Showing posts with label Global Housing Watch. Show all posts

Friday, July 15, 2022

Housing View – July 15, 2022

On cross-country:

- Are foreigners inflating property prices? – BFM

On the US:

- New Fed Paper Finds Surging Home Prices Driven by Demand — Not Supply – Bloomberg

- Volatility in Home Sales and Prices: Supply or Demand? – Federal Reserve Board

- What’s behind the rising rents and what can be done? – Washington Post

- Relief Eludes Many Renters as Fed Raises Interest Rates. As the central bank sharply increases borrowing costs, it could lock would-be home buyers into rentals and keep a hot market under pressure. – New York Times

- Remodeling Market Declines Year-over-Year – NAHB

- The Great Appreciation Of Home Prices Is Now Over – Forbes

- Housing Shortage Spreads Across US, Becoming Coast-to-Coast Crisis. New analysis shows deficits surging just before the pandemic, even in areas that had few supply challenges a decade ago. – Bloomberg

- What’s Up With the Crazy Housing Market? Rising mortgage rates. Faltering home sales. Skyrocketing rents. Here’s how to make sense of a baffling real estate market. – New York Times

- Housing inventories may note save prices after all – Washington Post

- The United States Must Deliver on Equitable Housing Outcomes for All. Federal investments kept millions of Americans in their homes during the pandemic; in the long term, commitment to bold federal housing policy can eliminate housing insecurity for millions while uplifting historically disadvantaged communities. – American Center for Progress

- Who’s To Blame for Gentrification? Most likely, no one in particular—but policy changes can alleviate the housing shortage and prevent displacement. – Planetizen

- Why this tightening cycle is so brutal for the US housing market – Quartz

- Housing-Affordability Index Drops to Lowest Level Since 2006. Mortgage rates and home prices are up sharply, pressuring buyers and driving sellers to cut prices – Wall Street Journal

- The Coming Housing Risks – American Action Forum

- The cities where house prices are most likely to fall – Axios

- The great house U.S. price boom continues – Global Property Guide

- Inflation Expectations Increase at Short Term, But Decline at Medium and Longer Terms; Home Price Growth Expectations Decline Sharply – New York Fed

- How to limit the risks to financial stability posed by the Federal Home Loan Bank System – Brookings

- Housing Could Provide More Fuel for Inflation. Other consumer prices might need to post big drops for the Fed to see overall inflation fall – Wall Street Journal

On China

- Is China Stumbling Into Its Own Mortgage Crisis? A rapidly spreading protest — borrowers refusing to make payments on unfinished homes — threatens to rattle the financial system. – Bloomberg

- China Convenes Banks on Mortgage Boycott Roiling Markets. Officials asked for information on impact of housing loan snub. More buyers refuse to pay loans on unfinished home projects – Bloomberg

- Chinese Homebuyers Across 22 Cities Refuse to Pay Mortgages. Home loan payment halts may cause $83 billion of bad debt. China Construction Bank, Postal Bank, ICBC may be more exposed – Bloomberg

- China developers face $13bn wall of dollar bond payments in second half. Foreign investors fear Beijing will favour onshore creditors as Shimao Group becomes latest to default – FT

On other countries:

- [Cambodia] Cambodia’s house prices plunging – Global Property Guide

- [Ireland] Taxes Can Ease House Price Volatility, Irish Central Bank Says – Bloomberg

- [Sweden] Swedish Home Price Expectations Drop to Lowest Level Since 2008. SEB survey points to worsening price outlook for houses. The Riksbank sees home prices falling 16% through end of 2023 – Bloomberg

- [Thailand] Thailand’s housing market continues to slow – Global Property Guide

- [United Kingdom] UK house prices rise at fastest rate in 18 years. Typical home goes for record £294,845 as property shortage drives up costs for buyers – FT

- [United Kingdom] Covid-19 and the curious case of the rental bust-up that never came. An arbitration scheme to handle pandemic rental arrears is currently virtually unused – FT

On cross-country:

- Are foreigners inflating property prices? – BFM

On the US:

- New Fed Paper Finds Surging Home Prices Driven by Demand — Not Supply – Bloomberg

- Volatility in Home Sales and Prices: Supply or Demand? – Federal Reserve Board

- What’s behind the rising rents and what can be done? – Washington Post

- Relief Eludes Many Renters as Fed Raises Interest Rates.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, July 12, 2022

Housing Market in the US

From the IMF’s latest report on the US;

“The housing market has been on a steep upward trajectory. Nationwide, average prices are 38 percent above where they were at end-2019 and prices are relatively high as a share of both rents and household income. Leverage, though, has been contained by relatively low loan-to-value ratios and conservative underwriting standards (a legacy of the post-financial crisis reforms). In addition, refinancing activity over the past few years has reduced average mortgage payments to all-time lows as a share of disposable income. As such, financial stability risks emanating from the housing market appear to be contained. However, there are important social concerns linked to the worsening in housing affordability, particularly for lower income households.”

From the IMF’s latest report on the US;

“The housing market has been on a steep upward trajectory. Nationwide, average prices are 38 percent above where they were at end-2019 and prices are relatively high as a share of both rents and household income. Leverage, though, has been contained by relatively low loan-to-value ratios and conservative underwriting standards (a legacy of the post-financial crisis reforms). In addition, refinancing activity over the past few years has reduced average mortgage payments to all-time lows as a share of disposable income.

Posted by at 5:50 PM

Labels: Global Housing Watch

Friday, July 8, 2022

Housing Market in Ireland

From the IMF’s latest report on Ireland:

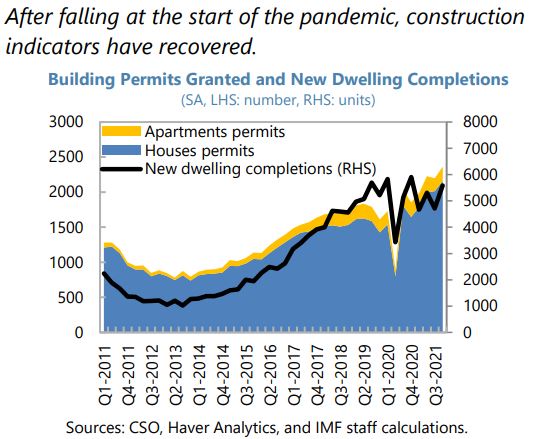

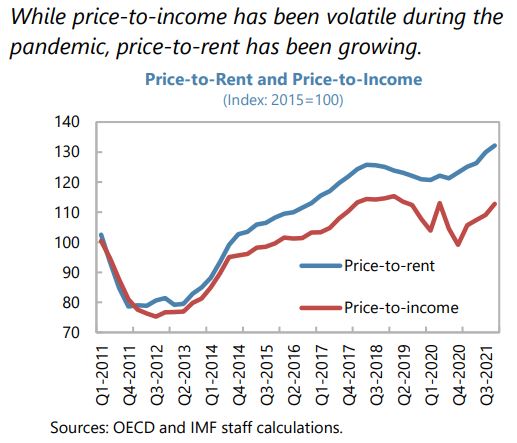

“The pandemic has exacerbated housing market’s imbalances, contributing to accelerating prices despite the recent acceleration in housing construction. Double-digit price growth has further pressured affordability as price-to-income and price-to-rent ratios increased sharply in recent quarters. House completions recovered in 2021 but were still below 2019 levels.

Housing commencements have accelerated to the highest number since the GFC, but the construction sector is facing combined headwinds of input cost inflation and labor shortages.

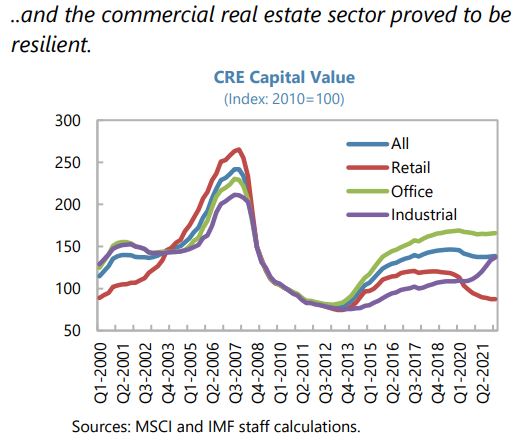

CRE activities performed better than expected during the pandemic. Investment in the sector was exceptionally strong in 2021 and this momentum is expected to continue in 2022. The polarization between different sectors that characterized the Irish property investment market stems from the higher return to investment in CRE than residential, partly due to the strong growth of MNEs, Brexit-related relocations to Ireland, and businesses’ general resilience despite the pandemic.

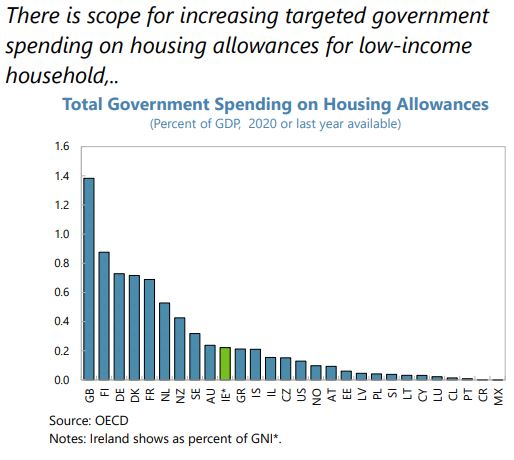

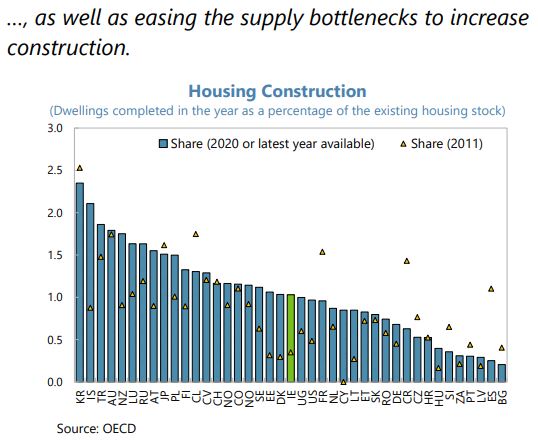

Supply-side policies should be further strengthened. The government has introduced a comprehensive fiscal and regulatory package (Housing for All18), costing close to 1 percent of GDP annually, to address the affordable housing shortage. The package includes measures to improve zoning, planning, land availability, and social housing. Timely implementation of these measures is needed and should be accompanied by additional policies aimed at raising productivity in the construction sector. The “First Home” affordable purchase shared-equity scheme (starting in 2022:Q3) aims to support first home buyers. However, it does not address the supply bottlenecks. While the scheme is partly targeted and limited in size, if expanded it can put further upward pressure on prices.

Improving construction productivity is needed to bolster housing supply. The construction sector is fragmented, lagging on digitalization, and faces high input costs and labor shortages. Complex and lengthy processes for obtaining occupational licenses, with excessively long apprenticeship requirements, raise barriers to entry and contribute to substantial bottlenecks and high costs of construction. In recent years, the government has taken some steps toward digitalization of the construction sector, upskilling and reskilling workers, including by increasing the number of apprenticeship centers. There is also a need to streamline the lengthy, cumbersome, and uncertain zoning and permit processes.

The government is implementing a set of comprehensive measures under “Housing for All – A New Housing Plan for Ireland” aimed at alleviating the housing shortage. Establishment of the Construction Sector Innovation and Digital Adoption Subgroup by the government and the industry is welcome to deliver on the seven priority actions detailed in the Building Innovation Report. The Construction Sector Group ensures regular and open dialogue between government and industry on how best to achieve and maintain a sustainable and innovative construction sector in order to successfully deliver on the commitments in Project Ireland 2040.”

From the IMF’s latest report on Ireland:

“The pandemic has exacerbated housing market’s imbalances, contributing to accelerating prices despite the recent acceleration in housing construction. Double-digit price growth has further pressured affordability as price-to-income and price-to-rent ratios increased sharply in recent quarters. House completions recovered in 2021 but were still below 2019 levels.

Housing commencements have accelerated to the highest number since the GFC, but the construction sector is facing combined headwinds of input cost inflation and labor shortages.

