Showing posts with label Global Housing Watch. Show all posts

Monday, September 10, 2012

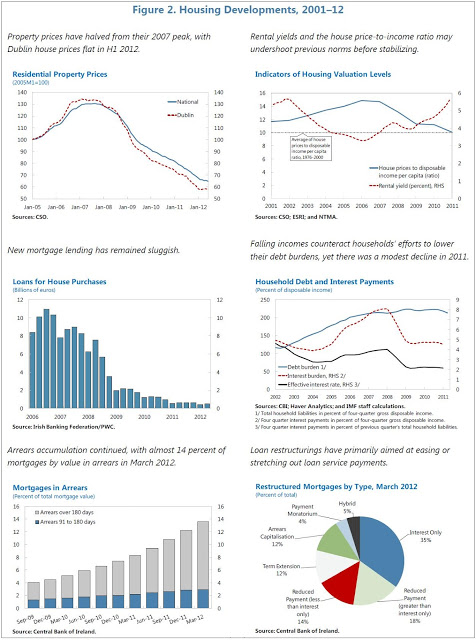

House Prices in Ireland

The new IMF report on Ireland says that “the correction in house prices, one of the largest in recent history, has continued. The decline in nominal residential property prices slowed to 14.4 percent y/y in June 2012. The index has halved since its peak in 2007, eclipsing recent U.K. and U.S. house price declines and comparable to the Japanese and Nordic experiences of the 1990s. As yet, clear signs of stabilization are limited to Dublin house prices (excluding apartments), which, after dropping by 55 percent, have been flat in H1 2012. Rural areas, in contrast, still show signs of oversupply.”

The new IMF report on Ireland says that “the correction in house prices, one of the largest in recent history, has continued. The decline in nominal residential property prices slowed to 14.4 percent y/y in June 2012. The index has halved since its peak in 2007, eclipsing recent U.K. and U.S. house price declines and comparable to the Japanese and Nordic experiences of the 1990s. As yet, clear signs of stabilization are limited to Dublin house prices (excluding apartments), which, after dropping by 55 percent,

Posted by at 4:51 PM

Labels: Global Housing Watch

Monday, September 3, 2012

Global House Price Watch

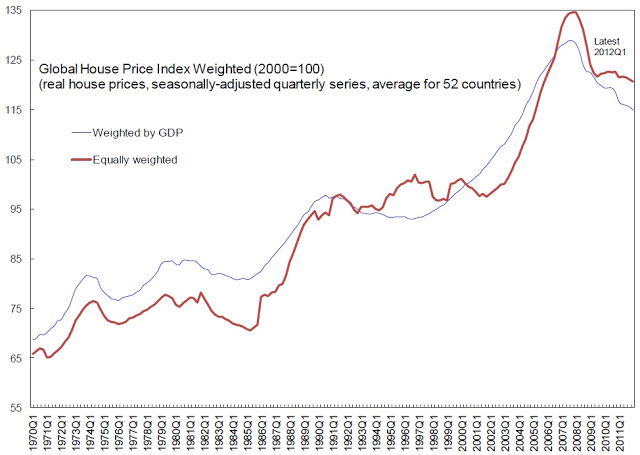

Roller Coaster

weighted average of price in 52 countries—shows no sign of an uptick. The

equally-weighted index moved sideways during the first quarter of 2012 and the

GDP-weighted index continued to decline (see Chart 1).

Chart 1. Global House Price Index

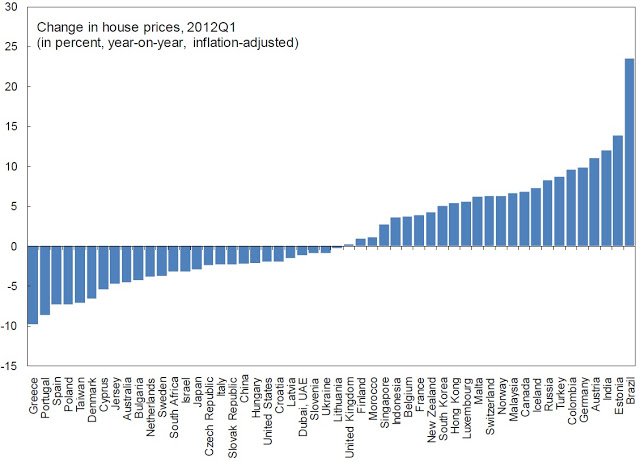

The global index continued to

mask very different developments across countries. House prices have fallen

over the past year in just over half of the countries and risen in the rest, in

Asian countries in particular (see Chart 2).

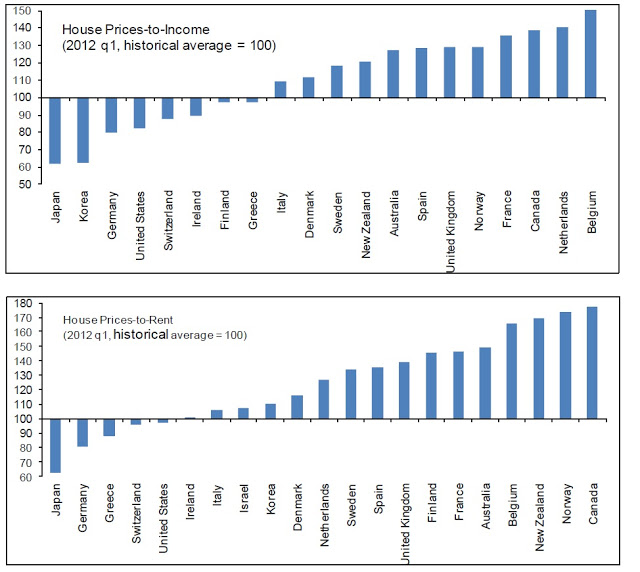

income and the ratio of house prices to rents are two indicators that give a

sense whether prices are likely to decline or rise. The price to income ratio

is the basic affordability measure for housing in a given area and the price to

rent ratio compares the total costs of homeownership vs. the cost of renting a

similar property. If these ratios are above their historical averages, economic

theory suggests that the house prices may decline in the future. The latest

data shows that both ratios continue to remain above—and in many cases well

above—their historical averages, signaling that there may potential for

corrections still to come (see Chart 3).

Relative to Incomes & Rents:

With Historical Averages

determinants of house prices, used in the working paper by Igan and Loungani explains

house price growth based on several short-run factors, such as growth in

incomes, asset prices, and population, and long-run-factors, such as the ratio

of house prices to incomes. The difference between house prices and those

predicted on the basis of these fundamental factors gives another indication of

whether prices may have more room to fall.

exercise show that in many countries the declines in house prices over the past

five years (the ‘actual’) are close to, or even exceed, what was predicted by

the model. But for many countries, house prices are still resisting the

predictions of the model (see Chart 4).

Chart 4. House Prices Changes Compared With Predictions from an Econometric Model

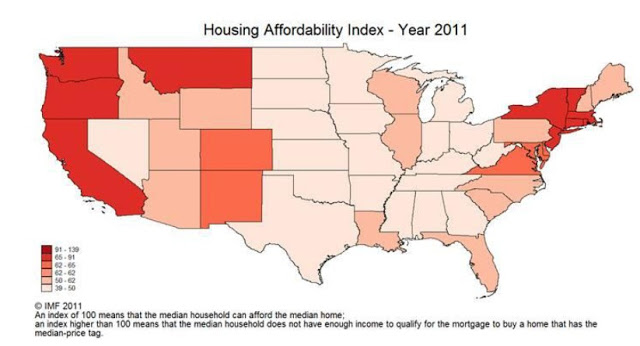

the United States

years, housing affordability improved in most U.S. states last year. In most

U.S. states, a family making the median income for the state could afford the

median house (Chart 5). There were still a few states, along the coasts, where

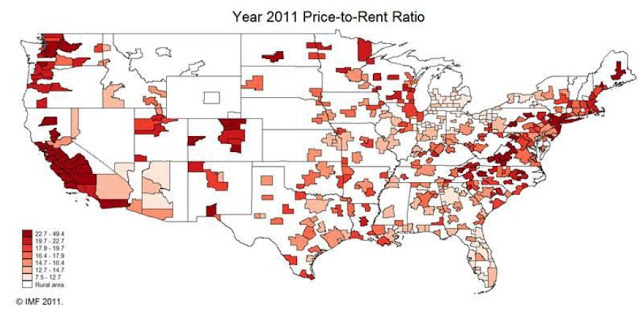

the median house still remained out of reach of the median household. A similar

picture emerges when looking at price-to-rent ratios by metropolitan areas:

house prices remained out of line with rents in some areas along the coasts

(see Chart 6).

studies

monitoring of economic conditions in countries (the so-called “Article IV”

reports), the IMF staff often provides an assessment of conditions in the

housing markets. Readers are encouraged to complement the broad-brush analysis

in this document with the country-focused assessment provided in those reports.

A list of some of the countries for which housing markets were described in

recent reports is given below.

|

Housing Markets in Recent IMF Staff Reports

|

Date of Report

|

|

|

Link to:

|

||

|

Discussion of housing markets

|

Full report (pages on which housing is discussed)

|

|

|

Germany

|

Jul-12

|

|

|

Mar-12

|

||

|

Feb-12

|

||

|

Feb-12

|

||

|

Mar-12

|

||

|

Aug-12

|

||

|

Jun-12

|

||

|

May-12

|

||

|

Aug-12

|

||

This document draws on “Global Housing Cycles”, an IMF Working Paper 12/217 by Deniz Igan and Prakash Loungani (http://www.imf.org/external/pubs/cat/longres.aspx?sk=26229.0). It updates a few of the charts from that paper. As with Working Papers, the views expressed in this document are those of the authors and do not necessarily represent those of the IMF or IMF policy.

The Global House Price

Roller Coaster

Our global index of house prices—a

weighted average of price in 52 countries—shows no sign of an uptick. Read the full article…

Posted by at 11:22 AM

Labels: Global Housing Watch

Monday, August 27, 2012

House Prices in Singapore

In Singapore, “indicators of housing affordability are mixed. House prices have risen more quickly than median incomes, especially for HDB resale housing. In addition, the tighter LtV ceilings raise the bar on qualifying for a housing loan. On the other hand, all-time low mortgage interest rates (about 70 percent of which are at floating rates, currently between 1⅓ percent and 2 percent) have reduced debt servicing costs,” according to a new IMF report on Singapore.

Moreover, it says “Following successive rounds of policy tightening, together with external factors, home prices have remained flat since end˗2011, while the volume of transactions has declined noticeably. In particular, the share of foreign buyers collapsed in Q1:2012 to 5½ percent as a result of new macroprudential measures targeting foreigners and weakening external investment sentiment, with buyers from China falling by nearly 50 percent. The more-than-proportionate decline in purchases by Mainland Chinese may reflect the impact of the economic slowdown in China. Transactions in the luxury market have also fallen. However, the share in total transactions of “shoe box” apartments (with an area of less than 50 square meters) doubled in Q1:2012 to close to 20 percent. While this may reflect the characteristics of new supply coming on-stream, demand for such housing is strong, possibly because of the reduced affordability of standard-size units.”

In Singapore, “indicators of housing affordability are mixed. House prices have risen more quickly than median incomes, especially for HDB resale housing. In addition, the tighter LtV ceilings raise the bar on qualifying for a housing loan. On the other hand, all-time low mortgage interest rates (about 70 percent of which are at floating rates, currently between 1⅓ percent and 2 percent) have reduced debt servicing costs,” according to a new IMF report on Singapore.

Moreover,

Posted by at 9:25 PM

Labels: Global Housing Watch

Thursday, August 2, 2012

House Prices in the US

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP), including loosened eligibility criteria through the elimination of debt service-to-income cutoffs, and the tripling of incentives for investors to carry out principal reductions under HAMP’s Principal Reduction Alternative (PRA) (Box 5). Recent data suggests that the October 2011expansion of HARP seems to have led to a significant increase in HARP refinancing. The share of loans that have benefited from a principal reduction under the modification program (Home Affordable Modification program of HAMP) has also been on the rise, and early signs show that the tripling of the incentives for principal reductions is receiving interest from investors, and is likely to spur further principal reductions in the future. The recent State Attorneys General Settlement with the major banks, which resolved claims about improper foreclosures and abuses in servicing the loans, could lead in the medium run to a non-trivial reduction in foreclosures, including through up to $34 billion of principal reduction. Early signs indicate that the settlement has led banks to delay foreclosures and also to increasingly substitute them with “short sales” of underwater properties, which are less costly and count toward the banks’ commitment for principal reduction under the settlement. The authorities highlighted that greater reliance on short sales, as opposed to foreclosures, could support the housing market going forward.

The mission welcomed this progress, but also noted that more aggressive policy action may be warranted to accelerate the resolution of the housing crisis. As noted in the Fed’s November 2011 white paper, housing markets do not self-correct efficiently and, absent forceful policies to support the market, prices could fall below their equilibrium levels due to feedback loops from prices to demand and supply. If house prices are anticipated to decline, potential buyers could stay out of the market even if interest rates are low. Moreover, a decline in prices reduces housing equity, triggering further defaults and foreclosures. Foreclosures, in turn, put renewed downward pressure on prices, not only by adding to the supply of houses for sale, but also because they lead to a destruction of value and impose “deadweight” losses on the economy, hurting consumer wealth and credit availability.

The IMF’s 2012 annual report on the US economy says that “house prices have shown some firming recently, with a surprising increase in Q1 2012.” It also highlights that

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP),

Posted by at 3:33 PM

Labels: Global Housing Watch

Tuesday, July 3, 2012

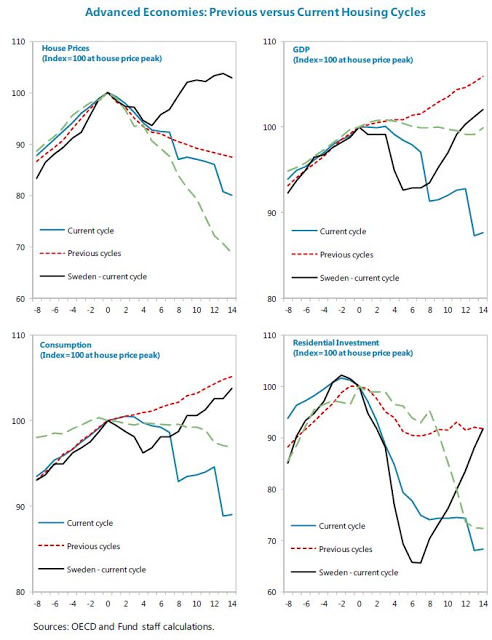

How Vulnerable Is Sweden’s Housing Market?

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value. Indeed, in the two years to 2011 Q2, residential investment (+37 percent) took off again, contrary to more muted developments during the previous recovery, offsetting the sharp drop in new homebuilding experienced during the global crisis.

Going forward, several factors may indicate further downward pressure on house prices. First, price-to-income and price-to-rent ratios remain 1.1 and 1.4 standard deviations respectively above historical averages. Second, staff’s model-based estimates from the Early Warning Exercise (EWE) and Vulnerability Exercise for Advanced Countries (VEA) suggest an overvaluation around 11–12 percent, exceeding the 10 percent threshold. (The EWE real estate model combines these three indicators to create a heat map for house price valuation.) Moreover, the predicted path of house prices based on WEO income projections suggests a decline of almost 5-6 percent through 2017.

These indicators put Sweden among the advanced countries where a house price correction is most likely to take place. Yet, the point estimate for the house price disequilibrium (the difference between actual prices and estimated equilibrium or long-run prices) is not large by historical standards, and Sweden ranks only 9th among 22 advanced economies in the VEA sample in terms of potential overvaluation. Furthermore, other components of residential real estate vulnerability (namely, potential impact on GDP, household balance sheets, and mortgage market characteristics) remain moderate or low in Sweden, compared to other advanced economies. That said, with most mortgages being “rollover” mortgages with terms of at most five years, any future interest rate increases could put additional strains on already highly indebted households.

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value.

Posted by at 2:24 PM

Labels: Global Housing Watch

Subscribe to: Posts