Showing posts with label Global Housing Watch. Show all posts

Friday, November 9, 2018

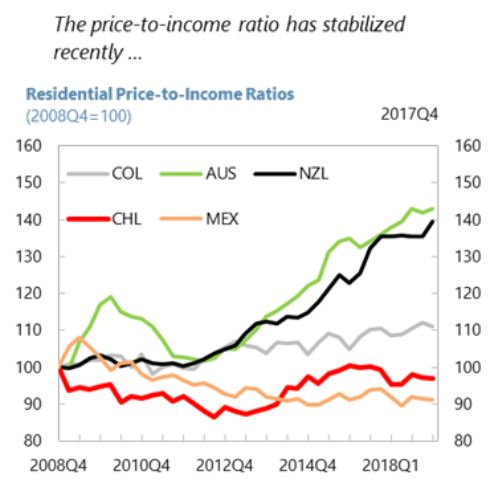

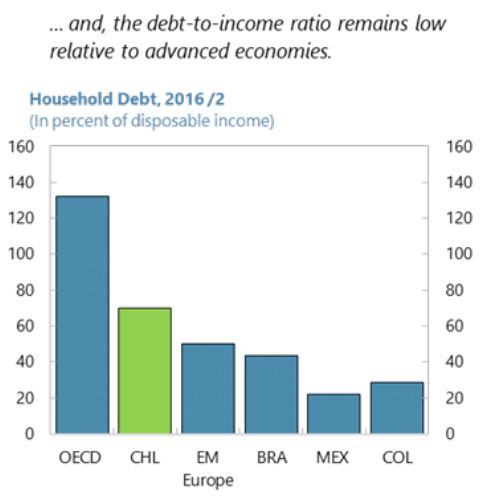

Chile: Housing Market Developments

Posted by at 4:20 PM

Labels: Global Housing Watch

Housing View – November 9, 2018

On cross-country:

- 2018 Housing Finance in Africa Yearbook – Centre for Affordable Housing Finance in Africa

- Pockets of risk in European Housing Markets: then and now – Central Bank of Ireland

- UN Special Rapporteur Leilani Farha on homelessness, human rights and why the lack of adequate housing is on the rise – Al Jazeera

- ULI/ PwC’s Emerging Trends in Real Estate Europe 2019 – Urban Land Institute

On the US:

- Birth Rates and Home Values: A Closer Look – Zillow

- Affordability, Disruption & Rising Interest Rates Lead Top Ten Issues Facing Real Estate – National Association of Realtors

- US Housing: As good as it gets? – ING

- When Millennials Battle Boomers Over Housing – Citylab

- Ballots for Buildings: Voters Weigh Affordable Housing Measures – The Pew Charitable Trusts

- Are median incomes actually stagnating? How we calculate housing costs affects the answer – Urban Institute

- Amazon’s real estate team did its homework – Brookings

- How Minimum Zoning Mandates Can Improve Housing Markets and Expand Opportunity – The Aspen Institute

- Resilience and housing markets: Who is it really for? – Land Use Policy

On other countries:

- [Australia] Australia’s Property Slump Casts Doubt on Household Spending – Bloomberg

- [Australia] Significant drop in auction rates set alarm bells ringing for major Australian housing markets – Global Property Guide

- [Canada] Vancouver’s complicated relationship with Chinese money – CBC

- [China] Three New Signs China’s Housing Market Slowdown Is Taking Hold – Bloomberg

- [Denmark] Party is over for apartment owners – but the Danish housing market is picking up – Danske Bank

- [Hungary] Measuring Heterogeneity of House Price Developments in Hungary, 1990–2016 – Central Bank of Hungary

Photo by Aliis Sinisalu

On cross-country:

- 2018 Housing Finance in Africa Yearbook – Centre for Affordable Housing Finance in Africa

- Pockets of risk in European Housing Markets: then and now – Central Bank of Ireland

- UN Special Rapporteur Leilani Farha on homelessness, human rights and why the lack of adequate housing is on the rise – Al Jazeera

- ULI/ PwC’s Emerging Trends in Real Estate Europe 2019 – Urban Land Institute

On the US:

- Birth Rates and Home Values: A Closer Look – Zillow

- Affordability,

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, November 5, 2018

Balancing Financial Stability and Housing Affordability: The Case of Canada

From the IMF’s latest report on Canada:

“Housing market imbalances are a key source of systemic risk and can adversely affect housing affordability. This paper utilizes a stylized model of the Canadian economy that includes policymakers with differing objectives—macroeconomic stability, financial stability, and housing affordability. Not surprisingly, when faced with multiple objectives, deploying more policy instruments can lead to better outcomes. The results show that macroprudential policy can be more effective than policies based on adjusting propertytransfer taxes because property-tax policy entails excessive volatility in tax rates. They also show that if property-transfer taxes are used as a policy instrument, taxes targeted at a broader-set of homebuyers can be more effective than measures targeted at a smaller subset of homebuyers, such as nonresident homebuyers.”

From the IMF’s latest report on Canada:

“Housing market imbalances are a key source of systemic risk and can adversely affect housing affordability. This paper utilizes a stylized model of the Canadian economy that includes policymakers with differing objectives—macroeconomic stability, financial stability, and housing affordability. Not surprisingly, when faced with multiple objectives, deploying more policy instruments can lead to better outcomes. The results show that macroprudential policy can be more effective than policies based on adjusting propertytransfer taxes because property-tax policy entails excessive volatility in tax rates.

Posted by at 9:49 AM

Labels: Global Housing Watch

Friday, November 2, 2018

Housing View – November 2, 2018

On cross-country:

- 500 Years of Urban Rents, Housing Quality and Affordability – Research Gate

On the US:

- Seventh annual AEI-CRN conference on housing markets and finance: Supply, demand, and pro-cyclical forces – American Enterprise Institute

- Lynn Fisher on affordable housing and US housing markets – American Enterprise Institute

- Changes in Supply and Demand at Various Segments of the Rental Market: How Do They Match Up? – Harvard Joint Center for Housing Studies

- Creepin’ it Real: Haunted Neighborhoods and Their Home Values – Trulia

- American Abodes: Where International House Hunters are Searching for Homes – Trulia

- Why there’s no bubble in the US housing market – AsianInvestor

- Intergenerational Homeownership – Urban Institute

- Mortgage Rates Are Pushing U.S. Homes Out of Reach – Bloomberg

- How Airbnb’s Tech Is Impacting People’s Fundamental Human Rights – Forbes

- No, rent control doesn’t always reduce the supply of housing – Los Angeles Times

- Rent Control Returns: Thoughts and Evidence – Conversable Economist

On other countries:

- [China] Local capital scarcity and industrial decline caused by China’s real estate booms – VOX

- [Greece] Seeking a bargain, and taste of the good life, Chinese buy Greek homes – Reuters

- [Singapore] Singapore’s Public Housing, Envy of World, Hits Rough Patch – Bloomberg

- [Spain] Little Caracas, el barrio de lujo que se ha instalado en el centro de Madrid – GQ

- [United Kingdom] Curtain comes down on Help to Buy – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- 500 Years of Urban Rents, Housing Quality and Affordability – Research Gate

On the US:

- Seventh annual AEI-CRN conference on housing markets and finance: Supply, demand, and pro-cyclical forces – American Enterprise Institute

- Lynn Fisher on affordable housing and US housing markets – American Enterprise Institute

- Changes in Supply and Demand at Various Segments of the Rental Market: How Do They Match Up?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, October 26, 2018

Housing View – October 26, 2018

On cross-country:

- Housing expenditures and income inequality: Shifts in housing costs exacerbated the rise in income inequality – VOX

- Cost of greener homes too high, Europe tells ING survey – ING

- Report on UN Special Rapporteur on the Right to Housing – National Economics & Social Rights Initiative

On the US:

- What does economic evidence tell us about the effects of rent control? – Brookings

- Star Tribune Op-Ed: Affordable housing crisis demands more supply – Federal Reserve Bank of Minneapolis

- Computer Vision and Real Estate: Do Looks Matter and Do Incentives Determine Looks – NBER

- New Book Asks: What It Would Take to Foster Communities of Inclusion in an Era of Inequality? – Harvard Joint Center for Housing Studies

- California has a housing crisis, and Californians seem confused about how to solve it – American Enterprise Institute

- Home Sales Are Dropping — Could The Housing Market Finally Be Cooling Off? – NPR

- Tax practices that amplify racial inequities: Property tax treatment of owner-occupied housing – D.C. Policy Center

On other countries:

- [Brazil] Brazil’s home buyers bet on the ballot – Financial Times

- [Germany] Germany’s housing crisis fuels black market for refugees – Reuters

- [Ireland] Is Dublin’s property market heading for a soft landing? – Financial Times

- [New Zealand] Ban on foreign buyers seen poor answer to New Zealand’s housing shortage – Reuters

- [Spain] Spanish banks hit by supreme court ruling on mortgage fees – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Housing expenditures and income inequality: Shifts in housing costs exacerbated the rise in income inequality – VOX

- Cost of greener homes too high, Europe tells ING survey – ING

- Report on UN Special Rapporteur on the Right to Housing – National Economics & Social Rights Initiative

On the US:

- What does economic evidence tell us about the effects of rent control?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts