Showing posts with label Global Housing Watch. Show all posts

Friday, July 1, 2022

Housing View – July 1, 2022

On cross-country:

- 2nd Workshop on Rent Control: Slides of presentations – PPT and Video

- The Global Housing Inspection Report – 2022 Edition – Seeking Alpha

- Land speculation, booms, and busts with endogenous phase transitions: A model of economic fluctuations with rational exuberance – VoxEU

On the US:

- Can the Fed pull off a controlled slowdown of the housing market? The events of the early 1980s might provide a guide – The Economist

- ‘Coast to Coast’ Housing Correction Is Coming, Says Moody’s Chief Economist. US home prices will likely fall in the most overvalued markets, projects Mark Zandi. But it will fall short of a crash. – Bloomberg

- Cost of Owning a Home Surges Above the Cost of Renting One. A new report shows that having a mortgage is far more expensive than having a lease, a disparity that is helping to cool a red-hot housing market. – New York Times

- Demand Shifting from Owning to Renting – John Burns Real Estate Consulting

- As For-Sale Demand Weakens, Single-Family Rentals Outperform – John Burns Real Estate Consulting

- ‘Coast to Coast’ Housing Correction Is Coming, Says Moody’s Chief Economist. US home prices will likely fall in the most overvalued markets, projects Mark Zandi. But it will fall short of a crash. – Bloomberg

- Home Sellers Are Getting Anxious. ‘They Feel Like They Missed the Height of the Market.’ – Barron’s

- Bidding Wars Overheated the Home-Buyer Market, Now They’re Coming for Renters. Competition among renters means many tenants feel compelled to pay more each month than what the landlord is asking – Wall Street Journal

- Credit Conditions in the Pandemic Mortgage Market – San Francisco Fed

- Hottest US Housing Markets Now Have Bigger Share of Price Cuts – Bloomberg

- Transcript: Jonathan Miller – The Big Picture

- Highest Mortgage Rates Since 2008 Housing Crisis Cool Sales. As the Federal Reserve tries to fight high inflation, costly mortgage rates have begun to price people out of the housing market – New York Times

- Disquiet Over the Housing Market Is Only Growing. The Fed needs to remove the heat from demand without prompting an accident among mortgage financiers – Bloomberg

- Blackstone dealt legal setback after $5bn low-income housing deal. Private equity group says it is working to resolve litigation inherited with AIG property portfolio – FT

- Did Housing Affordability Worsen During the First Year of the Pandemic? – Joint Center for Housing Studies

- A Hot Housing Market Is a Financial Crisis Risk. The longer prices defy the Fed, the harder the Fed might try to break them. – Bloomberg

On China

- Empirical evidence of risk contagion across regional Chinese housing markets – Economic Modelling

- Chinese Property Titan Says Housing Market Has Reached Bottom – Bloomberg

On other countries:

- [Australia] House Prices, Monetary Policy, and Commodities: Evidence from Australia – University of Sydney

- [Japan] Japanese house prices rising strongly, but demand slowing – Global Property Guide

- [Portugal] Portugal Home Prices Rise Faster Than Ever on Lack of Supply – Bloomberg

- [Spain] How fiscal policy affects housing market dynamics: Evidence from Spain – Bulletin of Economic Research

- [United Kingdom] Covid couldn’t cool house prices, but the economic chill might. Data due this week will be closely scrutinised to discern whether the market’s remarkable resilience is faltering – The Guardian

- [United Kingdom] Short-term lets face stricter rules as review gauges impact on tourist hotspots. Concern over proliferation of Airbnb-style rentals in popular holiday destinations spurs action – FT

On cross-country:

- 2nd Workshop on Rent Control: Slides of presentations – PPT and Video

- The Global Housing Inspection Report – 2022 Edition – Seeking Alpha

- Land speculation, booms, and busts with endogenous phase transitions: A model of economic fluctuations with rational exuberance – VoxEU

On the US:

- Can the Fed pull off a controlled slowdown of the housing market?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 30, 2022

Housing Market in Portugal

From the IMF’s latest report on Portugal:

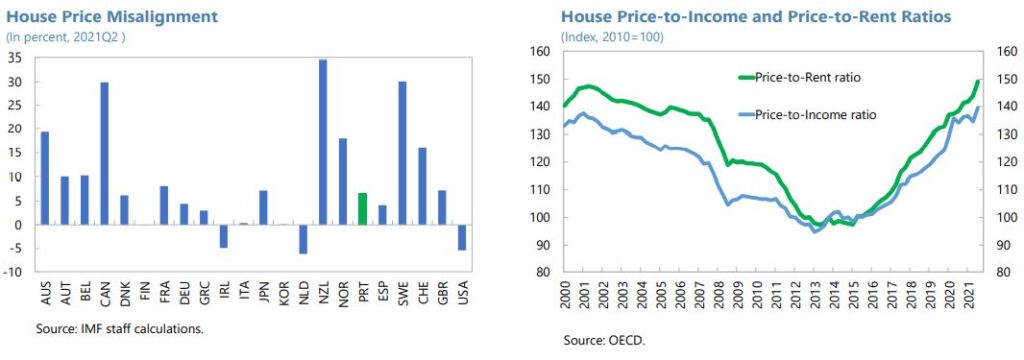

“Since 2015, Portuguese house price growth outpaced the EA average by almost 30 percentage points. This pace was sustained throughout the pandemic, with residential real estate prices gaining nearly 20 percentage points in real terms and relative to rents.

Available estimates suggest overvaluation of residential real estate. Based on indicators developed by the ECB, Banco de Portugal estimates point to an over-valuation of 8 to 16.5 percent (see Banco de Portugal, December 2021 Financial Stability Report). IMF model-based estimates of house price misalignments relative to fundamentals point to an overvaluation of 7 percent as of mid-2021. However, since mid-2021 house prices increased by 5.7 percent by end-2021. Price-to-rent and price-to income ratios have reached the highest levels since 2000.

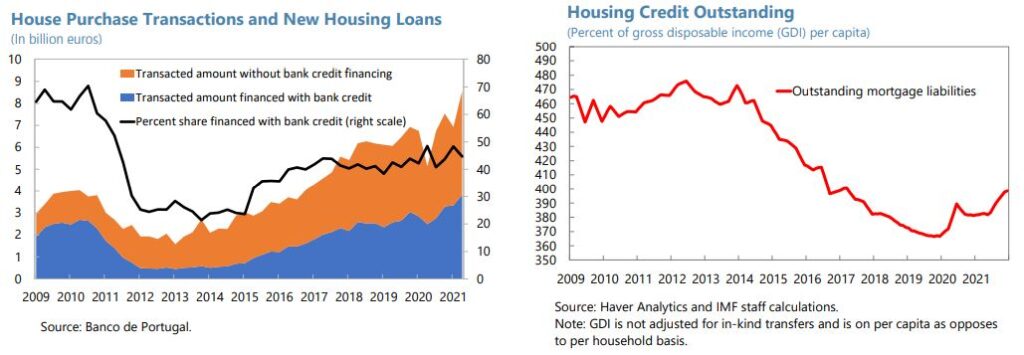

Domestic bank credit has not been a key driver of house prices yet. Even before the pandemic, Portugal had become one of EA’s most dynamic real estate markets partly reflecting tax incentives for foreigners and the Golden Visa program, whereby non-resident flows contributed to drive up housing prices. With households deleveraging since 2012–13, outstanding house credit to disposable incomes declined by 100 pp between 2014 and 2019. Housing credit growth turned positive only from 2019, driven by improved consumer confidence and low interest rates. While credit it still below historical averages, some estimates suggest small but positive credit gaps emerging in recent years. Housing supply shortages also played a role in boosting prices, with relatively subdued construction activity in the pre-pandemic years, although the construction sector remained resilient throughout the pandemic. Some cities (e.g., Lisbon) also saw a compression in price variation, with lower-end prices seeing steep gains.

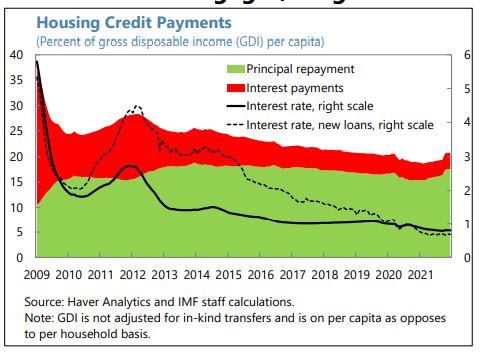

Although aggregate housing debt service as a share of disposable income was declining before the pandemic, this trend has slowed. On a per capita basis, average mortgage payments correspond to about 1/5th of household gross disposable income, marginally lower than the peak during the 2012–13 sovereign debt crisis. Also, mortgage interest payments declined from about 12 percent of disposable income in 2012H1 to about 3 percent in 2021. Principal repayments dipped temporarily due to moratoria.

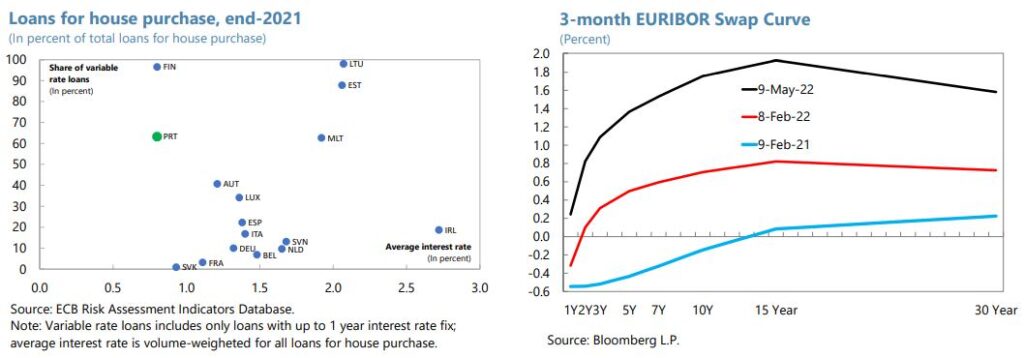

With house lending relying predominantly on variable rate mortgages, a significant increase in interest rates would quickly erode household incomes. Three quarters of housing loans have rate fixation of up to one year, with Euribor as the benchmark, while only a small fraction has fixed rates for longer than 10 years. Compared to early 2021, 2-year swap rates have widened by over 150 basis points reflecting expectations of ECB monetary tightening. With historic and euro-area’s lowest mortgage interest rates as of 2021Q4 – 0.7 percent for new mortgages and 0.8 percent for all outstanding –a 1 pp higher rate could raise household interest payments from 3.2 percent to about 7.2 percent of average household income, potentially also impacting aggregate demand. As per BdP’s borrower-based macroprudential policy measures, banks are recommended to consider a 300 basis point interest rate shock in the calculations of DSTIs for new mortgages.

The Bank of Portugal expanded its macroprudential toolkit in 2018, including measures on new credit agreements relating to residential property and consumer credit (also see Neugebauer and others 2021, Banco de Portugal Financial Stability Report, December 2021). Supervisory data indicate that borrower profiles improved in 2019, partly reflected in the increase in the share of mortgage credit granted to borrowers with net income above median. Nonetheless, the average maturity of new loans has not undergone gradual convergence towards 30 years, which prompted new macroprudential guidance from April 2022 on limits to maximum maturities. As regards the interest rate risk, and as mentioned above, the measures stipulate that banks should take into account the impact of higher interest rates in the calculations of DSTI, which is a mitigating factor. More generally, risks need to be closely monitored and consideration should be given on further strengthening capital positions, in accordance with the ESRB guidance, should vulnerabilities from the residential real estate sector continue increasing.

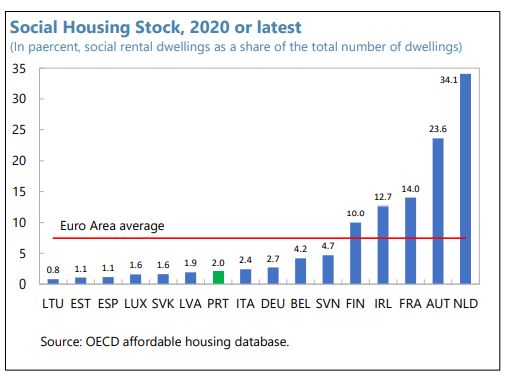

In view of rising house prices and limited social housing, housing affordability has also been a growing concern. House prices to disposable income are high among EA countries. Social housing is also limited, at about 2 percent of the total housing stock compared to EA average of 7.5 percent. In this context, the NGEU financed NRRP provides an opportunity for such investments to increase the stock of affordable rental housing for low-income families, which can also facilitate job mobility.”

From the IMF’s latest report on Portugal:

“Since 2015, Portuguese house price growth outpaced the EA average by almost 30 percentage points. This pace was sustained throughout the pandemic, with residential real estate prices gaining nearly 20 percentage points in real terms and relative to rents.

Available estimates suggest overvaluation of residential real estate. Based on indicators developed by the ECB, Banco de Portugal estimates point to an over-valuation of 8 to 16.5 percent (see Banco de Portugal,

Posted by at 12:37 PM

Labels: Global Housing Watch

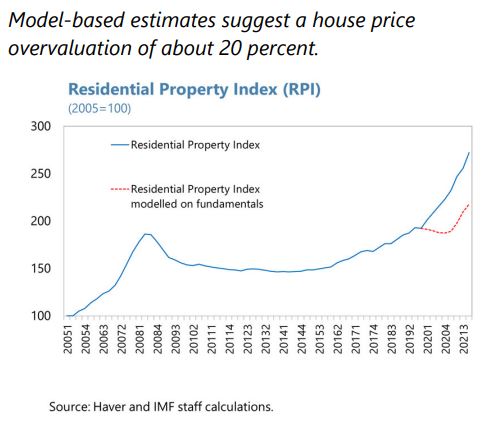

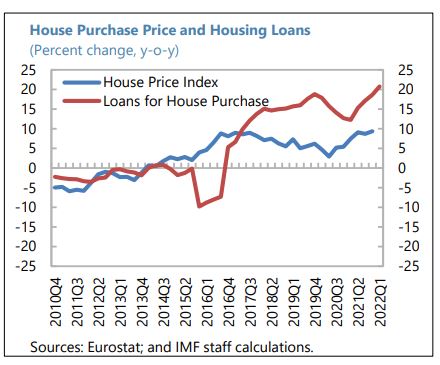

Housing Market in Slovak Republic

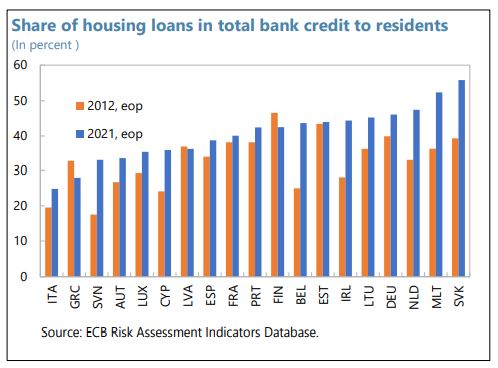

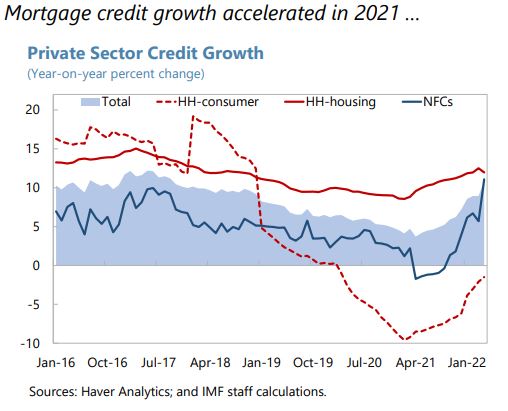

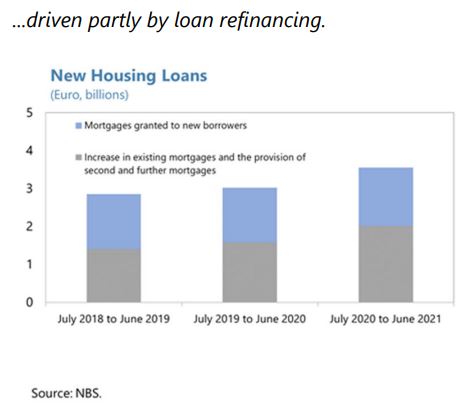

From the IMF’s latest report on Slovak Republic:

“House price growth has continued to accelerate amid rapid mortgage credit growth, driven by record low borrowing costs and looser credit standards. House price growth increased throughout 2021, reaching 22 percent y/y in 2022:Q1, with a wide gap between actual and model-predicted house prices. While housing affordability (as captured by the share of disposable income taken up by mortgage payments) remained quite high until mid-2021 given low interest rates and robust wage growth, and housing cost overburden for lower-income households is moderate from an international perspective, tightening financial conditions and higher inflation could quickly change this.

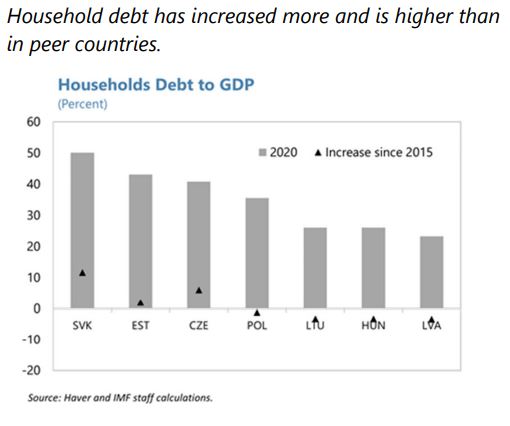

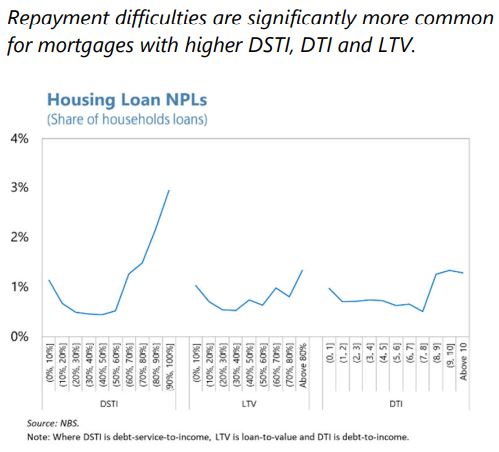

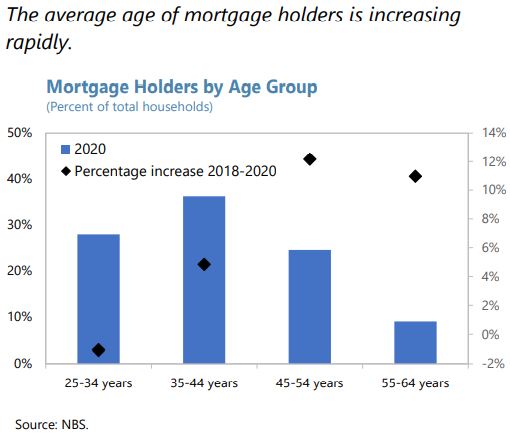

Macrofinancial vulnerabilities related to the housing market warrant close monitoring. Household debt relative to GDP has risen faster and is higher than in peer countries, due to the increase in homeowners with mortgages and the topping-up of existing mortgages. The active use of borrower-based measures has reduced the share of high LTV, DTI, and DSTI mortgages, but the cluster of mortgages right below regulatory limits is a potential source of vulnerability.16 There has also been an increase in mortgages with maturities extending beyond borrowers’ retirement age.

While the macroprudential stance is broadly adequate from a financial stability point of view, the authorities could consider introducing additional macroprudential policy measures to address housing market vulnerabilities if imbalances persist.17 As recommended in the 2021 IMF Staff Report and the ESRB, the NBS could consider introducing capital-based measures on mortgage exposures, including minimum risk weights, to strengthen banks’ resilience to adverse housing market shocks. The NBS could also explore applying the sectoral systemic risk buffer (SyRB) to target systemic risks from mortgage loans under the new Capital Requirements Directive (CRD V) flexibility, after conducting a cost-benefit analysis. To address pockets of vulnerability, such as the concentration of loans below regulatory limits and the rise in loans with maturities beyond retirement age, the authorities could consider adjusting borrower-based measures. For example, additional amortization requirements for new mortgages at the regulatory ceilings could reduce their clustering right underneath those ceilings. The proposal of a gradually falling DTI limit as borrowers approach retirement age would help limit overindebtedness of vulnerable pensioners, though it will be important to monitor its implementation and ensure that it does not reduce excessively access to credit to potentially credit-worthy older borrowers.

