Showing posts with label Global Housing Watch. Show all posts

Friday, September 21, 2018

Housing View – September 21, 2018

On cross-country:

- Q2 2018: Global house price boom – strong house price rises continue in Europe and parts of Asia – Global Property Guide

- Eurozone housing market cycle is maturing – ING

- Disillusion mounts in Europe’s housing market – ING

On the US:

- Price-to-Income Ratios are Nearing Historic Highs – Harvard Joint Center for Housing Studies

- Why do so many affordable-housing advocates reject the law of supply and demand? – Washington Post

- The Mortgage Market Is Back a Decade After the Credit Crisis—With New Risks – Bloomberg

- Jeff Bezos Homeless Pledge Follows Amazon Fight Against Housing Tax – Bloomberg

- Census: Renters’ Incomes Still Lagging Behind Housing Costs – Center on Budget and Policy Priorities

- New evidence shows manufactured homes appreciate as well as site-built homes – Urban Institute

- ‘As safe as houses’: How a small corner of the US mortgage market nearly brought down the global financial system – Bank of England

- Does Rising Housing Inventory Signal the Beginning of a Buyer’s Market? – First American

- The Wealth Hiding in Your Neighborhood – Institute for Policy Studies

- Luxury Real Estate Boom Adds to Risk of Climate Disruption – Institute for Policy Studies

- Tough Times Ahead for Housing – Wall Street Journal

On other countries:

- [Brazil] Brazil’s house prices still falling, but outlook positive – Global Property Guide

- [China] China’s Weakest Housing Markets Flash Red in Cautionary Tale – Bloomberg

- [China] One of China’s Wildest Housing Markets Is Broken – Bloomberg

- [China] How China’s plan to develop rental housing backfired – Reuters

- [Chile] Chile’s house prices continue to rise modestly, despite the imposition of 19% VAT on property sales – Global Property Guide

- [Ireland] Ireland sets up land agency as anger grows at housing shortage – Reuters

- [Ireland] Dublin’s Housing Crisis Reaches a Boiling Point – CityLab

- [Malta] Malta house price growth outstrips Hong Kong to take top ranking – Financial Times

- [New Zealand] New Zealand’s house prices are rising again – Global Property Guide

- [South Korea] Korea imposes tougher taxes on properties to curb price surge – Reuters

- [Ukraine] Ukraine’s house price falls accelerating – Global Property Guide

- [United Kingdom] Is UK property still a good investment? – Financial Times

- [United Kingdom] K. House Prices at Risk From Brexit – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- Q2 2018: Global house price boom – strong house price rises continue in Europe and parts of Asia – Global Property Guide

- Eurozone housing market cycle is maturing – ING

- Disillusion mounts in Europe’s housing market – ING

On the US:

- Price-to-Income Ratios are Nearing Historic Highs – Harvard Joint Center for Housing Studies

- Why do so many affordable-housing advocates reject the law of supply and demand?

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, September 18, 2018

House Prices and Labor Mobility in Norway: A Regional Perspective

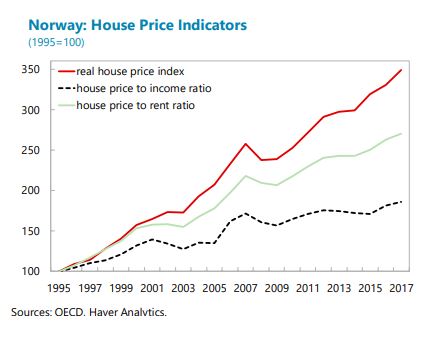

From the IMF’s latest report on Norway:

“House prices in Norway have been growing rapidly in recent years. As of May 2018, nationwide house prices were 55 percent higher than in 2010. The national house price to income ratio remains historically and internationally high. Although house prices fell in 20172— particularly in Oslo, which saw nominal house price declines of 10.5 percent—the correction was short lived. House prices rose again by 7.5 percent during January to May of 2018 on a seasonally-adjusted basis.

There has been a significant regional divergence of house price trends since 2013. Real house prices in Oslo now stand 60 above their 2010 level—compared to 35 percent for the whole of Norway. House prices in Oslo have been increasing particularly quickly compared to other regions since 2013. This represents a contrast to the last period of rapid house price appreciation—before the global financial crisis—when house prices grew evenly across Norway.

Large differences in house prices across regions can have macroeconomic implications. There is growing evidence that large house price differentials can limit regional labor mobility, thus slowing income and productivity convergence (Ganong and Shoag, 2015; Hsieh and Moretti, 2017). House price differentials—to the extent they translate into higher household debt and debt servicing costs—can make some local economies more sensitive to abrupt house price corrections than the others, thus providing arguments in favor of region-specific rather than nation-wide policies to mitigate financial vulnerabilities.

In this analysis we estimate the extent to which the recent regional house price divergence in Norway can be explained by fundamental factors. Section B looks at the recent trends in regional house prices, demand and supply factors more in detail. Section C describes our econometric approach to estimating regional equilibrium house prices, and provides main findings on the extent of house price over- or under-valuation across Norwegian regions. Section D studies the impact of house price differentials on labor mobility in Norway. Section E concludes.”

From the IMF’s latest report on Norway:

“House prices in Norway have been growing rapidly in recent years. As of May 2018, nationwide house prices were 55 percent higher than in 2010. The national house price to income ratio remains historically and internationally high. Although house prices fell in 20172— particularly in Oslo, which saw nominal house price declines of 10.5 percent—the correction was short lived. House prices rose again by 7.5 percent during January to May of 2018 on a seasonally-adjusted basis.

Posted by at 4:35 PM

Labels: Global Housing Watch

Monday, September 17, 2018

Affordable Housing: Views from Albert Saiz

Global Housing Watch Newsletter: September 2018

In this interview, Albert Saiz talks about the current housing affordability problems in the US, the reasons behind it, the tools to tackle affordability issues, what the future holds, and more. Saiz is the Daniel Rose Associate Professor of Urban Economics and Real Estate at the Massachusetts Institute of Technology (MIT). He also serves as the Director of MIT’s Urban Economics Lab.

On the current situation…

Hites Ahir: As you know, affordable housing has been dominating the headlines. To start, could you define affordable housing?

Albert Saiz: Affordable housing means the provision of a living space that is accessible and of good quality, and that is commensurate to the social and local economic conditions. It also means that the cost of housing should not put an excessive burden on a family’s consumption of other life essentials—such as food, water, electricity, heating, clothing, etc.

Hites Ahir: So why has affordable housing become a hot topic?

Albert Saiz: I think there are five reasons for this. First, income inequality is rising. House prices are rising, but the earnings of low and middle-income families are not rising at the same pace.

Second, construction costs are rising at a faster pace relative to other manufactured consumer goods. So, we have rising construction costs combined with almost flat growth in income. For low and middle-income families, this means rising housing expenditure shares.

Third, there are constraints on land available for real estate development. Some of the most popular cities in the US—which have better amenities—happen to be severely constrained in the land available for real estate development. Several of them are in coastal or mountainous regions, which limits their potential for geographic expansion. And in most of them, NIMBY [Not in My Backyard] and anti-growth municipal policies make it very difficult to build new housing at high densities. So, there are less houses for sale in the market at a price affordable to low and middle-income families.

Fourth, central cities have again become attractive. In the past, large central cities had become less desirable for the middle class due to suburbanization. This implied that they had become affordable for low-income families. However, this trend has stopped and—in many metropolitan areas, it has reversed. Better amenities combined with other features have made the denser parts of metro areas more attractive to upper-middle class citizens again. The ensuing process of gentrification is making these neighborhoods less affordable.

Fifth, there are multiple objectives between the key players in the sector. For example, affordable housing developers and policymakers sometimes have multiple objectives that are not always easy to reconcile.

Hites Ahir: You have defined affordable housing and explained why it has become a hot topic. Can you now explain why housing affordability matters?

Albert Saiz: Access to good housing, food, and clothing are three essentials of mankind. So, from a humanistic perspective, housing is an absolute priority for policymakers. Also, we have seen, problems related to housing affordability have become an important political issue in many cities in the US. Mayors are feeling the electoral pressure from their constituents to do something to mitigate rising cost of housing. However, state and the federal governments that cater to constituents outside of high housing cost areas, may feel less political pressure or ideological commitment to affordable housing. And yet, ensuring access to housing is necessary for social stability. It is in the best interest for all that the less well-off members of our communities’ lead fulfilling and productive lives. Housing, health, and education are fantastic investments that yield peaceful and cohesive societies.

On the ways to tackle affordable housing…

Hites Ahir: Could you now tell us about the main tools to tackle affordable housing? And have they worked?

Albert Saiz: Rent control, public housing, Section 8 vouchers, Low-Income Housing Tax Credit Program, and Community Development Corporations and land trusts are the main tools that have been used to tackle affordable housing.

Rent control regulations have demonstrated their shortcomings in curtailing incentives to rental supply. They are being abandoned throughout the country.

Public housing has been relatively expensive to build and manage. Throughout the US, large and isolated housing projects have been widely perceived as reservoirs for social maladies. Providing good public housing is possible. However, the fact that delivering high-quality housing services in their thousands represents a political risk for Mayors makes it unlikely that this option will experience substantial growth in the short run.

Section 8 program vouchers provide thousands of Americans with a check-like payment that can be used toward rental housing. The Section 8 program is effective but increasing the allocation funds for social policy at the federal level will continue to be challenging.

Under Low-Income Housing Tax Credit Program, developers raise funds to build and lease affordable rental units by selling federal tax credits to investors. Criticisms have been raised about how effectively the program has increased supply. Some of the subsidies may accrue to developers who would have built the units anyway. The Low-Income Housing Tax Credit Program has also been criticized for disproportionately siting affordable housing buildings in low-income neighborhoods that provide poor access to jobs and social opportunities.

Community Development Corporations and land trusts constitute a bottom-up effort from organized citizens to redevelop underused sites and produce housing and business in less-privileged areas. In many US cities, they typically channel a limited amount of public resources—subsidies, land, construction of infrastructure, or zoning allowances—in exchange for the provision of affordable housing in their communities. Given the current lack of political consensus for social housing policy at the federal level, this model is likely to grow.

On what the future holds?

Hites Ahir: Let’s talk a bit about the future. “Real Trends: The Future of Real Estate in the United States”—is a report that you recently put together with Arianna Salazar of the Massachusetts Institute of Technology. In a nutshell, what is the main message from this report?

Albert Saiz: This is a report about the major demographic, economic, social, and technological trends that will have an impact on the US real estate market in the decades to come. So, it is difficult to reduce it to a single message. However, if you insist, I can summarize two main conclusions. First, the current demographic change is having major consequences for the housing market. Second, with a bit of a lag, computers are now starting to change the nature of the real estate industry.

Hites Ahir: From the report, what is the good news for affordable housing?

Albert Saiz: There are some good news for affordable housing. Let me mention three areas. First, from the construction and design point of view, innovative technologies will have the potential to help produce and distribute quality housing in cheaper ways. For example, the diffusion of affordable housing innovations and policies is increasing. Drawings and designs of low-cost housing typologies can be found online for free.

Second, from the policy point of view, the awareness that supply-side policies are important has grown in recent years. This will lead to more consensus and efforts to fight NIMBY. For example, there is a very promising trend of re-using and adapting post-industrial spaces in cities for affordable housing.

Third, from the industry point of view, the re-emergence of more socially-oriented entrepreneurs and housing non-profits may spur innovation in the affordable housing arena. For example, the development of contract typologies that have hitherto been less used—such as rent-to-own; mortgages with lower rates where the lender shares in housing appreciation; space sharing and co-living arrangements; rentals of accessory units—may help more families access affordable housing. And socially-oriented crowdfunding platforms may help tap funds for affordable-housing construction.

Hites Ahir: And the bad news is?

Albert Saiz: The major underlying trends that generate the current affordability problems are likely to continue. For example, income inequality will continue growing, and redistributive policies is not likely to experience a major revival any time soon. And it will take a while for NIMBY pressures to abate in large coastal cities.

Hites Ahir: Is there an example of a country that has done better in tackling affordable housing?

Albert Saiz: Let me tell you about the case of the Netherlands. In the Netherlands, 75 percent of that nation’s 3 million rental units are provided by nonprofit housing associations. These associations purchase and develop apartments for rent. They compete with investors in the open real estate market. They also compete to provide high-quality services to their customers. These organizations are extremely agile, having to make investment and management decisions to survive in a competitive environment. Because they own the properties they rent, these organizations can deploy intelligent asset disposition and purchase strategies. They can, therefore, plow the gains from capital appreciation of their portfolio back into their social mission. So, I think the role of non-profit, non-governmental organizations could increase in the US.

Hites Ahir: For the past three years, you have been organizing the World Real Estate Forum. It is one of the top real estate conference held during the year. What messages are coming out on affordable housing from the entrepreneurs and CEOs that attend this conference?

Albert Saiz: I would say they are concerned about the housing affordability trends that we have discussed. Yet, my sense is that there will be a more proactive role from the industry in helping us with the housing affordability challenge in the future. We are already also seeing the reemergence of a new breed of humanistic, socially-conscious real estate entrepreneur—and associated investment vehicles—interested in creating more inclusive, and better communities. Some examples include Magic Johnson—his fund invested in more than 20 American cities, Dan Gilbert in Detroit, Jonathan Rose in greater New York Metro, Bobby Turner in Los Angeles, Patrick Kennedy in San Francisco, David Zucker in Denver, and thousands more throughout the US.

From a panel at the World Real Estate Forum

On the impact of technology…

Hites Ahir: Let’s talk a bit about the link between technology and affordable housing. What impact will the adoption of autonomous vehicles have on affordable housing?

Albert Saiz: According to most economic theories, the impact of reductions in the cost of transportation should have a positive impact on housing affordability—whenever accompanied by good policies. In denser urban areas, autonomous vehicles can facilitate car-sharing, thereby allowing for higher residential densities and more housing supply. We are seeing this trend play out in Miami, due to a reduction in parking requirements. In suburban and exurban locations—where families will still own their own cars—land availability may increase as remote locations now become accessible. This latter trend may actually facilitate the expansion of the American edge city, and its combination of relatively affordable housing but externalized social costs. Therefore, the impact on urban form will be dual: it will help produce denser redevelopment at higher densities, but actually increase sprawl in areas with initial low density.

Hites Ahir: In several cities, there are concerns that rents are rising due to short holiday lets through websites and apps. What are your views on the impact of sharing services within the housing market?

Albert Saiz: As an economist, I tend to believe that innovations that arise to better satisfy human needs are good. I therefore tend to look at new technologies, and mutually-agreeable contracts—such as those afforded by space-sharing apps—as positive developments in general.

I am apprehensive that—in some places—space-sharing apps may be coming to represent an easy-targetable scapegoat for much larger problems. For instance, many of the most touristic areas in popular cities had been already gentrifying—or would have done so—regardless of AirBnB.

A number of very selected extremely-attractive cities around the world, are experiencing a genuine trend of people flocking in for their amenities. This trend expresses itself via a number of highly-related phenomena: well-off professionals moving in from other areas; gentrification; proliferation of second residences; more out-of-town real estate investors; a surge in the number of tourists; more visitors in meetings and conferences; growth in the number of short or long-term students; retirees or freelancers—not tied to the local labor markets—moving in; and a higher incidence of short-term space sharing. Note that all of these are symptoms of the same implicit trend—increased demand for the city interacting with relatively fixed supply—rather than the maladies themselves. In fact, some of the cities that are taking action against AirBnB and similar platforms also happen to be cities that have acted aggressively against new real estate development, thereby making the problem worse.

Nevertheless, I do believe that there is a need for some regulation. For example, short-term rental apartments or rooms in which noise or disturbances keep happening repeatedly should be shut down. Individuals managing three or more shared-economy full-time rentals should be subject to the same business regulations, and tax regimes that apply to hotels or regular Bed-and-Breakfasts. Cash-flows from shared-economy operations should be taxed at the appropriate rate—perhaps with minimum exemptions—and underreported income should be severely punished.

Hites Ahir: What has been the impact of transactional websites or listing data aggregates websites?

Albert Saiz: The information revolution brought by the internet has allowed buyers and sellers of real estate to acquire information about millions of properties. Websites such as Realtor.com or Zillow.com aggregate information from regional Multiple Listing Services, facilitating access to information about each property in all markets. The most prodigious aspects of this “transactions revolution” in residential properties have been its speed and ubiquity. Searching for vast numbers of properties on the internet has become the norm.

The future will bring further integration of existing and new databases into the search records and statistical analysis of market information in real time. For instance, prospective buyers may be able to see 3D renderings of a home’s interior and, given the history of recorded clicks, obtain forecasts of the probability of an offer being made on a property in the next three days.

Hites Ahir: I am sorry to have bombarded with a lot of questions. I have one more. As you know, we are in a period of accelerated technological change. Is there a specific technology/innovation that will be in high demand?

Albert Saiz: There are so many of them. I invite your readers to go through our report for an in-depth exposition. However, demographic trends are crystal clear. We will require ways to house our elderly by retrofitting existing homes and urban spaces. We will also need to provide assisted living facilities for those with reduced mobility. The demand for inpatient and outpatient health facilities will not wane anytime soon. Necessity is the mother of invention, so all of these needs will require of new technologies and design applied to the provision of housing and residential services to the growing elderly population.

Global Housing Watch Newsletter: September 2018

In this interview, Albert Saiz talks about the current housing affordability problems in the US, the reasons behind it, the tools to tackle affordability issues, what the future holds, and more. Saiz is the Daniel Rose Associate Professor of Urban Economics and Real Estate at the Massachusetts Institute of Technology (MIT). He also serves as the Director of MIT’s Urban Economics Lab.

Posted by at 5:02 AM

Labels: Global Housing Watch

Urban Revitalization: The View from the Trenches

Global Housing Watch Newsletter: September 2018

Why social responsibility matters for urban revitalization? How does a developer provide city center affordable housing? How can a developer involve the community in a urban revitalization process? What challenges do developers face? These are some of the questions that Keyes Christopher “KC” Hardin tackles in this interview. KC is the co-founder and CEO of Conservatorio SA—a real estate development company based in Panama City, Panama. He is also a Fellow of the Aspen Institute’s Central American Leadership Initiative, and a Research Associate at MITs Community Innovators Laboratory.

The company…

Hites Ahir: What is Conservatorio SA and what does it do?

KC Hardin: Conservatorio SA is a real estate development company dedicated to sustainable urban revitalization. We started Conservatorio SA fourteen years ago to fix up a couple of historic buildings in Panama City’s UNESCO Heritage site, and it’s grown into a company that builds just about every category of product you can find in a downtown—hotels, condos, offices, multi-family, even cultural infrastructure like theatres.

We call our brand of real estate “sustainable urban revitalization” which is basically mixed-use, mixed-income urban core redevelopment with a heavy social inclusion component. Within all those categories we also build just about every level. We have hotels that are $17 US dollars per night and hotels that are over $300 US dollars. We build apartments that sell for $80,000 US dollars and others for $2 million US dollars. All within a few blocks of each other. We tend to hold on to commercial property for the long-term but we like to sell apartments because it allows us to recycle capital and we think that neighborhoods work better when people have a chance to own their own homes.

Hites Ahir: Why social responsibility matters to Conservatorio SA?

KC Hardin: On a personal level, I grew up in Miami until the 1990s and then in New York until 2003. For whatever reason I was always in neighborhoods that were either revitalizing or deteriorating. So, I had a sense for the good and the bad of an urban revitalization cycle. I saw how much better cities worked when their cores became vibrant and safe, but I also came to understand that there was a question of “better for whom?” So Conservatorio SA was founded on the question of whether it is possible to have the good of urban revitalization while minimizing its two big negative externalities: displacement and cultural homogenization.

That question has taken us down a long road of learning how to balance our responsibility to capital with our responsibility to community. Along the way we’ve picked up what I think is a pretty deep understanding of the mechanisms of social and economic exclusion, the long-term value of authenticity and how to co-create with communities.

The historic district of Panama City…

Hites Ahir: How has Casco Viejo and the surrounding area evolved over the years?

KC Hardin: The Spanish laid out Casco Viejo’s fantastic street grid in the 1500s, and it has been transforming ever since, through numerous booms and busts. As Panama most recently boomed in the 2000s, Casco Viejo lagged the rest of the city. I think this is because very few investors understood how revitalization works back then. When we started Conservatorio SA in 2004 more than 80 percent of the building inventory was unrestored, there were four gangs that controlled the district, and raw sewage leaked onto the streets, just to name a few issues. But there were preservationists who fought hard to protect the area, and pioneers who started reigniting it culturally. It is now able to support a very high quality of life, and is a point of pride for the country.

Hites Ahir: What has happened to house prices?

KC Hardin: Housing prices have risen from being about 30 percent lower than the best parts of the city in 2007 to being about 30 percent higher now. I think that premium is due to limited supply, higher construction costs, and a unique lifestyle that doesn’t exist in other parts of the city. On the rental side, the change has been even more dramatic because it has gone from a neighborhood where most people lived in condemned buildings paying little or no rent to one of the city’s most expensive. So, in terms of relevance to the city and pricing, the neighborhood has gone full cycle from its last peak in the 1950s.

But that revitalization has come at a human cost because much of the population that moved in during the decline was not given a real opportunity to stay. There was a direct tension between public policies designed to restore heritage and create economic growth on one side, and the social need of preventing widespread displacement on the other. There were well-intentioned but isolated efforts to balance these tensions but going forward we need better public policy and a deeper understanding of the long-term value of authenticity in the private sector.

Hites Ahir: How do you go about providing affordable housing in the area?

KC Hardin: Conservatorio SA has an internal policy of building one affordable housing unit for every high-end unit. We keep them affordable by keeping them compact, making parking optional, and sharing social areas and other amenities among several adjacent buildings. In many buildings, we mix market rate with affordable, so there are often a few units where the price is subsidized by those market rate units. There is also a government subsidy on interest rates for apartments that are under $120,000 US dollars, which helps keep the monthly payment affordable. For example, the monthly payment on a two bedroom can be as low as $380 US dollars, meaning that it is affordable for a minimum wage couple. That still leaves out a lot of people in our community so we need the government to address this gap.

Building an inclusive neighborhood…

Hites Ahir: What are some of the social projects that you have implemented to help, and involve the community?

KC Hardin: Besides building affordable housing, our primary social mission is to nurture an eco-system of social and economic inclusion programs. We believe that homeownership is a critical determinate of social outcomes, but we have learned that in historically marginalized communities the opportunity to buy, or even to move into a formal rental, no matter how affordable, is a very high rung on the ladder for many people. So investment in human development is the other key to minimizing displacement.

We invest in programs that address a multitude of interrelated problems like violence, teenage pregnancy, education, and poverty. We have also learned that all of those problems are just symptoms of a dysfunctional system. To create any sustainable change, those programs have to be tied together with a larger process of community organization, and empowerment that will hopefully push the community back into balance over the long-term. To help that process, we worked with the Community Innovators Lab at MIT to create a leadership development program called LiderazCo, which is short for “Leaders who Co-Create Community”.

Hites Ahir: If you had to pick one social project that has had the most significant impact in the district, which one would it be?

KC Hardin: Resolving gang tensions was critical. We invested heavily in a program to integrate gang members into the broader community. The outcomes at the individual level varied widely, but I think it had the effect of not only reducing violence, but also changing perceptions in the public and private sector about what was possible. In Latin America there is a strong bias towards repressive policies towards gangs that is probably counter-productive in the long run, so one of the program’s goals was to build bridges between sectors that don’t normally connect.

Hites Ahir: In your drive to build inclusive city center housing, what are the top three challenges that you are facing?

KC Hardin: I see three big challenges for inclusive housing. First is antiquated zoning that requires expensive parking and generally encourages lower priced detached housing out on the periphery of the city. The rules are conceived around an ideal of city center apartments for middle-to-upper income nuclear families who have two cars and two incomes. That leaves out a lot of people and makes it hard to innovate with new housing models, though lately the city has been receptive to proposals.

The second problem is a strict bank financing criteria that generally filters out people who are self-employed and those who are in the informal economy.

The final challenge is the high degree of marginalization in our society. The lack of investment in human development has made it extremely difficult for a lot of people to break into the formal economy, especially here where the big job growth is in the service sector.

What is next?

Hites Ahir: What is next for Consevatorio SA?

KC Hardin: In terms of lines of business, we are rapidly pushing further into bottom-of-the-pyramid, urban core housing solutions. We feel that affordable, multi-family housing with imbedded social services can be a profitable, and a key step in the ladder to equity. We are also working with our academic partners on some interesting commercial models around formalizing informal commerce. Geographically, we are now in Honduras and want to create urban core-focused joint ventures with like-minded developers throughout Latin America.

Global Housing Watch Newsletter: September 2018

Why social responsibility matters for urban revitalization? How does a developer provide city center affordable housing? How can a developer involve the community in a urban revitalization process? What challenges do developers face? These are some of the questions that Keyes Christopher “KC” Hardin tackles in this interview. KC is the co-founder and CEO of Conservatorio SA—a real estate development company based in Panama City,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, September 14, 2018

Housing View – September 14, 2018

On cross-country:

- Affordable Housing Governance and Finance: Innovations, partnerships and comparative perspectives – Taylor & Francis Group

- Housing & Migration – A Research Briefing – Housing Europe Observatory

- Affordable housing in Europe: how do the various member-states do it? – Housing Europe Observatory

- “Investing in affordable housing comes with a high return both socially and financially” – Barcelona City Council

- Housing Europe supports the Municipalist Declaration of Local Governments for the Right to Housing and the Right to the City – Housing Europe Observatory

- Can Housing Be Affordable Without Being Efficient? – World Resources Institute

- These May Be the World’s 10 Riskiest Housing Markets – Bloomberg

On the US:

- Ben Carson and HUD Get Ready to Take On the Nimbys – Bloomberg

- Mapping the boom in nonbank mortgage lending—and understanding the risks – Brookings

- Is the housing price-rent ratio a leading indicator? – Federal Reserve Bank of St. Louis

- Americans are now better off renting than buying. Above all, avoid buying in Dallas! – Global Property Guide

- Rental Glut Sends Chill Through the Hottest U.S. Housing Markets – Bloomberg

- Mortgage Fraud Fueled the Financial Crisis—and Could Again – Institute of New Economic Thinking

- Voters Can Keep Housing Affordable – New York Times

- Book Review: High-Risers: Cabrini-Green and the Fate of American Public Housing – The New York Review of Books

- The Financial Crisis Changed Home Buying Forever – Wall Street Journal

- Preserving Affordable Rental Housing – MacArthur Foundation

- The Housing Bubble Burst All Over Reality TV – New York Times

- Maryland’s Biggest County Responds to Full Schools by Halting New Housing – Slate

- City NIMBYS – Furman Center for Real Estate and Urban Policy

On other countries:

- [Australia] Chinese real estate investment in Australia drops by nearly 30% – Macro Business

- [China] How Much Would China’s GDP Respond to a Slowdown in Housing Activity? – Federal Reserve Bank of Kansas City

- [Iceland] Iceland’s house prices continue to rise, albeit at a slower pace – Global Property Guide

- [Ireland] House prices in Ireland continue to rise at breakneck speed – Global Property Guide

- [Portugal] Portugal’s housing market remains robust – Global Property Guide

- [Portugal] Qué son las “visas doradas” y por qué causan polémica en Portugal – BBC

- [Romania] Romania’s house price growth decelerating sharply – Global Property Guide

- [Spain] The financial transmission of housing bubbles: Evidence from Spain – VoxEU

- [Spain] Te presentamos a tu casero: se llama Blackstone y es dueño de medio Madrid – GQ

- [Sweden] Sweden’s house price boom is officially over – Global Property Guide

- [Switzerland] Holes in Swiss property market ring mortgage alarm bells – Reuters

- [Thailand] Thailand’s house prices rising strongly again – Global Property Guide

- [United Kingdom] Housing affordability: Is new local supply the key? – Sage Journals

Photo by Aliis Sinisalu

On cross-country:

- Affordable Housing Governance and Finance: Innovations, partnerships and comparative perspectives – Taylor & Francis Group

- Housing & Migration – A Research Briefing – Housing Europe Observatory

- Affordable housing in Europe: how do the various member-states do it? – Housing Europe Observatory

- “Investing in affordable housing comes with a high return both socially and financially” – Barcelona City Council

- Housing Europe supports the Municipalist Declaration of Local Governments for the Right to Housing and the Right to the City – Housing Europe Observatory

- Can Housing Be Affordable Without Being Efficient?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts