott, who was formerly married to Jeff Bezos, is part of group of billionaires promising to donate more than half their wealth – The Guardian

- Key facts about housing affordability in the U.S. – Pew Research Center

- The US’s top housing authority just declared housing a human right – Quartz

- The real estate evangelist — why buy one home when you can buy 100? – FT

On China

- China Says Housing Prices Are Stable, but Developers See Significant Declines. One reason for diverging picture is the composition of the official data, economists and analysts say – Wall Street Journal

On other countries:

- [Australia] Early Signs Point to Downturn in Sydney Property Prices After 27% Rise – Bloomberg

- [Australia] Interest rate rise threatens Australia’s booming housing market. Owners rush to cash in as prices in even sleepy towns rocket after city residents search for more space – FT

- [Germany] What Is Adler and Why Is It Fueling Fears About Real Estate? – Bloomberg

- [United Arab Emirates] Dubai Property Market Set to Consolidate 2021 Gains, S&P Says – Bloomberg

- [United Kingdom] Average house price in Great Britain exceeds £350,000 for first time. Asking prices up 1.7% in March, biggest monthly rise for this time of year in 18 years, according to Rightmove – The Guardian

- [United Kingdom] Where next for the private rented sector? – Social Market Foundation

On cross-country:

- Could housing crack before inflation does? And a contrarian view on oil – FT

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, March 24, 2022

The Red Hot Housing Market: the Role of Policy and Implications for Housing Affordability

From a speech by Fed Governor Christopher J. Waller:

On rents:

“However, more recently rents have accelerated sharply. On net, rents have risen 6.5 percent since January 2020, according to the prices tracked under the Consumer Price Index (CPI). That is not out of line with the pace of rent increases seen in the CPI over the previous five years. But there is good reason to think this number doesn’t fully reflect the extent to which rents have grown. CPI measures rents that people are currently paying, under leases that can be slow to reflect market conditions. Meanwhile, measures of market rent have increased a lot more than 6.5 percent over the last two years. For example, CoreLogic’s single family rent index rose 12 percent over the 12 months through December, and RealPage’s measure of asking rent for units in multifamily buildings rose 15 percent over the 12 months through February. Based on various measures of asking rents, some recent research suggests that the rate of rent inflation in the CPI will double in 2022. If so, rent as a component of inflation will accelerate, which has implications for monetary policy.

Rent is a significant share of monthly expenses for many households, but lower income households spend a larger fraction of their budget on housing, so rising rents hit these households harder. In 2019, those in the lowest quintile of household income dedicated 41 percent of their spending to housing, while those in the top quintile spent only 28 percent. One piece of better news for low-income renters is that rent increases have not been larger in the neighborhoods where they tend to live. Specifically, data from RealPage suggest that asking rents rose 16 percent in both low- and moderate-income neighborhoods from January 2020 to February 2022, the same as in higher income neighborhoods.”

On affordability of purchasing a home:

“House prices are up a cumulative 35 percent since the beginning of the pandemic, according to the Zillow Home Value Index. That rate of increase is much faster than the previous five years and even faster than during the housing boom of the mid-2000s. Looking over the past two years, one would think the large increase in home prices would have made it more difficult for renters to become first-time buyers. Surprisingly, we have not seen evidence of that yet. The fraction of renters aged 20 to 45 who transitioned into home ownership last year was the highest since the Great Recession. It could be that time spent at home during the pandemic made renters more interested in owning a home, or that people are getting help from family or friends with down payments, or that some people are choosing to buy smaller homes than they would have a few years ago when prices were lower. Whatever the causes, the increase in first time buyers is clear.

Home buying during the pandemic has been strong among minority families as well. In 2020, 7.3 percent of home purchase loans for owner-occupied properties were taken out by Black families, the highest level since 2007 and well above the low of 4.8 percent in 2013. Still, the gap in homeownership rates between minority and white families remains very wide. Moreover, according to Census Bureau data, homeownership rates for Black and Hispanic families appear to have edged down during 2021. These trends may reflect that the negative economic effects of the pandemic were felt disproportionately by minority households. Indeed, research shows that minority homeowners were much more likely to miss mortgage payments and enter mortgage forbearance than white homeowners. While federal and private sector forbearance programs helped many households keep their homes, families experiencing more permanent or severe income losses may have had to sell their homes and exit homeownership.”

On housing demand:

“Demand for housing space has been especially strong during the pandemic. Lockdowns as well as remote work and school may have spurred people to seek homes with more space, leading to an increase in demand for larger and otherwise better homes.5 In fact, the average size of new single-family homes increased in 2021, reversing a downward trend from 2015 through 2020. Retail sales at building supply stores surged during the pandemic, as homeowners added space or made other improvements that could increase the quality of their homes. In January, this spending was 42 percent higher than the average for 2019, and even after adjustment for the sharp increase in the price of building materials, it was still up 19 percent. One indication of people trading up for housing is evident by comparing Zillow’s Home Value Indexes by housing type. The index for single-family homes has increased more than that for condominiums since January 2020. In addition, purchases of second homes have increased. Second homes averaged about 3-1/2 percent of home purchase loan originations from 2014 to 2019 but about 5 percent of originations in 2021. The 2021 share was in line with the peak seen during the last housing boom.

Meanwhile, changes in household formation may have been contributing to increases in housing demand over the past year or so. While many households increased in size during the early months of the pandemic, as young people returned to their parents’ homes, this change appears to have largely reversed by the end of 2021. The fraction of adults aged 18 to 30 who are the heads of their own households is now back near its 2017-2019 average. The surge in the number of households has pushed down housing vacancy rates from already-low levels. Rental and homeowner vacancy rates fell considerably during the pandemic, reaching lows in the fourth quarter of last year that haven’t been seen since the 1980s.

The pandemic-related changes in demand for housing, rented and owned, coincided with a longer-run increase in demand to live in certain parts of the country. For the past several decades, demand for living in cities with high-paying jobs and many urban amenities has surged, pushing up housing costs in these areas. Among metro areas in the top quartile of local housing demand, population increased 80 percent, and single-family home prices rose more than 110 percent from 1990 to 2019 after adjusting for inflation.6 For the nation as a whole, population only increased 32 percent and house prices rose 59 percent.”

On housing supply:

“The supply side has been pushing in the same direction—towards tighter housing markets and more expensive shelter. U.S. housing supply has probably been more constrained lately than at any time since the end of World War II. One estimate is that the current growth in the supply of new housing units is about 100,000 less per year that would be needed to support trend increases in demand from household formation and replacement of depreciating units.7 Supply adjusts to changes in the economy more slowly than demand because of the time it takes to plan and build. With workers at home and supply bottlenecks, there were pandemic-related drops in the production and importation of many construction materials. These supply shortages contributed to skyrocketing input prices. In January 2022, lumber prices included in the Producer Price Index were 92 percent higher than the 2019 average. Even with increased materials costs, suppliers have been unable to keep up with demand. The volume of lumber now being sold is more than 150 percent higher than last August and is similarly larger than the average volume over the previous ten years.

Labor is also a key input in home construction. The supply of construction labor, like other sectors, has been held down by pandemic-specific issues like early retirement. One measure of labor market tightness for the construction industry increased steadily from 2010 to 2019 and then in 2021 was more than double the level recorded during the construction boom of the mid-2000s.

Local land use regulations have also played a role in constraining housing supply over the past several decades. Probably not by accident, these regulations have tended to be more restrictive in areas with high housing demand. There has been a growing public debate about these restrictions on local home building, not just at the local level, but among governors and state legislatures. While some local regulations have been changed to allow more housing construction in high demand areas, the effects will take time, and it remains to be seen whether the increases in supply created by these regulatory changes will be enough to satisfy local demand.”

From a speech by Fed Governor Christopher J. Waller:

On rents:

“However, more recently rents have accelerated sharply. On net, rents have risen 6.5 percent since January 2020, according to the prices tracked under the Consumer Price Index (CPI). That is not out of line with the pace of rent increases seen in the CPI over the previous five years. But there is good reason to think this number doesn’t fully reflect the extent to which rents have grown.

Posted by at 4:22 PM

Labels: Global Housing Watch

Subscribe to: Posts