Showing posts with label Global Housing Watch. Show all posts

Wednesday, July 5, 2017

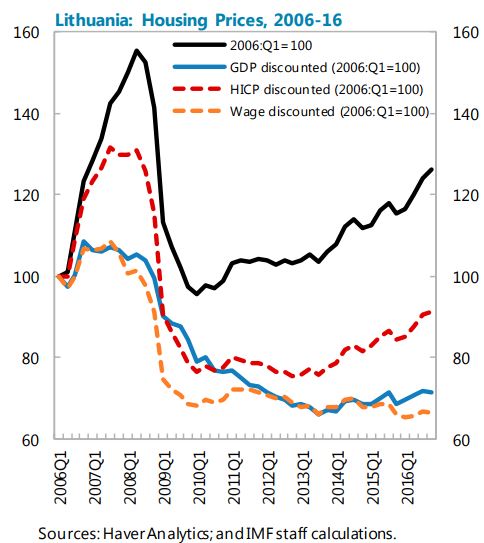

House Prices in Lithuania

IMF’s latest report on Lithuania says that: “Housing price developments in Lithuania are not an immediate concern, but the Bank of Lithuania rightly keeps an eye on possible overheating and froth in certain market segments. Macroprudential tools are in place to step in if needed. The strength of some small non-systemic financial institutions needs continued attention and credit union reform should be completed in line with current plans.”

IMF’s latest report on Lithuania says that: “Housing price developments in Lithuania are not an immediate concern, but the Bank of Lithuania rightly keeps an eye on possible overheating and froth in certain market segments. Macroprudential tools are in place to step in if needed. The strength of some small non-systemic financial institutions needs continued attention and credit union reform should be completed in line with current plans.”

Posted by at 1:08 PM

Labels: Global Housing Watch

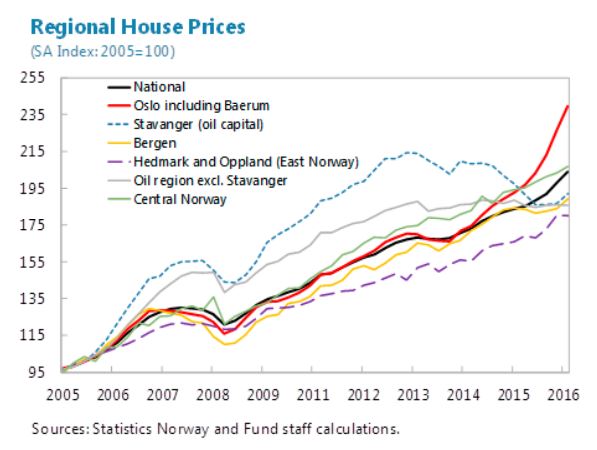

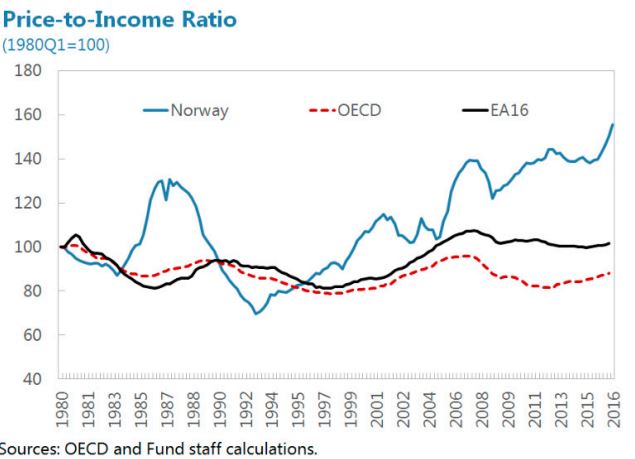

Are House Prices Overvalued in Norway?

From a new IMF paper on: Are House Prices Overvalued in Norway? – A Cross-Country Analysis:

“High and overvalued house prices are a source of vulnerability in Norway, in view of the importance of the housing market to both financial and macroeconomic stability. A large correction of house prices, driven by slower real income growth, a reverse in sentiment, or interest rate hikes could weaken household balance sheets and depress private demand, and in turn adversely affect corporate and bank earnings. The authorities have been vigilant about the risks and have implemented a list of measures to strengthen the resilience of banks and households, including additional bank capital buffer requirements in line with Basel III/CRD IV, higher risk weights on residential mortgages using IRB models, tighter mortgage regulations, and the introduction of the debt-to-income limit of five times the borrower’s gross annual income to complement the loan-to-value (LTV) limits and affordability tests. Nevertheless, further targeted macroprudential measures should be considered to help contain systemic risks if vulnerabilities in the housing sector intensify, including: tighter LTV limits, a reduction in banks’ scope for deviating from mortgage regulations, and/or higher mortgage risk weights.

In the longer term, the macro-financial resilience of the economy to housing market shocks should be enhanced through tax reform and structural measures. A stable housing market (without pronounced boom-bust cycles) would contribute to smoother economic development. While macroprudential measures play an important role in containing the buildup of financial imbalances, a holistic approach is needed to fundamentally address the issue: (i) reducing the generous tax preferences for housing investment would help prevent demand distortions and excessive leverage, thereby dampening housing cycles; (ii) while the recent streamlining of building codes―which shortened the time needed to obtain a building permit and finish construction—is welcome, relaxing land-use and remaining constraints on new property construction, including at the municipal level, should facilitate a more efficient use of land and a flexible adjustment of housing supply, which will mitigate house price growth; and (iii) a more developed rental market would help relieve demand pressures—especially in view of the recent large influx of asylum seekers―as well as support labor mobility across regions as the economy goes through structural change.”

From a new IMF paper on: Are House Prices Overvalued in Norway? – A Cross-Country Analysis:

“High and overvalued house prices are a source of vulnerability in Norway, in view of the importance of the housing market to both financial and macroeconomic stability. A large correction of house prices, driven by slower real income growth, a reverse in sentiment,

Posted by at 11:31 AM

Labels: Global Housing Watch

Housing View – July 5, 2017

On cross-country:

- Prime Global Rental Index – Q1 2017 – Knight Frank

- EMF Quarterly Review – Q1 2017 – European Mortgage Federation

- Houses Across Time and Across Place – Centre for Economic Policy Research

On the US:

- How Exclusionary Zoning Comes at a Loss for Housing and Jobs – Foundation for Economic Education

- Moving to Opportunity: Why Breaking Family Ties Isn’t So Easy – Zillow

- Developing Inclusive Communities: Challenges and Opportunities for Mixed-Income Housing – Federal Reserve Bank of Atlanta

- Community Banks Account for Nearly Half of Residential Construction Loans – Eye on Housing

- Estimating the Total U.S. Demand for Rental Housing – National Multifamily Housing Council

- Incomes, Migration and Housing Affordability – Oregon Office of Economic Analysis

On other countries:

- The role of foreign investors in the London residential market – London School of Economics

- [United Kingdom] Low-cost housing schemes have little impact on social mobility – London School of Economics

- German Housing Prices: Boom Time Over? – Handelsblatt Global

- [Canada] B.C. throne speech acknowledges importance of housing supply on affordability – Fraser Institute

- [United Kingdom] Grenfell: the anatomy of a housing disaster – Financial Times

- Irish House Price Report Q2 2017 – Daft.ie

- Moving to a New Housing Pattern? New Trends in Housing Supply and Demand in Times of Changing. The Portuguese Case – Critical Housing Analysis

- Some Thoughts on Massive Affordable Housing Schemes under the Pressure of Commodity Housing Inventory in China’s Cities – Hubei University

On cross-country:

- Prime Global Rental Index – Q1 2017 – Knight Frank

- EMF Quarterly Review – Q1 2017 – European Mortgage Federation

- Houses Across Time and Across Place – Centre for Economic Policy Research

On the US:

- How Exclusionary Zoning Comes at a Loss for Housing and Jobs – Foundation for Economic Education

- Moving to Opportunity: Why Breaking Family Ties Isn’t So Easy – Zillow

- Developing Inclusive Communities: Challenges and Opportunities for Mixed-Income Housing – Federal Reserve Bank of Atlanta

- Community Banks Account for Nearly Half of Residential Construction Loans – Eye on Housing

- Estimating the Total U.S.

Posted by at 7:31 AM

Labels: Global Housing Watch

Wednesday, June 28, 2017

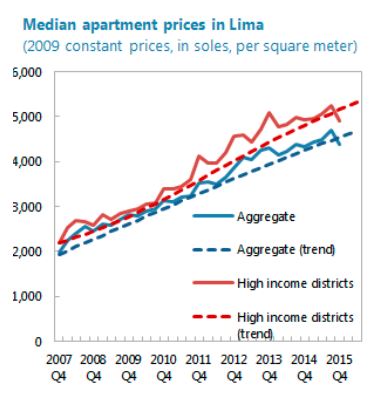

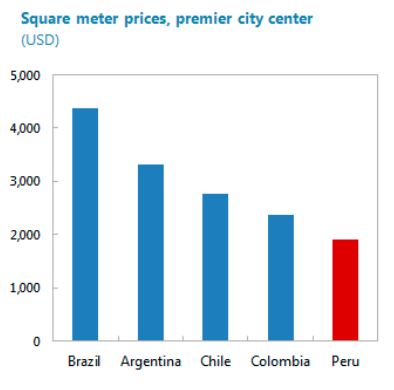

House Prices in Peru

“The property sector has grown rapidly, though there has been some price moderation recently and indicators do not suggest overheating. Prices have risen over the decade, in tandem with Peru’s economic expansion. In Q2 2016, the growth in median apartment prices in Lima softened compared to Q2 2015, but remained well above the 5-year average. Valuation indicators show that Peru’s property market is on an average footing compared to regional peers (…). The country also faces a housing deficit, particularly in the lower-income segments, and buying patterns do not appear speculative. Furthermore, property price indices in Peru only reflect the capital, Lima, which has a higher population growth and urbanization level than the rest of the country”, according to the IMF’s annual economic report on Peru.

“The property sector has grown rapidly, though there has been some price moderation recently and indicators do not suggest overheating. Prices have risen over the decade, in tandem with Peru’s economic expansion. In Q2 2016, the growth in median apartment prices in Lima softened compared to Q2 2015, but remained well above the 5-year average. Valuation indicators show that Peru’s property market is on an average footing compared to regional peers (…). The country also faces a housing deficit,

Posted by at 3:39 PM

Labels: Global Housing Watch

Tuesday, June 27, 2017

Housing View – June 27, 2017

On macroprudential policy:

- Stanley Fischer on Housing and Financial Stability – Federal Reserve Board

- DNB-Riksbank Macroprudential Conference – De Nederlandsche Bank

On cross-country:

- Global House Price Index – Q1 2017 – Knight Frank

- Q1 2017: World’s housing markets poised to slow, though the boom continues strongly in Europe, Canada, and some parts of Asia – Global Property Guide

- Global developments in residential property prices – Bank for International Settlements

- Europe’s Next Housing Boom Raises Red Flags in Ex-Communist East – Bloomberg

- Relevamiento Inmobiliario de América Latina – Universidad Torcuato Di Tella

- Recent Trends and Developments in European Mortgage Markets – CEPS

- House prices and monetary policy in the euro area: evidence from structural VARs – European Central Bank

- A housing policy that could almost pay for itself? Think retrofitting – World Bank

On the US:

- Is a Bubble Brewing in the Multifamily Housing Market? – Federal Reserve Bank of St. Louis

- The State of the Nation’s Housing 2017 – Harvard Joint Center for Housing Studies

- Does it matter whether those who lost their homes during the crisis come back to the housing market? – Federal Reserve Bank of Richmond

- Housing Constraints and Spatial Misallocation – University of California, Berkeley

- Dynamics of Housing Debt in the Recent Boom and Great Recession – NBER

On other countries:

- Is Australia’s property market overheating? – The Economist

- The lessons from Canada’s attempts to curb its house-price boom – The Economist

- Czech central bank moves to rein in lending in ‘overvalued’ property market – Financial Times

- How can we dampen the build-up of housing price bubbles? – Bank of Finland

- A review of residential mortgage lending in 2016 – Central Bank of Ireland

- [New Zealand] House prices slow, and will likely keep slowing – CoreLogic

- South Korea tightens rules on housing to restrain buying frenzy in some cities – Reuters

- [Spain] Buen desempeño del mercado inmobiliario en 1T17 – BBVA

On macroprudential policy:

- Stanley Fischer on Housing and Financial Stability – Federal Reserve Board

- DNB-Riksbank Macroprudential Conference – De Nederlandsche Bank

On cross-country:

- Global House Price Index – Q1 2017 – Knight Frank

- Q1 2017: World’s housing markets poised to slow, though the boom continues strongly in Europe, Canada, and some parts of Asia – Global Property Guide

- Global developments in residential property prices –

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts