Showing posts with label Global Housing Watch. Show all posts

Thursday, August 9, 2018

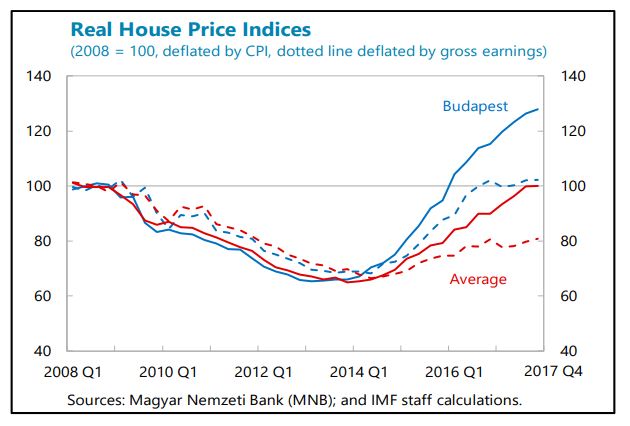

Housing Market in Hungary

From the IMF’s latest report on Hungary:

“Hungarian housing prices have increased rapidly since 2014, but from a low level. House prices began to increase in the Budapest area, but have spread to other cities and more recently to municipalities. According to the MNB’s and European Systemic Risk Board’s (data for the latter are as of Q3 2017) estimates, average prices are not yet excessively overpriced compared to fundamentals. The number of transactions has begun to stabilize, possibly due to labor shortages and increasing construction costs, which, according to market observers, frequently delay the completion of new dwellings by 6–12 months.

The housing boom has been driven by many factors other than credit. Delayed purchases following the global financial crisis as well as fiscal initiatives have contributed to the boom. For instance, (i) young families committed to have three or more children can receive a grant and a subsidized loan to purchase a home; and (ii) the VAT rate on sales of certain new dwellings has been temporarily reduced from 27 to 5 percent during the 2016–2019 period. Moreover, low interest rates have made real estate investments more attractive. The MNB’s mortgage bond purchase program may have further supported the market. Finally, the MNB-certified consumer friendly housing loans introduced in 2017, has helped level the playing field, lowered borrowing costs, and encouraged fixed-rate lending. The stock of loans for house purchases increased by 6.8 percent (y-o-y) in May 2018. Nevertheless, according to market observers, only about 45 percent of transactions involve borrowings. Moreover, household debt in Hungary remains low compared to peers. It is also almost completely denominated in local currency, but a substantial share remains variable-rate loans.

The MNB has preventatively tightened macroprudential policies, but the booming housing market needs to be closely monitored. The various macroprudential measures seem to be working, as only about 20 percent of new lending have variable-rates or a fixed rate up to one year. Already in 2016, the calculation of the payment-to-income (PTI) ratio was changed to not discourage fixed-rate borrowing. In April 2017, the mortgage funding adequacy ratio (MFAR) was introduced to encourage banks to issue longer mortgage bonds. These ratios will be further refined to discourage interest rate risk for households in October 2018, while there are no plans thus far to change the loan-to-value ratios. However, given the fact that the boom thus far has mostly been driven by strong disposable income and fiscal incentives rather than credit and low interest rates, there is also a need to review these fiscal incentives as well as supply constraints that appear to be contributing to the boom.”

From the IMF’s latest report on Hungary:

“Hungarian housing prices have increased rapidly since 2014, but from a low level. House prices began to increase in the Budapest area, but have spread to other cities and more recently to municipalities. According to the MNB’s and European Systemic Risk Board’s (data for the latter are as of Q3 2017) estimates, average prices are not yet excessively overpriced compared to fundamentals. The number of transactions has begun to stabilize,

Posted by at 10:08 AM

Labels: Global Housing Watch

Friday, August 3, 2018

Housing View – August 3, 2018

On cross-country:

- Housing, Debt and the Economy: a Tale of Two Countries – University of Oxford

- The End of the Global Housing Boom – Bloomberg

- Housing Costs and Regional Income Inequality in China and the U.S. – Federal Reserve Bank of St. Louis

- Charlemagne: the backlash against Airbnb – Economist

- ¿Es posible alquilar en la ciudad sin dejarse el sueldo en ello? – GQ

- Prime price growth drift lower across global cities – Knight Frank

On the US:

- The Scar From Which The Construction Workforce Has Yet To Recover – BuildZoom, Wall Street Journal

- Eyes Wide Shut? The Moral Hazard of Mortgage Insurers during the Housing Boom – NBER

- What is driving America’s housing crisis? A long-read Q&A with Lynn Fisher – American Enterprise Institute

- Fixing Public Housing: A Day Inside a $32 Billion Problem – New York Times

- Blackstone Makes First Bet on Manufactured Housing – Blackstone

- The Urbanist Case for Trailer Parks – CityLab

- The U.S. Housing Market Looks Headed for Its Worst Slowdown in Years – Bloomberg

- A Greater Share of Rentals Are Out of Reach for Blacks, Hispanics – Zillow

- Buying a Home Is Less Affordable Than It’s Been in Almost a Decade – Zillow

- Homeownership Aspirations: The Enduring & Evolving American Dream – Zillow

- Non-Resident Foreigners Sell for Twice Median U.S. Home Value – Zillow

- When Rent Growth Signals Stability, Not Stress – Zillow

- The Real Reasons Millennials Are Struggling to Become Homeowners – Zillow

- Housing’s Headwinds Are Getting Stiffer – Bloomberg

- Nation’s housing market may be headed for biggest slowdown in years – Seattle Times

- As Affordable Housing Crisis Grows, HUD Sits on the Sidelines – New York Times

- MLS Information Sharing Intensity and Housing Market Outcomes – The Journal of Real Estate Finance and Economics

- New York City Sues Airbnb to Force Compliance With Subpoena – Bloomberg

- Best Neighborhoods for Real Estate Buying and Investing – ATTOM

On other countries:

- [Australia] Australia House Prices Fall the Most in 7 Years – Bloomberg

- [Canada] Canada Risks Creating ‘A Permanent Generation Of Middle-Class Renters’: Industry Group – Huffington Post

- [China] China Toughens Housing Policy as Shenzhen Imposes More Curbs – Bloomberg

- [Poland] Disequilibrium in the real estate market: Evidence from Poland – Land Use Policy

Photo by Aliis Sinisalu

On cross-country:

- Housing, Debt and the Economy: a Tale of Two Countries – University of Oxford

- The End of the Global Housing Boom – Bloomberg

- Housing Costs and Regional Income Inequality in China and the U.S. – Federal Reserve Bank of St. Louis

- Charlemagne: the backlash against Airbnb – Economist

- ¿Es posible alquilar en la ciudad sin dejarse el sueldo en ello?

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, July 31, 2018

Housing Price, Credit, and Output Cycles: How Domestic and External Shocks Impact Lithuania’s Credit

A new IMF working paper by Iacovos Ioannou says that:

“Lithuania’s current credit cycle highlights the strong link between housing prices and credit. We explore this relationship in more detail by analyzing the main features of credit, housing price, and output cycles in Baltic and Nordic countries during 1995–2017. We find a high degree of synchronization between Lithuania’s credit and housing price cycles. Panel regressions show a strong correlation between a credit upturn and housing price upturn. Moreover, panel VAR suggests that shocks in housing prices, credit, and output within and

outside Lithuania strongly impact Lithuania’s credit.”

A new IMF working paper by Iacovos Ioannou says that:

“Lithuania’s current credit cycle highlights the strong link between housing prices and credit. We explore this relationship in more detail by analyzing the main features of credit, housing price, and output cycles in Baltic and Nordic countries during 1995–2017. We find a high degree of synchronization between Lithuania’s credit and housing price cycles. Panel regressions show a strong correlation between a credit upturn and housing price upturn.

Posted by at 10:05 AM

Labels: Global Housing Watch

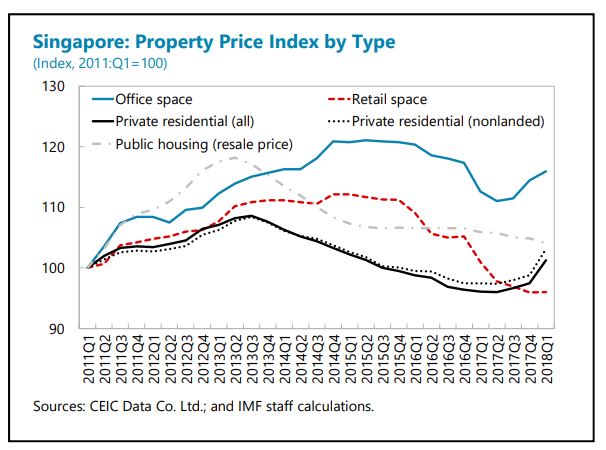

Housing Market in Singapore

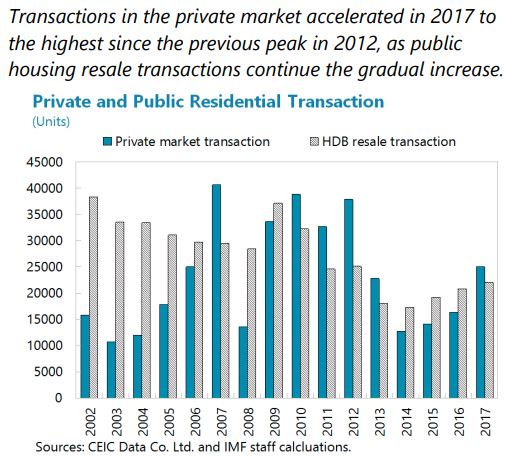

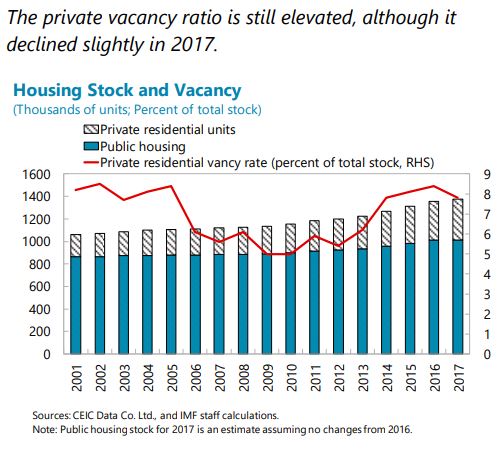

The IMF’s latest report on Singapore says that:

“In the housing market, prices of private residential properties staged a steady recovery in 2017, for the first time since 2013, and were up by 5.4 percent y/y in 2018Q1. The share of foreign transactions has remained stable over the past six years (close to 7 percent) but is significantly below the 2011 peak (19.5 percent). Vacancy rates have come down slightly but

are still elevated. In recent quarters, supply in the pipeline (i.e., new and redevelopment projects of private residential units with planning approvals that are expected to be on the market within a few years) has also increased after a few years of falling.”

Singapore’s property market policies are comprehensive, aiming to manage demand and supply with active monitoring and periodic adjustments. Staff’s empirical analysis suggests that the prices of private housing in Singapore are affected by a host of factors, including incomes, rents and interest rates, and by supply and cost determinants. Moreover, while housing prices in major Asian cities are increasingly synchronized, Singapore’s property prices appear to have decoupled and are now relatively attractive to international investors (…). Singapore’s comprehensive set of property market cooling measures, including Additional Buyer’s Stamp Duty (ABSD) and limits on Total Debt Servicing Ratio (TDSR) and Loan to Value (LTV) caps, have been critical to stabilizing the property market. Property prices picked up in the last three quarters and are expected to increase further in the near term. Staff analysis also suggests that prices are now moderately above levels consistent with long-term fundamentals. Higher private property prices have been accompanied by increased transaction volumes amid a stronger economy, improved market sentiments, and the recent increase in collective sales for redevelopment projects. The Seller’s Stamp Duty was relaxed in March 2017. In the 2018 Budget, the Buyer’s Stamp Duty was raised by one percentage point for residential properties valued over S$1 million, justified by the need to make property

taxation more progressive.Against this background, staff’s views on property market measures are as follows:

- On the demand side, property market cooling measures should be maintained, including structural macroprudential policies (TDSR and LTV caps) and cyclical measures, such as ABSD, given the elevated financial risks. However, ABSD is a residency-based capital flow management/macro-prudential measure, and staff recommends eliminating residency-based differentiation by unifying rates (lowering rates charged foreigners to the level charged Singaporeans and foreign residents), and then phasing out the measure once systemic risks from the housing market dissipate.

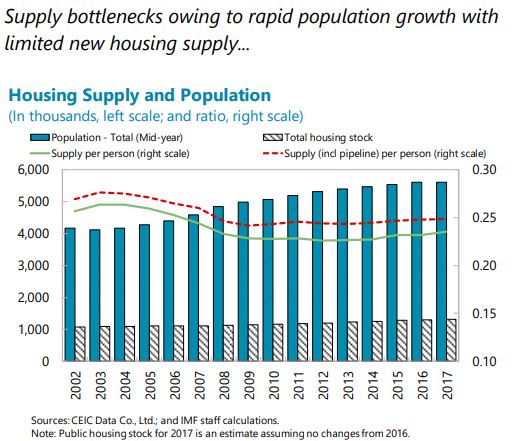

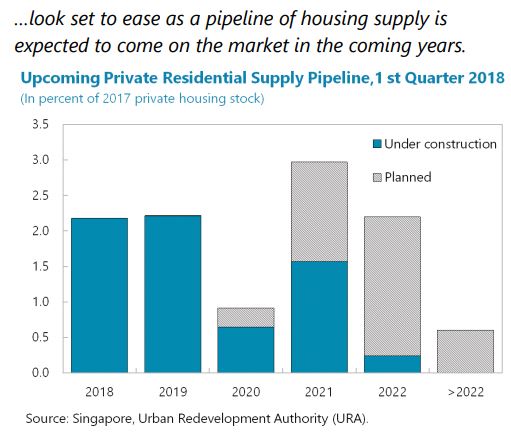

- On the supply side, housing supply in the pipeline has continued to rise in 2018Q1. A large part of those will be on the market for sale in later this year or the next year, adding significant new supplies of housing stock. Staff encourages the authorities to continue to monitor the supply side to ensure that sufficient land is reserved and released in a timely manner through the government land sales program. In addition, other supply-side measures such as the process of building approval could be targeted to meet housing demand.”

The IMF’s latest report on Singapore says that:

“In the housing market, prices of private residential properties staged a steady recovery in 2017, for the first time since 2013, and were up by 5.4 percent y/y in 2018Q1. The share of foreign transactions has remained stable over the past six years (close to 7 percent) but is significantly below the 2011 peak (19.5 percent). Vacancy rates have come down slightly but

are still elevated.

Posted by at 10:01 AM

Labels: Global Housing Watch

Friday, July 27, 2018

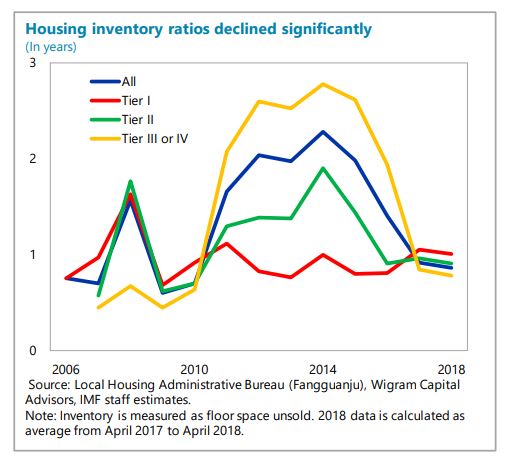

Housing Market in China

The IMF’s latest report on China says that:

- “Housing inventories in smaller cities declined considerably, due in part to social housing programs. House price growth moderated following the tightening measures since late 2016.”

- “A more sustainable housing market. The government’s “long-term mechanism for housing” appropriately focuses on addressing fundamental supply-demand imbalances. Ensuring long-run sustainability of the housing market requires increasing land supply for residential housing, promoting rental markets, and reducing the reliance of local governments on land sales. De-emphasizing growth targets would allow housing investment to be driven by long-run fundamentals, rather than the need to manage economic cycles. Staff’s projection indicates that residential investment, a key growth engine over the last decade, will decline as a share of GDP over the medium term as household income and consumption growth moderates.”

The IMF’s latest report on China says that:

- “Housing inventories in smaller cities declined considerably, due in part to social housing programs. House price growth moderated following the tightening measures since late 2016.”

- “A more sustainable housing market. The government’s “long-term mechanism for housing” appropriately focuses on addressing fundamental supply-demand imbalances. Ensuring long-run sustainability of the housing market requires increasing land supply for residential housing,

Posted by at 3:50 PM

Labels: Global Housing Watch

Subscribe to: Posts