Showing posts with label Global Housing Watch. Show all posts

Tuesday, July 18, 2017

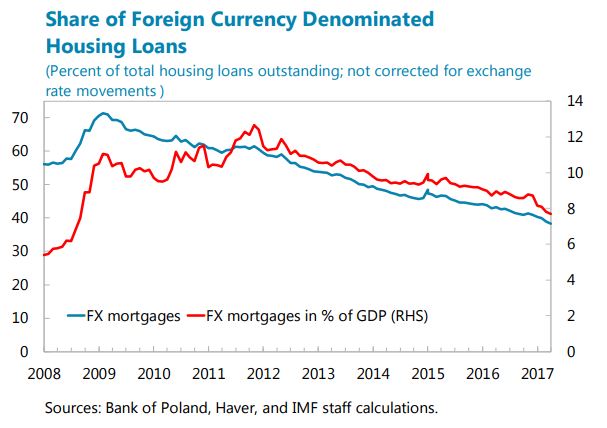

Housing in Poland

The IMF’s latest report on Poland notes that “the stock of foreign-currency mortgages continues to decline”.

The IMF’s latest report on Poland notes that “the stock of foreign-currency mortgages continues to decline”.

Posted by at 5:09 PM

Labels: Global Housing Watch

Monday, July 17, 2017

Housing View – July 17, 2017

On cross-country:

- How Advanced Economies Tackle Housing Market Imbalances: Lessons for Canada – IMF

- Confronting the Urban Housing Crisis in the Global South: Adequate, Secure, and Affordable Housing – World Resource Institute

- Housing and the tax system: how large are the distortions in the euro area? – European Central Bank

On the US:

- Homeownership and the Racial Wealth Divide – Federal Reserve Bank of St. Louis

- Are Immigrant and Minority Homeownership Rates Gaining Ground in the US? – SSRN

- HUD Secretary Shaun Donovan on all things housing – Milken Institute

- Linking Residents to Opportunity: Gentrification and Public Housing – US Department of Housing and Urban Development

On other countries:

- [Australia] The Rise and Rise of Medium Density Housing – CoreLogic

- [Canada] Macroprudential Tools at Work in Canada – IMF

- [Ghana] Housing transformation and livelihood outcomes in Accra, Ghana – ScienceDirect

- Israel Faces End of Decade-Long Housing Boom – Bloomberg

- [Japan] The Reverse Mortgage Market in Japan and Its Challenges – U.S. Department of Housing and Urban Development

- [Norway] Chart of the Week: Norway’s Home-Price Boom – IMF

- UK Residential Market Update – Knight Frank

- [United Kingdom] English Housing Survey 2015 to 2016: potential for stock improvements – UK Gov

On cross-country:

- How Advanced Economies Tackle Housing Market Imbalances: Lessons for Canada – IMF

- Confronting the Urban Housing Crisis in the Global South: Adequate, Secure, and Affordable Housing – World Resource Institute

- Housing and the tax system: how large are the distortions in the euro area? – European Central Bank

On the US:

- Homeownership and the Racial Wealth Divide – Federal Reserve Bank of St.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 13, 2017

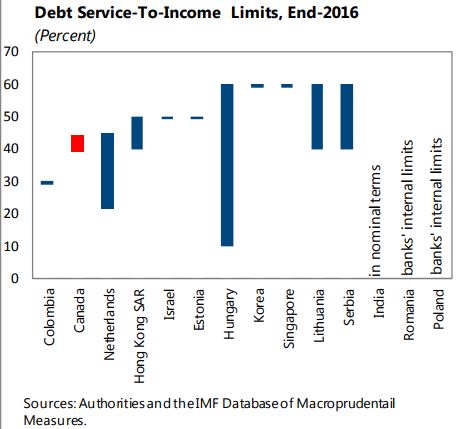

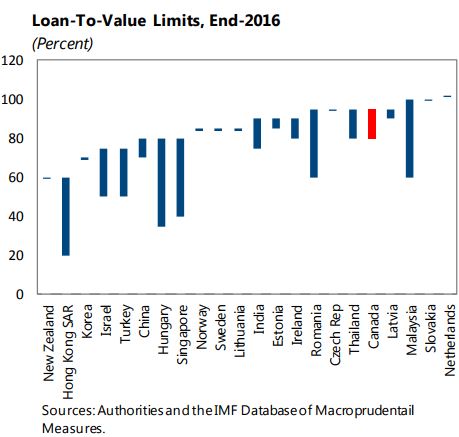

How Advanced Economies Tackle Housing Market Imbalances: Lessons for Canada

A new IMF study on says that:

“Low interest rates and abundant liquidity globally has led to significant demand pressures on housing markets around the world. Economies have tackled growing imbalances with the continued tightening of prudential-based tools and, in some cases, targeted tax measures. While the outcomes of these policies are not straightforward to assess, and up-to-date empirical evidence is not readily available for the individual economy cases, the measures likely have slowed down increases in house prices and household indebtedness, and improved the resilience of the financial sector to housing market related shocks. The trend towards coordinating prudential measures with tax-based measures is likely to improve the overall effectiveness of macroprudential policy in cases when speculative and investment demand play a major role.”

Another IMF study on Canada says that:

“The aim of this paper is to assess which macroprudential policy measures have been effective in containing house price and mortgage credit growth in Canada and other economies. Our analysis indicates that macroprudential policy measures have had a moderating effect on house prices and mortgage credit in Canada since 2010. International experience suggests that lower caps on debt-service-to-income (DSTI) ratios and loan-to-value ratios could be effective in containing both mortgage credit and house price growth.”

A new IMF study on says that:

“Low interest rates and abundant liquidity globally has led to significant demand pressures on housing markets around the world. Economies have tackled growing imbalances with the continued tightening of prudential-based tools and, in some cases, targeted tax measures. While the outcomes of these policies are not straightforward to assess, and up-to-date empirical evidence is not readily available for the individual economy cases, the measures likely have slowed down increases in house prices and household indebtedness,

Posted by at 12:26 PM

Labels: Global Housing Watch

Wednesday, July 12, 2017

Housing Market in Germany

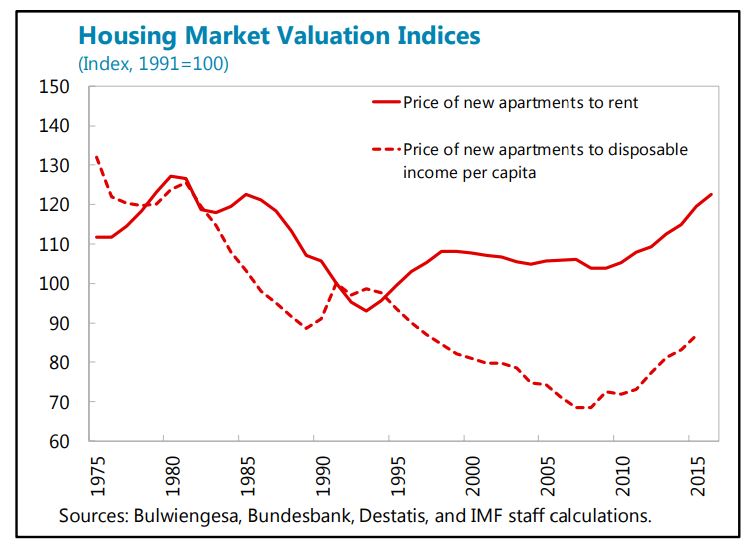

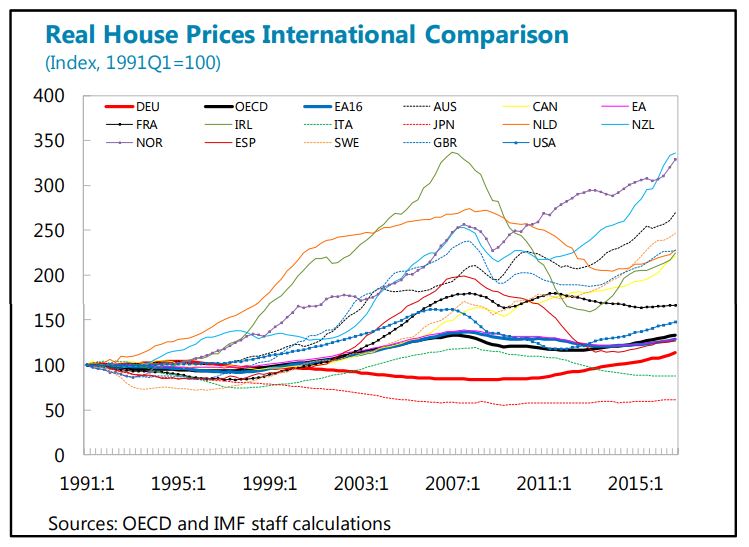

IMF’s latest report on Germany says that:

“At the aggregate level, housing affordability remains good, and price developments moderate in international comparison, but growing regional differences warrant close monitoring. House prices have continued to accelerate but their level remains moderate, as do various indicators of mortgage affordability (price-to-rent, price-to-income). However, the picture is different when regional developments are considered. While house prices continue to fall in some rural areas, price growth has reached double-digits in large cities and university towns. In certain urban areas, overvaluation may amount to 30 percent according to the Bundesbank’s latest estimates. While there is no comprehensive data available on regional mortgage growth, there is some anecdotal evidence of looser underwriting standards in some areas.

Relaxing housing supply constraints would help mitigate price pressures. Last year the government adopted a package of measures to address supply shortages and improve affordability. The plan is progressing in coordination with local authorities and includes stepping up the sales of federally-owned land and properties below market price for affordable housing projects, more funds for social housing, and the promotion of building code harmonization. However, the authorities estimate that the supply of new housing units remained below demand in 2016. To significantly boost supply in the short term, these measures must be complemented by further encouragement for local authorities to relax zoning and height restrictions in areas under pressure. Lowering the effective transaction tax rate on new construction, as recommended by staff in the past, would also be helpful in this regard.

New legislation introducing macroprudential instruments for the real estate market was approved, but left the toolkit incomplete and important data gaps unaddressed. The new legislation broadens the macroprudential toolkit to include loan-to-value and amortization requirements, but does not include either debt-to-income or debt-service-to-income limits— instruments designed to limit borrower vulnerability to income and interest rate shocks, and ensure affordability. Most importantly, the new law does not include any provision for a granular, loan-by loan database, a central tenet of past staff recommendation to ensure the effective implementation of macroprudential tools. At a minimum, a regular (at least annual) survey should be conducted in hotspots to collect information on individual loans, and assess household leverage, loan affordability and the concentration of banks’ exposure.”

IMF’s latest report on Germany says that:

“At the aggregate level, housing affordability remains good, and price developments moderate in international comparison, but growing regional differences warrant close monitoring. House prices have continued to accelerate but their level remains moderate, as do various indicators of mortgage affordability (price-to-rent, price-to-income). However, the picture is different when regional developments are considered. While house prices continue to fall in some rural areas, price growth has reached double-digits in large cities and university towns.

Posted by at 10:57 AM

Labels: Global Housing Watch

Monday, July 10, 2017

Housing View – July 10, 2017

On cross-country:

- Global Residential Cities Index – Q1 2017 – Knight Frank

- Economic Activity, Credit Market Conditions, and the Housing Market – Macroeconomic Dynamics

On the US:

- FED Governor Jerome H. Powell on The Case for Housing Finance Reform – Speech, Event Video, and Coverage: Financial Times

- Are Home Prices Really Above Their Pre-Recession Peak? – Harvard Joint Center for Housing Studies

- Housing Sentiment at Record High as Consumers’ Confidence in Home-Selling Environment Strengthens – Fannie Mae

- What you want to know about California’s failed housing affordability law – Los Angeles Times

- It’s time for cities to start building their fair share of housing – Los Angeles Times

On other countries:

- Australian Housing ‘Bubble’ Fears Overblown, HSBC Economist Says – Bloomberg

- [Canada] Rental Ownership Structure in Canada – Canada Mortgage and Housing Corporation

- [Canada] Ontario’s One Cylinder Economy: Housing in Toronto and Weak Business Investment – Fraser Institute

- [Canada] Restrictive Land-Use Regulation: Strategies, Effects and Solutions – Frontier Centre for Public Policy

- [China] Relationship between the Chinese housing and marriage markets – VoxDev

- [China] The bubble dynamics of China’s housing boom – VoxDev

- [Germany] Cheap credit not fuelling German real estate bubble for now- central banker – Reuters

- [Norway] Are House Prices Overvalued in Norway? – IMF

- [Switzerland] UBS and Credit Suisse cut back on domestic mortgages – Financial Times

On cross-country:

- Global Residential Cities Index – Q1 2017 – Knight Frank

- Economic Activity, Credit Market Conditions, and the Housing Market – Macroeconomic Dynamics

On the US:

- FED Governor Jerome H. Powell on The Case for Housing Finance Reform – Speech, Event Video, and Coverage: Financial Times

- Are Home Prices Really Above Their Pre-Recession Peak?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts