Showing posts with label Global Housing Watch. Show all posts

Saturday, December 29, 2012

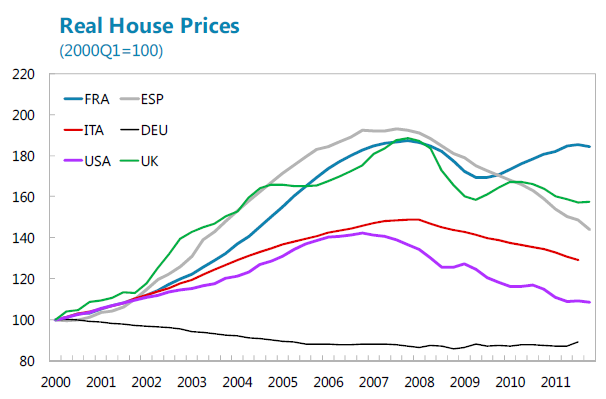

House Prices in France

According to a new report, “Macroeconomic risks related to a correction in real estate prices appear to be relatively contained. The increase in housing prices (over 100 percent in real terms since the mid 1990s) has been supported by stronger fundaments (higher population growth, relatively low supply of housing, and low household indebtedness) than in other countries with rising real estate prices, but also by tax incentives that have fueled demand without addressing underlying supply constraints. There is a perception of price overvaluation, especially in Paris (by 10-20 percent at end-2011 according to staff estimates). However, there is no housing glut or household debt overhang that could trigger a sudden price adjustment. Moreover, stress tests suggest that banks are well placed to absorb the impact of a possible sizable price adjustment owing to tight underwriting criteria (emphasizing sustainability of the borrower’s income, not collateral value) and the absence of nonrecourse loans. The impact of a possible price correction on private demand would also be contained reflecting weak evidence of wealth effects on consumption.”

According to a new report, “Macroeconomic risks related to a correction in real estate prices appear to be relatively contained. The increase in housing prices (over 100 percent in real terms since the mid 1990s) has been supported by stronger fundaments (higher population growth, relatively low supply of housing, and low household indebtedness) than in other countries with rising real estate prices, but also by tax incentives that have fueled demand without addressing underlying supply constraints.

Posted by at 10:25 PM

Labels: Global Housing Watch

Friday, December 28, 2012

Macroprudential Policies and Housing Prices

Several countries in Central, Eastern and Southeastern Europe used a rich set of prudential instruments in response to last decade’s credit and housing boom and bust cycles. A new paper collects detailed information on these policy measures in a comprehensive database covering 16 countries at a quarterly frequency. The authors use this database to investigate whether the policy measures had an impact on housing price inflation. Their evidence suggests that some—but not all—measures did have an impact. These measures were changes in the minimum CAR and non-standard liquidity measures (marginal reserve requirements on foreign funding, marginal reserve requirements linked to credit growth).

Several countries in Central, Eastern and Southeastern Europe used a rich set of prudential instruments in response to last decade’s credit and housing boom and bust cycles. A new paper collects detailed information on these policy measures in a comprehensive database covering 16 countries at a quarterly frequency. The authors use this database to investigate whether the policy measures had an impact on housing price inflation. Their evidence suggests that some—but not all—measures did have an impact.

Posted by at 12:43 AM

Labels: Global Housing Watch

Friday, September 21, 2012

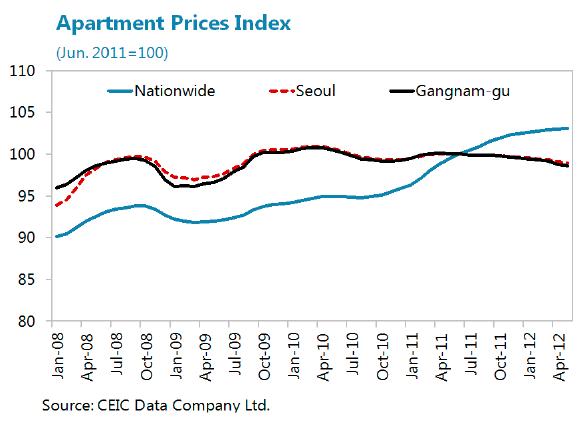

House Prices in Korea

“Housing prices have peaked in Seoul but are rising in the rest of Korea,” according to a new report from the IMF. The report says that “following a protracted period of rising prices, housing prices in Seoul have remained weak due to a still large, albeit declining, inventory of unsold homes and limited expectation of price appreciation. The steady rise in housing prices outside Seoul (which have moderated recently) has been supported by contracting supply, a rapid increase in rents, and a rise in demand supported by strong non-bank lending. In response to the weakness in the Seoul housing market, the authorities have relaxed regulations in May 2012, including by raising loan-to-value (LTV) and debt-to-income (DTI) ratios applied to some high-house price districts.”

“Housing prices have peaked in Seoul but are rising in the rest of Korea,” according to a new report from the IMF. The report says that “following a protracted period of rising prices, housing prices in Seoul have remained weak due to a still large, albeit declining, inventory of unsold homes and limited expectation of price appreciation. The steady rise in housing prices outside Seoul (which have moderated recently) has been supported by contracting supply, a rapid increase in rents, and a rise in demand supported by strong non-bank lending.

Posted by at 1:46 PM

Labels: Global Housing Watch

Monday, September 17, 2012

Global House Prices Still Showing Down Trend

- Prices still falling in roughly half of 54 countries tracked around world

- Brazil, Germany among countries seeing house prices rise

- Within United States, housing picture varies considerably

Price trends vary widely between countries, with Ireland, Greece, Portugal, and Spain seeing the biggest falls in the past year and Brazil and Germany, substantial increases.

While overall the trend is mixed, there is no sign of an uptick in the global index of house prices, a weighted average of prices in 54 countries, according to our research. The index remained level during the second quarter of 2012—the latest quarter for which consistent data is available for a large group of countries—and the GDP-weighted index continued to decline. Continue reading here.

- Prices still falling in roughly half of 54 countries tracked around world

- Brazil, Germany among countries seeing house prices rise

- Within United States, housing picture varies considerably

House prices in the United States have started to pick up a little recently, but globally prices are still on a down trend, according to research by the International Monetary Fund (IMF).

Price trends vary widely between countries, Read the full article…

Posted by at 8:43 PM

Labels: Global Housing Watch

Thursday, September 13, 2012

The Construction Sector: Reeling or Rolling?

sector is looking optimistic. In 2012, total construction spending is expected

to grow by 3 to 9 percent. And the future looks even brighter; total

construction is expected to go up by 6 to 10 percent per year in 2013-2017.

September 6, Ken Simonson, Chief Economist of the Associated General

Contractors, gave a presentation on the economic outlook for construction at an

event hosted by the National Economist Club.

construction sector? Simonson said that office, retail, and lodging

constructions are up due to remodeling. In addition, the production of shale

gas (67 percent increase in 2007-10), and the expansion of the Panama Canal are

driving new activity. Shale gas has both direct and indirect impacts on

construction. For example, the direct impacts include the construction of

access road, site preparation, storage pond, support structures, and pipes for

each well. The indirect impacts include local spending by drilling firms,

workers, royalty holders, among others.

construction in the United States? The expansion of the Panama Canal will

require an upgrade of the ports in the United States to accommodate larger

ships. The upgrade of ports includes investing

in dredging, piers, cranes, and access road. The upgrade will also lead to

possible bridge, tunnel, and highway improvements, resulting in possible

changes in inland distribution and manufacturing. Overall, private

nonresidential and residential spending are leading the way forward for the

construction sector.

According to Simonson, apartments and multi-family housing should boom. On

the other hand, single family housing is growing, but with an uncertain future.

He noted that the apartment vacancy rate is now at a 10-year low and rents are

high.

sector? “Construction added 0 jobs in 2 years, but unemployment is down,”

said Simonson. Basically, workers are leaving for other sectors, going back to school,

and retiring. Simonson presented a chart that showed the change in construction

employment by state in the United States. The map was half or less in green,

meaning jobs available, and half or more in red.

The economic outlook for the construction

sector is looking optimistic. In 2012, total construction spending is expected

to grow by 3 to 9 percent. And the future looks even brighter; total

construction is expected to go up by 6 to 10 percent per year in 2013-2017.

On

September 6, Ken Simonson, Chief Economist of the Associated General

Contractors, gave a presentation on the economic outlook for construction at an

event hosted by the National Economist Club. Read the full article…

Posted by at 3:34 PM

Labels: Forecasting Forum, Global Housing Watch

Subscribe to: Posts