Addressing housing supply shortages and reforming property taxation could help alleviate property market pressures. Over the past decade, the overcrowding rate in Slovakia has declined but remains significantly higher than the EU average, especially among the younger population.18 The inflow of refugees might also raise housing demand. Improving housing supply will have social benefits as well as dampen house price growth and associated vulnerabilities. In that regard, the recently approved construction and spatial planning laws, which aim to simplify the construction code, shorten the lengthy building permit process and reduce bureaucracy are welcome. Developing the rental market could also help contain house price inflation. Finally, raising Slovakia’s property taxes would strengthen public finances and dampen overheating pressures.

Authorities’ Views

The authorities broadly concurred with staff’s assessment of housing market risks. They are open to expanding their macroprudential toolkit with capital-based measures, such as minimum risk weights, but a thorough cost-benefit analysis would be needed, especially given the sizable differences in mortgage risk-weights among IRB banks. They plan to introduce age-related DTI limits to address the rise in mortgages with maturities extending beyond retirement age. Their analysis suggests that the early adoption of such a precautionary measure would help limit excessive indebtedness and reduce the accumulation of risks, with only a slight reduction of credit growth. They also highlighted recent regulatory changes to bolster housing supply flexibility.”

From the IMF’s latest report on Slovak Republic:

“House price growth has continued to accelerate amid rapid mortgage credit growth, driven by record low borrowing costs and looser credit standards. House price growth increased throughout 2021, reaching 22 percent y/y in 2022:Q1, with a wide gap between actual and model-predicted house prices. While housing affordability (as captured by the share of disposable income taken up by mortgage payments) remained quite high until mid-2021 given low interest rates and robust wage growth,

Posted by at 12:13 PM

Labels: Global Housing Watch

Friday, June 24, 2022

Housing Market in Bulgaria

From the IMF’s latest report on Bulgaria:

“Despite recent measures, credit risk could increase, including due to spillovers from the war. During the pandemic, macroprudential measures provided banks room to manage a possible deterioration of loan quality without limiting credit flows, while broader measures supported borrowers’ repayment capacity. Nominal credit to households is now growing at a rapid pace, driven by housing mortgages. To prevent the buildup of new risks, the BNB appropriately announced gradual increases in the countercyclical capital buffers (CCCB), up to 1.5 percent in 2023 from 0.5 percent currently. Possible further increases will need to consider the strength of the recovery to ensure that credit to corporates remains sufficiently available to support private investment. The introduction of borrower-based measures could also be considered if signs of overheating in the real estate market were to emerge. Supervisors should continue to ensure that banks monitor asset quality for possible deterioration and proactively resolve NPLs, as credit risks may rise with the lagged impact of withdrawing COVID-19 related support, the impact of surging commodity prices and supply-chain disruptions on corporates, rising interest rates, or the emergence of imbalances in the housing market.”

From the IMF’s latest report on Bulgaria:

“Despite recent measures, credit risk could increase, including due to spillovers from the war. During the pandemic, macroprudential measures provided banks room to manage a possible deterioration of loan quality without limiting credit flows, while broader measures supported borrowers’ repayment capacity. Nominal credit to households is now growing at a rapid pace, driven by housing mortgages. To prevent the buildup of new risks, the BNB appropriately announced gradual increases in the countercyclical capital buffers (CCCB),

Posted by at 12:48 PM

Labels: Global Housing Watch

Housing View – June 24, 2022

On cross-country:

- The World’s Bubbliest Housing Markets Are Flashing Warning Signs. Global monetary tightening is squeezing homebuyers, adding risks that a slowdown could ripple through the economy. – Bloomberg

- The property industry has a huge carbon footprint. Here’s how to reduce it. Some buildings should be retrofitted, others torn down – The Economist

On the US:

- America Faces a Housing Bust. All ingredients seemed in place at 2022’s start for a continued housing boom, but now the market has priced itself for a sharp reversal – Wall Street Journal

- The State of the nation’s Housing 2022 – Joint Center for Housing Studies of Harvard University

- Is another housing crash on the way? – The Economist

- Investors’ Housing Bets Are on Shaky Foundations. Cash has been pouring into residential property on the assumption that an unprecedented run up in rents will continue – Wall Street Journal

- We’re Already Seeing the Stock Market Selloff Spill Into the Housing Market. It’s especially notable in places where stock-based comp is significant. – Bloomberg

- U.S. labor market appears to cool; homebuilding slumps as rates surge – Reuters

- US Housing Starts Decline to Lowest Level in More Than a Year. May construction fell to 1.55 million pace after April surge. Builder backlogs remain elevated even as sales decrease – Bloomberg

- Housing Just Hit a Wall. What’s Next for Prices, Brokers, and Builder Stocks. – Barron’s

- Work From Home and the Office Real Estate Apocalypse – SSRN

- The Size and Census Coverage of the U.S. Homeless Population – NBER

- Housing’s Slowdown Has Economy on the Edge. News of a cooling housing market might be a relief to some, but we’ll be living with the aftereffects for a long time to come. – Bloomberg

- Hot Housing Market Keeps Home Foreclosures at Bay. Robust home prices and government relief programs are giving financially squeezed homeowners options to avoid foreclosure – Wall Street Journal

- US House Prices Are Likely to Drop as Rates Rise, Capital Economics Says – Bloomberg

- The Left-NIMBY meltdown. It’s getting harder to pretend that blocking new housing helps poor people. – Noah Smith

- Cancel Zoning. If we want to fix the housing-affordability crisis, segregation, and sprawl, zoning must go – The Atlantic

- In Pursuit of Affordable Housing: The Migration of Homebuyers within the U.S.—Before and After the Pandemic – Freddie Mac

On China

- China’s Once-Sizzling Property Market Has Started to Cool. New home prices in China have fallen, and would-be buyers are thinking twice. That’s bad news for the overall economy. – New York Times

- Chinese Developer Accepts Wheat, Garlic as Payment to Woo Buyers – Bloomberg

- China’s Property Slump Is a Bigger Threat Than Its Lockdowns. The worst decline on record could hold growth below 4% for the rest of the decade. – Bloomberg

On other countries:

- [Australia] Sydney house prices still 20% above pre-pandemic levels despite rising interest rates. Economists say while property prices could come down by up to 20%, affordability has ‘never been worse’ – The Guardian

- [Australia] Sales slow down in Sydney’s suburbia-on-sea. After a period of rising prices, homebuyers are starting to get more for their money, while some sellers lose out – FT

- [Canada] Distressed Deals Pile Up in Canada’s Once-Booming Housing Market. Prices are falling in some of the urban markets that had the biggest increases over the past two years. That’s leading to broken and renegotiated deals. – Bloomberg

- [Israel] Israel lawmaker seeks larger mortgage loans as home buyers priced out – Reuters

- [Sweden] Sweden’s Housing Bubble Deflates as Realtors Sound Alarm – Bloomberg

- [United Kingdom] Are the Days of UK Property Booms and Busts Over? Tougher mortgage regulation in 2014 sought to contain overstretched buyers. Its effectiveness is about to be put to the test. – Bloomberg

- [United Kingdom] Bank of England to Get Rid of Mortgage Affordability Rules. UK central bank will end the affordability test from Aug. 1. The BOE raised the benchmark interest rate last week to 1.25%. – Bloomberg

On cross-country:

- The World’s Bubbliest Housing Markets Are Flashing Warning Signs. Global monetary tightening is squeezing homebuyers, adding risks that a slowdown could ripple through the economy. – Bloomberg

- The property industry has a huge carbon footprint. Here’s how to reduce it. Some buildings should be retrofitted, others torn down – The Economist

On the US:

- America Faces a Housing Bust.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts