Showing posts with label Global Housing Watch. Show all posts

Wednesday, March 4, 2015

House Prices in Malta

“After a period of downward correction in 2008-09, Malta’s housing market seems to have stabilized,” notes the latest IMF report on Malta. However, the report says that “One of the main risks facing core domestic banks relates to their exposure to the real estate sector. Around two thirds of loans extended by banks are secured with real estate collateral, and mortgages are one of the few segments of bank loans which have been increasing recently (unlike loans to NFCs). Read the full article…

Posted by at 2:58 PM

Labels: Global Housing Watch

Wednesday, February 25, 2015

Global Housing Watch Newsletter

- IMF’s latest assessment on Canada’s housing market and a new working paper on differences in house price behavior across advanced and emerging markets.

- Experts views on how diverging monetary policy rates and currency volatility will affect housing markets.

- Was fraud a cause of the U.S. housing crash of seven years ago? Yes and no, says new research.

- Other views and analysis on housing markets:

- Cross-country work: two reports from a World Economic Forum initiative on detecting when and why housing bubbles emerge and how consequences can be mitigated. Another report from McKinsey Global Institute that examines the evolution of debt across countries and assesses the implications of higher leverage in the global economy. Also, a tool that map the institutional components of property markets and evaluate their effectiveness, developed by Center for International Private Enterprise and the International Real Property Foundation. Finally, the latest house price developments by the BIS.

- A new book: Zillow Talk: The New Rules of Real Estate by Spencer Rascoff and Stan Humphries

- Country specific: Australia, Belgium, Canada, China, Denmark, Germany, Hong Kong, India, Israel, New Zealand, Peru, Sweden, Singapore, Spain, Switzerland, United Kingdom, and United Sates.

The February issue includes:

- IMF’s latest assessment on Canada’s housing market and a new working paper on differences in house price behavior across advanced and emerging markets.

- Experts views on how diverging monetary policy rates and currency volatility will affect housing markets.

- Was fraud a cause of the U.S. housing crash of seven years ago? Yes and no, says new research.

- Other views and analysis on housing markets:

- Cross-country work: two reports from a World Economic Forum initiative on detecting when and why housing bubbles emerge and how consequences can be mitigated.

Posted by at 5:46 PM

Labels: Global Housing Watch

Thursday, February 19, 2015

House Prices in Slovenia

House prices are are still declining in Slovenia, according to the latest IMF economic report on Slovenia.

Posted by at 3:40 PM

Labels: Global Housing Watch

Sunday, February 1, 2015

Global Housing Watch Newsletter

This newsletter aims to present a snapshot of the month’s news and research on global housing markets. If you have suggestions on new material that could be included, you can send it by clicking here. The January 2015 issue includes:

- IMF issues report on housing markets in Denmark, Ireland, the Netherlands and Spain

- The impact of decline in oil prices on housing

- Housing affordability emerging as an issue

- News and research for the following countries: Brazil, Canada, China, Germany, Hong Kong, Israel, Netherland, Norway, Philippines, Singapore, South Korea, United Kingdom, United States, and cross country research.

Read the full newsletter here.

This newsletter aims to present a snapshot of the month’s news and research on global housing markets. If you have suggestions on new material that could be included, you can send it by clicking here. The January 2015 issue includes:

- IMF issues report on housing markets in Denmark, Ireland, the Netherlands and Spain

- The impact of decline in oil prices on housing

- Housing affordability emerging as an issue

- News and research for the following countries: Brazil,

Posted by at 3:47 PM

Labels: Global Housing Watch

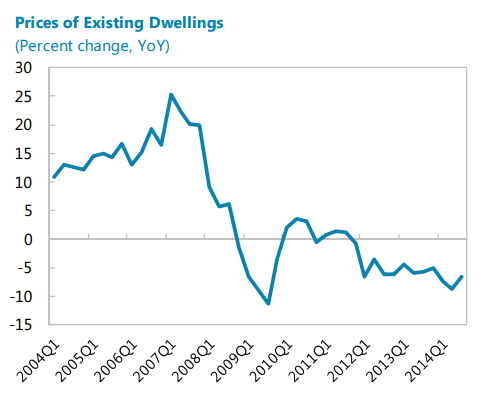

House Prices in Advanced and Emerging Economies

In a new paper, Alessandro Rebucci (Johns Hopkins University) and his co-authors have assembled a database that expands the availability of historical house price data for emerging markets.The authors used this database to study the impact of increased global liquidity—an increase in the international supply of credit—on house prices. The paper finds that an increase in global liquidity by 1 percent of world GDP raises house prices in emerging markets by 3 percent, over three times the impact in advanced economies. Read the full article…

Posted by at 3:19 PM

Labels: Global Housing Watch

Subscribe to: Posts