Tuesday, March 29, 2022

Housing Market in Korea

From the IMF’s latest report on Korea:

“The pandemic magnified a chord of pre-COVID trends that included rising of already elevated household debt and rapid house price growth, raising macro-financial risks and social tension. These trends require coordinated policy action, including tightening of borrower-based macroprudential policies, raising real-estate taxes, and housing supply.

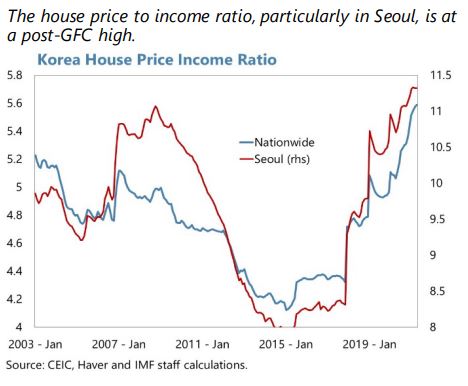

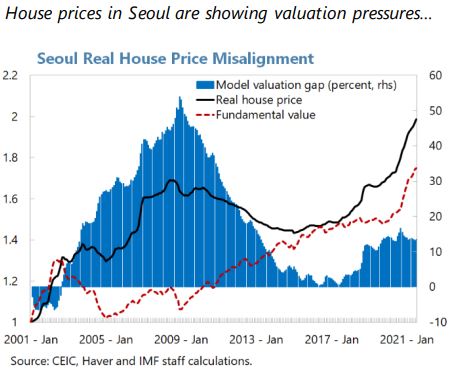

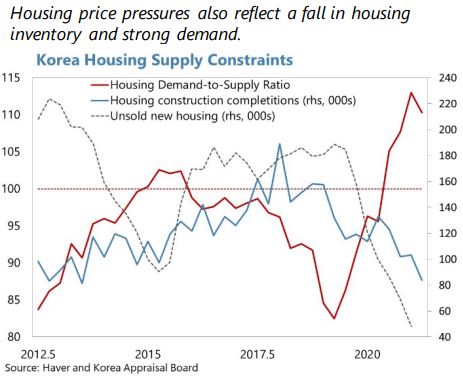

Real estate prices grew at an unprecedented rate during the pandemic, with the house price-to-income ratio at a multi-decadal high. Since the pandemic the confluence of a decline in mortgage rates, shifts in household formation, and longer-term structural factors linked to demography has fueled rapid growth in house prices. The strong real-estate demand surpassed new housing supply that has come on the market in recent years, particularly in Seoul. Historically low mortgage rates have fueled speculative behavior in the housing market, with house prices in the major cities now showing significant valuation pressures (Annex VIII and Figure 10). Prices have also significantly outpaced wages and widened inequality. House price growth is beginning to slow on the back of tighter prudential and monetary policies, but affordability will remain a concern going forward.

While housing supply has expanded in recent years, it has been surpassed by strong housing demand since the pandemic. Housing supply has grown by 30 percent in Seoul over the last decade, but the home ownership ratio remains relatively unchanged and lower than peer countries. To continue improving supply and improve affordability, particularly in urban areas, a number of welcome measures have been introduced: the easing of brownfield density restrictions for redevelopment projects; a fast track one-stop review process for redevelopment projects; allowance of pre- pre-sale of new apartments to facilitate housing access to first-time buyers. 10 Efforts are also underway to upgrade transportation links to greenbelt developments on the outskirts of Seoul. Over the medium term, the supply of new dwellings will need to consider Korea’s projected decline in population to avoid the potential risk of boom-bust cycles in the housing market.

Real-estate demand drove very strong growth in household debt during the pandemic, but vulnerabilities are mitigated. The tight borrower-based macroprudential stance has supported low NPLs and debt servicing ratios, and lending remains concentrated among high credit score individuals (Figure 11). Moreover, average LTVs are around 40 percent and household income is expected to remain stable which further contains balance sheet risks (Figure 12). FSAP and more recent Bank of Korea stress tests—applying a more severe economic shock than the pandemic downturn—showed that risks from household balance sheets are contained.

Some post-pandemic household lending developments may pose risks going forward. In contrast to pre-COVID trends, a larger share of new bank loan origination has been unsecured lending linked to floating interest rates, which is being used to top up lending and meet tight LTV requirements. There has also been strong growth in bullet loans, linked to the Jeonse market, which raises rollover risks. In turn, some subprime borrowers are resorting to non-banks to increase their financing. This suggests that borrower-based restrictions have been effective, but some mortgage prudential requirements can be circumvented. Moreover, while lending is concentrated among high credit score individuals, credit risks from the uplift in scores is susceptible to economy-wide credit cycles.

Household assets are concentrated in real-estate and closely intertwined with demographic challenges, which may also pose risks going forward. Korean households tend to self-insure for retirement by accumulating real-estate over their life cycle; the equity of which could be withdrawn in the reverse mortgage market. 12 Therefore, unlike in other advanced economies, engagement with the credit market does not decline with age.13 These risks could be further exacerbated in the future by the rapid demographic transition in Korea. 14 On both the assets (via real estate investment) and liabilities side (via Jeonse deposit), Korea household balance sheets are significantly exposed to real estate price fluctuations when compared to other advanced economies.

Policy Package to Contain Vulnerabilities

Given rising risks, housing and household debt vulnerabilities need to be closely managed. With due consideration on financial inclusion, a broad package of policies could help reduce financial risks from housing and household debt:

Macroprudential policies. Borrower-based prudential measures have been effective and recent measures, including the individual based DSR ceiling, are welcomed. 16 However, some prudential requirements on mortgage are being circumvented. Additional measures may be required, as recommended in the 2020 FSAP, including: (i) a sectoral counter cyclical capital buffer (sCCyB) to ensure banking sector resilience; (ii) introducing a stressed DSR ratio to moderate borrowing risk in the event there is a snapback in lending rates; (iii) formalizing the unsecured debt-to-annual income ratio ceiling that is currently a supervisory recommendation for both banks and nonbanks, (iv) incentivizing banks to lower the share of new unsecured floating rate lending via higher risk weights applied to unsecured loans. 17 The authorities should also review remaining gaps in lending-related regulations between banks and non-banks (e.g., DSR ceilings and loan-to-deposit ratio prudential requirements) to avoid individuals borrowing from multiple institutions to circumvent mortgage prudential requirements.

Tax policies: Tax measures implemented to contain housing demand include raising the Comprehensive Real Estate Holding Tax (CRET) for multiple-home owners and a transfer tax on short-term capital gain. The effectiveness of these measures should continue to be assessed against housing market outcomes. The higher CRET likely helped to expand supply by raising the holding costs for multiple-home owners, which could be broadened and raised to foster increased supply. However, the capital gains tax hike on multiple-home owners, while designed to reduce speculative demand, may have also reduced existing-housing supply, at least in the short term, by disincentivizing multiple-home owners from selling real-estate and should be reassesed as experience on its effectivenes is gained.

Housing supply. Current market valuations provide strong incentives for private sector developers to expand the supply of dwellings. However, private sector incentives are distorted by the regulatory and tax treatment of real estate, including price caps on new pre-construction apartment sales and excess capital gains on redevelopment projects, which should be reviewed to increase private housing supply. Moreover, further efforts should be made to accelerate the process of repurposing commerical land to residential usage in urban areas through encouraging greater coordination between governmental agencies and local councils. In this regard, the setting up of a public private task force composed of the Ministry of Land and Infrastructure, local governments, and industry is welcome.

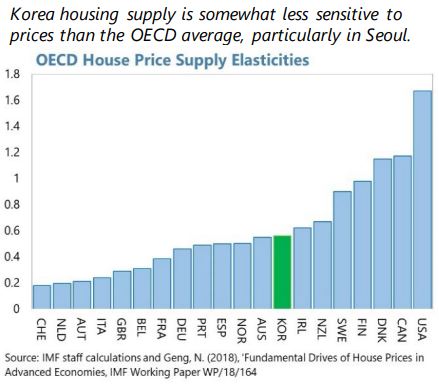

A combination of housing supply measures and higher property taxes would help contain housing prices over the medium-term. Staff analysis suggests that reforms that increase the elasticity of the supply of housing and higher property taxes would result in lower nationwide house prices (with the impact likely to be greater in Seoul).19 A combined policy package, together with the normalization of monetary policy conditions, would strengthen the effectiveness of these measures to reduce the growth of housing prices over the medium-term.

Authorities’ Views

(…)

The authorities view raising housing supply, particularly in Seoul, as an important step in making housing more affordable. The government announced a ‘30-80 plus’ project that aims to increase housing supply by 300 thousand homes in Seoul and 800 thousand homes nationwide over the next decade. While focusing on easing of building codes to accelerate the overall housing supply, the government will first increase the supply of office-tel apartments, which can be built more speedily due to a less onerous building code. The government will also directly purchase 35 thousand new development properties in Greater Seoul that will be repurposed as rental housing for lower income households. Reforms have also focused on increasing private sector engagement by raising the cap on loans to finance housing projects. The authorities are also reviewing stronger financial support for small and mid-sized construction companies by alleviating construction prerequisites for project financing loan guarantees. The authorities do not share staff’s view that the capital gains tax hike may have reduced housing supply, as the number of housing units for sale began to rise in September 2021 after a temporary decline since June.

The authorities deem the pre-sale apartment price and excess gain caps as necessary to maintain house price affordability. The authorities view the price cap as stabilizing house prices for actual buyers. Increasing the ceiling of pre-sale apartment prices would fuel inflation in existing apartments in the surrounding area. The excess gain cap is required to ensure that the gains of private sector led redevelopment contribute to the public good.”

Posted by at 5:23 PM

Labels: Global Housing Watch

Subscribe to: Posts