Showing posts with label Global Housing Watch. Show all posts

Wednesday, September 13, 2017

Increasing Resilience to Large and Volatile Capital Flows: The Role of Macroprudential Policies in Sweden

On Sweden, the new IMF report says that:

“The robust economy and low interest rates, together solid population growth and inelastic housing supply, boosted housing prices and hence household debt:

- As a percentage of disposable income, household indebtedness has almost doubled since 1996 and now stands at about 180 percent, with a growing share of new borrowers taking on high debts relative to income. The growth in debt has primarily reflected rising housing prices owing to prolonged supply demand imbalances exacerbated by low amortization, low interest rates, and tax incentives to hold real estate and to finance it with debt.

- House prices have also doubled in real terms since 1996 and Swedish homes are highly valued from a historical perspective. The price-to-income ratio is 40 percent above

its 20-year average—highest among the OECD countries. Model-based estimates of overvaluation are notably smaller, at about 10 percent, but are subject to significant

uncertainty.Cheap wholesale funding, from a mix of Swedish and foreign sources, including in foreign currency, has underpinned mortgage growth. Customer deposits represent around 40 percent of banks’ total funding since Swedish households invest a large proportion of savings in mutual funds rather than bank accounts, in part reflecting high mandatory contributions to

pension funds (Figure 2). With banks having one of the highest loan-to-deposit ratios in European countries (about 200 percent), the long-maturity residential mortgages rely on wholesale funding, such as covered bonds, unsecured bonds and commercial paper, giving rise to refinancing risks. Nonetheless, a substantial portion of this wholesale funding comes from Swedish pension funds and insurance companies, who may be less flighty investors. About half of the wholesale funding is in foreign currency predominantly in euro and USD. The Riksbank estimates that about 25 percent of the major banks’ foreign funding is used to fund Swedish assets. The banks use currency swaps to hedge this funding to match their SEK denominated loans.Home ownership financed by high levels of mortgage debt make households vulnerable to falling house prices. Although the immediate effect of a potential decline in housing prices on Swedish household default rates appears to be contained, the indirect macroeconomic impact can be sizeable. Analysis by Sweden’s National Institute of Economic Research finds a 20 percent drop in housing prices would lead to a recession-like impact on household consumption and unemployment, with an even greater impact if this drop coincided with a global downturn. In an extreme but plausible scenario, this can combine with a broader loss of confidence in housing collateral and potentially higher funding interest rates. Given the

high interconnectedness among the Nordic-Baltic financial systems, such a shock could also have significant cross-border spillovers.Swedish banks’ heavy reliance on wholesale funding in FX could reinforce the risks. As illustrated by the financial crisis, the build-up of unease on international financial markets from 2007 had an impact on the Swedish covered bond market. During the second half of 2007, foreign investors reduced their holdings of Swedish covered bonds by almost one-third affecting the banks’ possibilities of obtaining funding and prompting government intervention.

The authorities have responded to rising household debt with a range of macroprudential measures to protect the resilience of households and the banking sector (Table 1). An 85 percent cap on loan-to-value (LTV) ratios was adopted in 2010 in order to protect households against the risk of negative equity which could increase the risk of default.10 A requirement for a stress test on households at the time of mortgage origination aims to ensure households have adequate buffers against significantly higher interest rates. In May 2013, the FSA introduced a 15 percent floor for risk weights on Swedish residential mortgages to address IRB model risks. In 2014, the floor was raised to 25 percent as a macroprudential measure, to target risks arising from high growth rates in residential mortgage lending. The countercyclical capital buffer has been increased three times since 2015 to support banks’ resilience to shocks. The recently introduced minimum amortization requirement applies to mortgages issued after June 2016, until LTV ratios reach 50 percent. The minimum annual amortization is 2 percent for LTV ratios above 70 percent, and 1 percent for LTV ratios between 50 and 70 percent.

The authorities also introduced a Liquidity Coverage Ratio (LCR) requirement11 to reinforce the banks’ resilience to shocks in FX funding. The requirement of 100 percent, introduced in January 2013, applies separately to EUR and USD as well as to all currencies and ensures that the banks have enough liquid FX assets to withstand FX liquidity stress in the short term. The decision to also introduce separate currency requirements was justified by Swedish banks’ extensive dependence on market funding in foreign currency, which makes them particularly sensitive to liquidity shocks in these currencies. In addition, as the Riksbank’s ability to provide liquidity assistance in foreign currency is limited, the authorities argued that it is important that the banks themselves ensure that they have FX buffers to deal with liquidity disruptions in the main foreign currencies.

Macroprudential measures appear to have helped contain vulnerabilities, and may have slowed housing prices and lending, but it is not yet clear how lasting the latter impacts will be. Average LTV ratios on new mortgages have declined from 71 percent in 2010 to 69 percent in 2016, and credit growth to households has remained at a single digit pace since 2010, even as house prices gains accelerated to around 15 percent in 2014-15. The announcement of the mortgage amortization requirement in late 2015 was followed by a period of significantly slower housing price increases, especially in apartments, which was reflected in slower credit growth with a lag. But following the actual implementation of the measure, prices appears to rebound somewhat in the second half of 2016. Nonetheless, housing price increases remain well below the pace seen in 2014-15. For new mortgages, average amortization has risen to 4.6 percent of income in 2016, from 3.3 percent in 2015. Further analysis of the impact of the amortization requirements by the Swedish supervisor finds it has resulted in households buying less expensive homes and borrowing less, which suggests the potential for a more lasting effect on the level of housing demand and household debt. The share of households taking on high debt burdens (exceeding 600 percent of gross disposable income) had risen from 10 percent in 2011 to 17 percent 2015, but edged back to 16.4 percent in 2016.

The Article IV consultations in 2015 and 2016 recommended additional measures to address the risks associated with rising housing prices and housing indebtedness. The consultations emphasized the need for deep reforms of Sweden’s poorly functioning housing market, including to (i) sustain the increase in housing supply; (ii) tax reforms to reduce housing demand and incentives for debt financing, and; (iii) phasing out rent controls which leave many household with no option other than to purchase. It also recommended that a limit on the share of high debt-to-income (DTI) loans be adopted soon to contain increases in the interest sensitivity of consumption and protect household resilience to incomes losses, to automatically reduce LTVs on high DTI loans when housing prices rise faster than income, and to make lending responses to housing price increases less elastic, dampening potential for an upward credit-price spiral.”

On Sweden, the new IMF report says that:

“The robust economy and low interest rates, together solid population growth and inelastic housing supply, boosted housing prices and hence household debt:

- As a percentage of disposable income, household indebtedness has almost doubled since 1996 and now stands at about 180 percent, with a growing share of new borrowers taking on high debts relative to income. The growth in debt has primarily reflected rising housing prices owing to prolonged supply demand imbalances exacerbated by low amortization,

Posted by at 4:41 PM

Labels: Global Housing Watch

Friday, September 8, 2017

Housing View – September 8, 2017

On cross-country:

- Global developments in residential property prices – BIS

- Global House Price Index – Knight Frank

- European Mortgage Markets Quarterly Review (Q42016) – EMF

- The Valuation of Property for Lending Purposes – EMF

- Winner Take All? Richard Florida’s ‘New Urban Crisis’ Part of Growing Global Focus on Unequal Cities – World Resources Institute

- Pricey housing markets mean co-living buildings are on the rise – Economist

On the US:

- Why Can’t We Get Cities Right? – New York Times

- How Local Housing Regulations Smother the U.S. Economy – New York Times

- Home Purchases and Household Spending – NBER

- Is Home Sharing Driving Up Rents? Evidence from Airbnb in Boston – Journal of Housing Economics

- Rebuilding Housing in Harvey’s Aftermath: Two Lessons from Hurricanes Katrina and Rita – Harvard Joint Center for Housing Studies

- Uncertainty in the housing market: Evidence from the US states – University of Macedonia

- 8 Big Housing Changes Thanks to Driverless Cars – John Burns Real Estate Consulting

- Real Estate Lending Risks Monitor – Federal Reserve Bank of San Francisco

On other countries:

- [Canada] Why Bother With Stocks in Vancouver’s Relentless Housing Market? – Bloomberg

- [Canada] Vancouver’s housing crisis – RICS Land Journal

- [Canada] Trends in household mobility and housing choices – CMHC

- [China] China’s property market is a major source of financial risk: central bank official – Reuters

- [Ethiopia] Ethiopia is struggling to make housing affordable – Economist

- [Italy] Is social polarization related to urban density? Evidence from the Italian housing market – Landscape and Urban Planning

- [Netherlands] Can Netherlands’ ground-shifting plan prevent flooding? – Financial Times

- [Norway] Irrationality in the housing market? An empirical analysis of the capitalisation of local property taxes in the Norwegian housing market – University of Oslo

- [Spain] The cycle of wage inequality in Spain: The impact of the boom and bust in the housing market – VOX

- [Spain] Se consolida la tendencia positiva del inmobiliario en el 1S17 – BBVA

- [United Arab Emirates] The UAE Property Report 2017 – Cluttons

On cross-country:

- Global developments in residential property prices – BIS

- Global House Price Index – Knight Frank

- European Mortgage Markets Quarterly Review (Q42016) – EMF

- The Valuation of Property for Lending Purposes – EMF

- Winner Take All? Richard Florida’s ‘New Urban Crisis’ Part of Growing Global Focus on Unequal Cities – World Resources Institute

- Pricey housing markets mean co-living buildings are on the rise – Economist

On the US:

- Why Can’t We Get Cities Right?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, September 1, 2017

Housing View – September 1, 2017

On cross-country:

- Workshop: Housing and Household Finance – Norges Bank

On the US:

- Perspective and Trends in the US Housing Market – Unassuming Economist

- Credit Growth and the Financial Crisis: A New Narrative – NBER, Quartz

- The Housing Industry Still Hasn’t Realized It’s Building Too Many Homes for Rich People – Slate

- Mortgage Interest Deduction Reform On the Table – Cato Institute

- S. house prices to keep rising on supply constraints: Reuters poll – Reuters

On other countries:

- [Canada] Advice for Toronto’s next chief planner—give Torontonians housing options – Fraser Institute

- [China] China to boost rental housing supply by building on rural land – Reuters

- [New Zealand] Housing Affordability Fires Up New Zealand’s Voters – Bloomberg

On cross-country:

- Workshop: Housing and Household Finance – Norges Bank

On the US:

- Perspective and Trends in the US Housing Market – Unassuming Economist

- Credit Growth and the Financial Crisis: A New Narrative – NBER, Quartz

- The Housing Industry Still Hasn’t Realized It’s Building Too Many Homes for Rich People – Slate

- Mortgage Interest Deduction Reform On the Table – Cato Institute

- S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, August 30, 2017

Perspective and Trends in the US Housing Market

Where will the 30-year fixed mortgage rate be next year? How will this affect the housing market? What has happened to mortgage rates in previous episodes of hikes of monetary policy rate? Is the low for sale inventory a new normal? These are some of the questions that Frank Nothaft tackles in this interview. Nothaft is a Senior Vice President and Chief Economist at CoreLogic.

Hites Ahir: CoreLogic recently hosted RiskSummit 2017 in California. What is the idea behind this annual event, and can you tell us about the audience at this event?

Frank Nothaft: CoreLogic’s RiskSummit is a housing conference for our clients. Now in its 29th consecutive year, RiskSummit brings together hundreds of domestic and international executives from mortgage banking, capital markets, home insurance carriers, regulatory agencies, government-sponsored enterprises, multifamily and rental property management companies, and real estate information providers.

Hites Ahir: At the event, you made a presentation on the US housing market. The first thing you did was to take a poll from the audience on where will the 30-year fixed mortgage rate be by the next RiskSummit 2018. What did you find?

Frank Nothaft: There was consensus that mortgage rates will be higher a year from now, but with a wide dispersion in views. It reminded me of the latest projection material from the Federal Open Market Committee (FOMC) members, who expect the target for the federal funds rate to be higher by the end of 2018 but with wide disagreement on how much higher the target will be; FOMC members’ views varied from no change in today’s target to a 200-basis point increase! (see FOMC Projection Materials June 2017).

Hites Ahir: What is your view?

Frank Nothaft: My view is in line with the consensus projection: Namely, that mortgage rates will be higher a year from now. Today, 30-year fixed-rate mortgages are up about 50 basis points from a year ago, and it is likely that mortgage rates will be up an additional 50 basis points a year from now. Even if that increase should come to pass, raising 30-year mortgage rates to about 4.5 percent, these rates will still be remarkably low compared to where they have been historically.

Hites Ahir: How will this affect the housing market?

Frank Nothaft: There are several effects on both the housing and the mortgage markets. The most salient effects in the housing market are a decline in affordability, and a slowing of homeowner mobility. The latter point is sometimes referred to as the ‘lock-in’ effect: Homeowners with a mortgage rate that is significantly lower than current interest rates may be less willing to ‘trade homes’ and take on higher financing costs. When we compare the re-sale frequency when mortgage rates had risen by, say, 1½ percentage points compared with their level as of the original purchase, we found that the mobility rate was lower. This suggests that the for-sale inventory may continue to remain lean for the foreseeable future, adding upward pressure to home-price growth.

Higher interest rates also have significant effects on the mortgage market. For one, refinance originations generally fall sharply. The median mortgage rate is about 3.75 percent today, and as market interest rates rise the amount of mortgage debt that remains ‘in-the-money’ to refinance shrinks. Thus, the drop-in refinance originations implies that overall lending volumes will likely be somewhat less in the coming year. On the other hand, annual originations will likely be less volatile in an environment of higher interest rates, as purchase-money lending has less year-to-year variation than refinance.

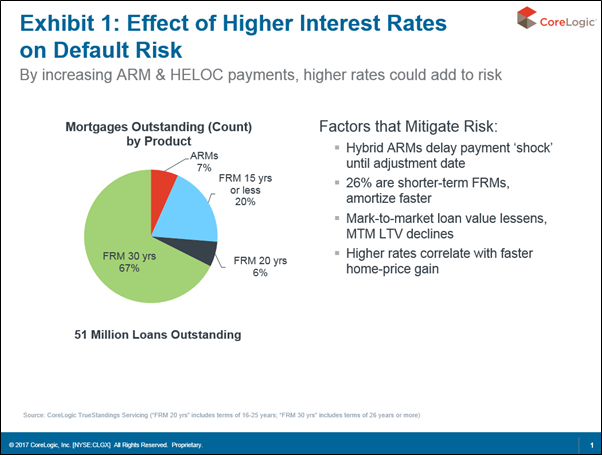

Another issue for mortgage markets is whether higher market rates affects credit risk. While credit risk for adjustable-rate mortgages (ARMs) and home-equity lines-of-credit (HELOCs) may increase (because of the potential for ‘payment shock’ when the payment adjusts), there are several mitigating forces which suggest that overall credit risk on loans outstanding will be minimal: first, ARMs are only 7 percent of the mortgage loans outstanding; second, shorter-term mortgages are 26 percent of loans outstanding and amortize quickly; third, mark-to-market loan-to-value on fixed-rate loans will decline as interest rates rise; and fourth, nominal home-price growth is generally correlated with the level of interest rates and will lower current loan-to-values. (Exhibit 1)

Hites Ahir: What has happened to mortgage rates in previous episodes of hikes of monetary policy rate?

Frank Nothaft: The Federal Reserve has direct control over the discount rate and the federal funds rate, and substantial influence over other short-term interest rates. But its effect lessens as one moves to longer-term maturities across the yield curve. Long-term yields, such as on 10-year Treasuries or 30-year mortgages, will also be affected by investors’ inflation expectations. If the capital market thinks that higher short-term rates reduces inflationary pressures, then long-term rates may show little change or even decline. Conversely, if the market believes the Federal Reserve is increasing short-term rates too slowly, then the entire yield curve could shift up. In other words, sometimes mortgage rates have moved higher, sometimes lower. I believe that mortgage rates are likely to move higher over the coming year because the Federal Reserve has also indicated that it plans to reduce the size of its mortgage-backed security and Treasury bond portfolio over time.

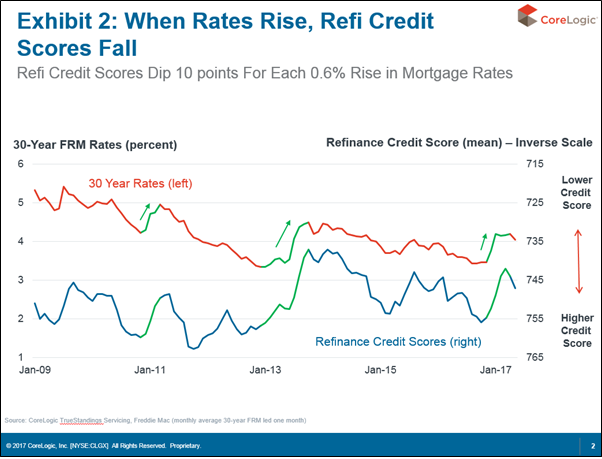

Hites Ahir: “When Rates Rise, Refi Credit Scores Fall”—this is one of slides of your presentation. What happens when you look at period before and after the Great Recession?

Frank Nothaft: In general, when mortgage rates have risen, we observe the credit scores of refinance borrowers decline. (Exhibit 2) This could reflect an increase in ‘cash-out’ refinance, or an increase in FHA-to-Conventional refinance as a share of refinance. The latter is particularly important because the FHA, since January 2013, has not allowed termination of the mortgage insurance premium payment. The only way for a borrower to ‘cancel’ the mortgage insurance premium is to refinance into a conventional loan with a loan-to-value of 80 percent or less. This type of refinance has picked up and may account for 200,000 refinances in 2017. Thus, one reason credit scores for refinance borrowers dip when interest rates rise is that FHA borrowers typically have a lower credit score that conventional borrowers, so as FHA borrowers refinance into conventional, the average credit score of all refinance borrowers dips.

Hites Ahir: You also point out that there is a low for sale inventory. Is this a new normal?

Frank Nothaft: Yes, I think it is a ‘new normal’. We measured the for-sale inventory relative to the housing stock and found that the inventory was the lowest it has been in at least three-and-a-half decades. And if higher mortgage rates reduce homeowner mobility, and thus reduces the number of existing homes offered for sale, then the low for-sale inventory levels will continue.

Where will the 30-year fixed mortgage rate be next year? How will this affect the housing market? What has happened to mortgage rates in previous episodes of hikes of monetary policy rate? Is the low for sale inventory a new normal? These are some of the questions that Frank Nothaft tackles in this interview. Nothaft is a Senior Vice President and Chief Economist at CoreLogic.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, August 25, 2017

Housing View – August 25, 2017

On cross-country:

- Dealing with the effects of one bubble creating more – Financial Times

- Real Estate Summary – Edition 2, 2017 – UBS

On the US:

- The Housing Boom and Bust: Model Meets Evidence – NBER

- Oil Change: Fueling Housing and Land Prices? – Real Estate Center at Texas A&M University

- Why Housing Has Outperformed Equities Over the Long Run – Policy Tensor

- The Appropriate Government Role in U.S. Mortgage Markets – Federal Reserve Bank of New York

- Mortgage Lenders Shift Focus to Enhancing the Consumer Experience – FannieMae

On other countries:

- [Canada] Foreign Buyers and Home-Price Growth: 15% nonresident foreign buyer tax enacted in Toronto and Vancouver – CoreLogic

- [Canada] Interest Rates and Mortgage Borrowing Power in Canada – Fraser Institute

- [China] Beijing plans to extend homeowners’ right to schools to tenants – Financial Times

- [Colombia] Housing Finance and Real Estate Markets in Colombia – IMF

- [Germany] Germany’s Housing Market Is Red Hot, But Don’t Call It a Bubble – Bloomberg

- [Israel] Spatial Planning and Policy in Israel: The Cases of Netanya and Umm al-Fahm – OECD

- [Ireland] An analysis of recent trends in the Irish rental market 2017 Q2 – Daft.ie

- [Turkey] Housing price dynamics and bubble risk: the case of Turkey – Journal of Housing Studies

- [United Arab Emirates] Dubai Supply: Myth Busters – REIDIN

- [United Kingdom] Major land reform urged to fix UK housing crisis – Financial Times

On cross-country:

- Dealing with the effects of one bubble creating more – Financial Times

- Real Estate Summary – Edition 2, 2017 – UBS

On the US:

- The Housing Boom and Bust: Model Meets Evidence – NBER

- Oil Change: Fueling Housing and Land Prices? – Real Estate Center at Texas A&M University

- Why Housing Has Outperformed Equities Over the Long Run – Policy Tensor

- The Appropriate Government Role in U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts