Showing posts with label Global Housing Watch. Show all posts

Wednesday, July 17, 2013

House Prices in China

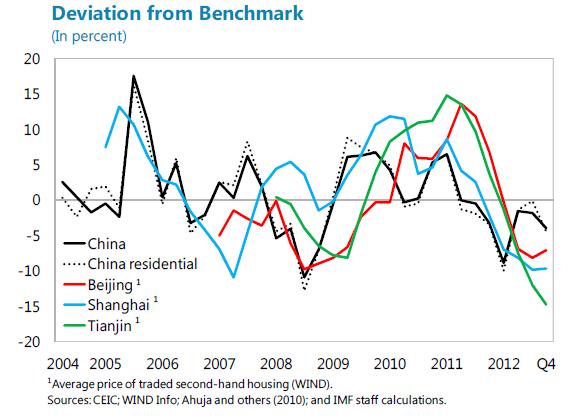

“Real estate has rebounded,” is one of the messages of the latest IMF’s economic report on China. The report says, “Real estate investment in 2012 accounted for 12½ percent of China’s GDP, 14 percent of total urban employment, and rising share of FAI. Lending to real estate is primarily for household mortgages and has slowed recently. The real estate market has shown signs of a recovery lately, with moderate growth in prices, investment, and sales and affordability indices have been improving and prices now seem to be broadly in line or even below fundamentals nationwide and in major cities. Over the medium term, residential construction is likely to slow as the market matures.”

“Real estate has rebounded,” is one of the messages of the latest IMF’s economic report on China. The report says, “Real estate investment in 2012 accounted for 12½ percent of China’s GDP, 14 percent of total urban employment, and rising share of FAI. Lending to real estate is primarily for household mortgages and has slowed recently. The real estate market has shown signs of a recovery lately, with moderate growth in prices, investment, and sales and affordability indices have been improving and prices now seem to be broadly in line or even below fundamentals nationwide and in major cities.

Posted by at 6:43 PM

Labels: Global Housing Watch

Friday, July 12, 2013

House Prices in Malta

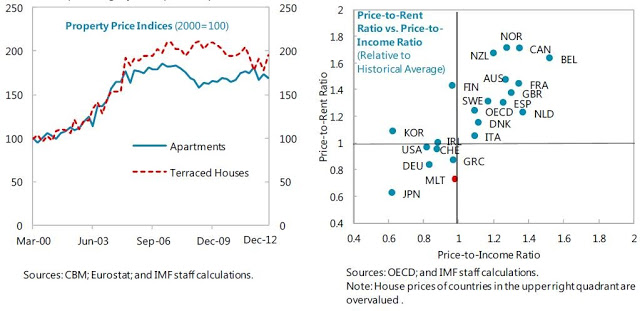

“House prices slightly below pre-crisis peaks,” says IMF’s report on Malta that was released today. According to the report, “the fall in property prices was not drastic. The decline in property prices during the crisis was 8 percent. The loss in household wealth from property was thus moderate. Malta’s house prices are one of the most undervalued amongst the advanced economy countries, indicating there is no potential risk of correction in the property market. Both the price-to-income and price-to rent ratio remain one of the lowest among the advanced economies.”

“House prices slightly below pre-crisis peaks,” says IMF’s report on Malta that was released today. According to the report, “the fall in property prices was not drastic. The decline in property prices during the crisis was 8 percent. The loss in household wealth from property was thus moderate. Malta’s house prices are one of the most undervalued amongst the advanced economy countries, indicating there is no potential risk of correction in the property market. Both the price-to-income and price-to rent ratio remain one of the lowest among the advanced economies.”

Posted by at 9:41 PM

Labels: Global Housing Watch

Wednesday, July 10, 2013

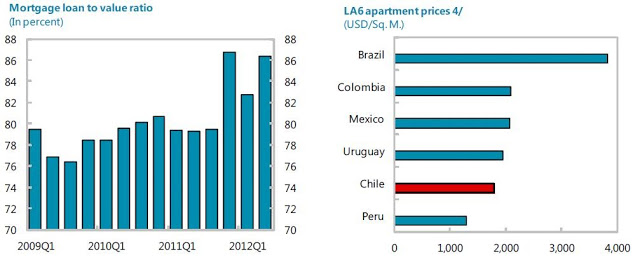

House Prices in Chile

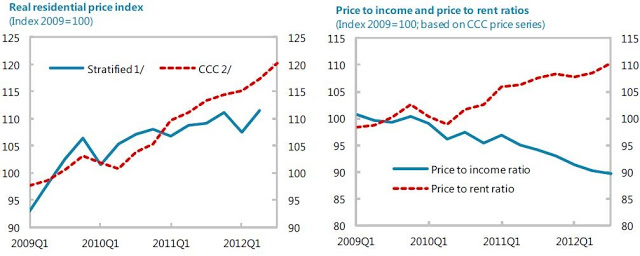

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011, as highlighted in recent central bank financial stability reports. Another issue is the above-mentioned worsening in construction companies’ financial strength. As for construction, while residential housing activity seems to be cooling off, commercial real estate (for which data are spotty) remains hot with a substantial amount of office space being completed in 2013-14.”

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011,

Posted by at 2:39 PM

Labels: Global Housing Watch

Wednesday, June 19, 2013

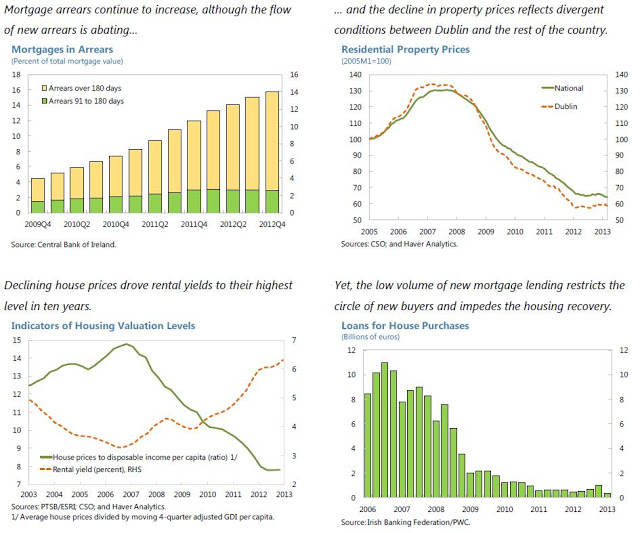

House Prices in Ireland

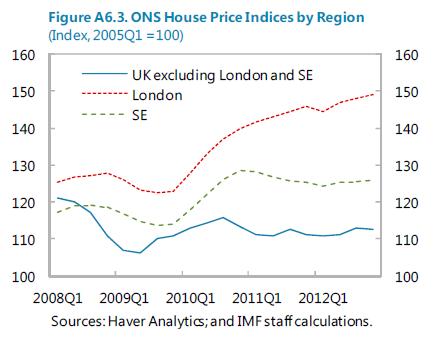

“House prices slipped back reflecting developments outside Dublin. After stabilizing over much of 2012, national residential property prices fell 2.6 percent in the first quarter of 2013, bringing the index to a new low 51 percent below its pre-crisis peak,” according a new IMF report on Ireland. What explains the drop in prices? The report says that “this decline was driven by an almost 4 percent price fall outside Dublin, reflecting divergent market conditions—the stock of property available for sale in Dublin amounts to around 6 months‘ supply, Read the full article…

Posted by at 4:49 PM

Labels: Global Housing Watch

Tuesday, May 21, 2013

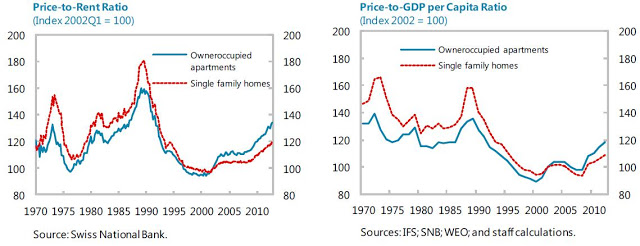

House Prices in Switzerland

“House prices are high, but it’s too early to call it a bubble,” according to an IMF study on the Swiss Housing Market: What are the risks? It says that “real house prices are high, and at an all-time high for owner-occupied apartments. Prices have been on an increasing trend since the late 1990s and the average price for a single family home has increased by about 49 percent. Prices for owner occupied apartments have increased even more (72 percent) and in the last four years the annualized price increase (5 1/2 percent) substantially exceed nominal GDP growth. When deflating house prices by the CPI, owner-occupied apartment prices are slightly above the peak of the boom-bust period in the late 80s to early 90s. Single family home prices are still below the peak, but still high by historic standards. Residential house price increases are especially pronounced in certain segments and region. Turning to regional patterns, Geneva stands out with price increases far exceeding the other regions in both the single family home and the owner occupied segments. It is also important to note that the price increases started from already high price levels.”

However, “current prices look less elevated when compared to income and rents. Following the

boom in the late 80s housing prices fell dramatically and their subsequent growth remained

subdued relative to growth in rents and in GDP per capita until the late 2000s, when housing price growth accelerated. While these ratios are still well below the levels reached at the peak of the previous boom, the ratio of price to rents for owner occupied apartments is already 15 percent above its long-term average.”

“House prices are high, but it’s too early to call it a bubble,” according to an IMF study on the Swiss Housing Market: What are the risks? It says that “real house prices are high, and at an all-time high for owner-occupied apartments. Prices have been on an increasing trend since the late 1990s and the average price for a single family home has increased by about 49 percent. Prices for owner occupied apartments have increased even more (72 percent) and in the last four years the annualized price increase (5 1/2 percent) substantially exceed nominal GDP growth.

Posted by at 2:47 PM

Labels: Global Housing Watch

Subscribe to: Posts