Posted by at 7:44 AM

Labels: Global Housing Watch

Housing Market in Vietnam

From the IMF’s latest report on Vietnam:

“Property and corporate bond markets risks are rising. Easy financial conditions contributed to record-high corporate bond issuances and equity and property market valuations. Price pressure points are largely seen in land sales, high-end housing in major cities, and mega-developments in coastal areas. Besides sizable direct exposure to the real estate sector in their loan portfolios, banks face indirect exposure through holding of corporate bonds issued by real estate companies. These companies have fairly robust debt servicing capacity but are more leveraged than the rest of the economy, and some were hit hard by the pandemic-induced drop in tourism. Recent policies to moderate systemic risks include measures to limit excessive leverage (e.g., higher risk weights for real estate) and recommendations urging prudent loan origination, particularly for property purchases.”

From the IMF’s latest report on Vietnam:

“Property and corporate bond markets risks are rising. Easy financial conditions contributed to record-high corporate bond issuances and equity and property market valuations. Price pressure points are largely seen in land sales, high-end housing in major cities, and mega-developments in coastal areas. Besides sizable direct exposure to the real estate sector in their loan portfolios, banks face indirect exposure through holding of corporate bonds issued by real estate companies.

Posted by at 7:24 AM

Labels: Global Housing Watch

Housing View – July 8, 2022

On cross-country:

- Prime residential rents in global cities rising at fastest rate since 2010 – Knight Frank

- The Impact of Home Sharing on Housing Affordability. Evidence from Airbnb in Urban Cities in Europe – Jonkoping University

On the US:

- Written testimony for hearing by Jenny Schuetz: Where Have All the Houses Gone: Private Equity, Single Family Rentals, and America’s Neighborhoods – Brookings

- Home Sellers Are Slashing Prices in Sudden Halt to Pandemic Boom. The rapid rise in mortgage rates is cooling demand, jolting markets from coast to coast – Bloomberg

- Biden Administration Weighs Move to Trim Mortgage Costs as Home Prices Rise. Mortgage industry officials say insurance cut for FHA-backed loans would help entry-level buyers; Republicans say it could increase prices – Wall Street Journal

- Redfin’s chief economist says the housing market correction has begun—and things are going to get worse before they get better – Fortune

- Inflation is making homelessness worse – Washington Post

- Volatility in Home Sales and Prices: Supply or Demand? – Federal Reserve Board

- Pandemic-Induced Remote Work and Rising House Prices – NBER

- Construction Job Openings Leveling Off – NAHB

- Lessons Learned from Mortgage Borrower Policies and Outcomes during the COVID-19 Pandemic – Boston Fed

- Mortgage Rates Fall to 5.30%, Reflecting Recession Fears. Rates fell for a second straight week, though they are still up significantly this year – Wall Street Journal

On China

- My garlic for a home: China struggles to revive property sector. The real estate market is struggling to recover as zero-Covid policies and developer debt sap buyer demand – FT

- China Property Debt Crisis Is Just Beginning, Charlene Chu Says. Charlene Chu sees further problems for China real estate. Ex-Fitch analyst says debt weighing on China economic growth – Bloomberg

On other countries:

- [Austria] How Vienna took the stigma out of social housing. In some European cities living in social housing is a misfortune. In Austria’s capital it’s an indicator of high-quality urban life. – Politico

- [Australia] Australian house prices fall for second month as interest rates rise. CoreLogic’s home value index drops for the second month in a row, after declining 0.6% in June – The Guardian

- [United Kingdom] The signs are Britain is not heading for a property crash. It would be naive to rule out the possibility, but the evidence points to house prices dampening rather than tumbling – The Guardian

On cross-country:

- Prime residential rents in global cities rising at fastest rate since 2010 – Knight Frank

- The Impact of Home Sharing on Housing Affordability. Evidence from Airbnb in Urban Cities in Europe – Jonkoping University

On the US:

- Written testimony for hearing by Jenny Schuetz: Where Have All the Houses Gone: Private Equity, Single Family Rentals, and America’s Neighborhoods – Brookings

- Home Sellers Are Slashing Prices in Sudden Halt to Pandemic Boom.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts