Showing posts with label Global Housing Watch. Show all posts

Thursday, September 13, 2018

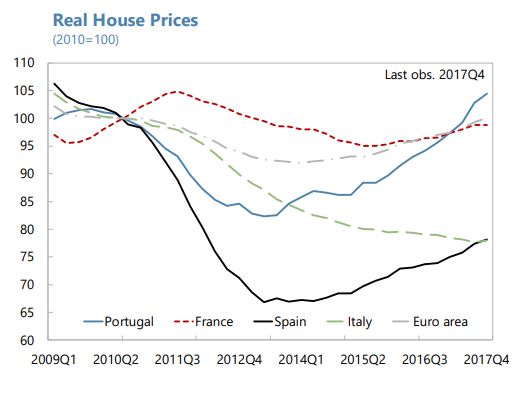

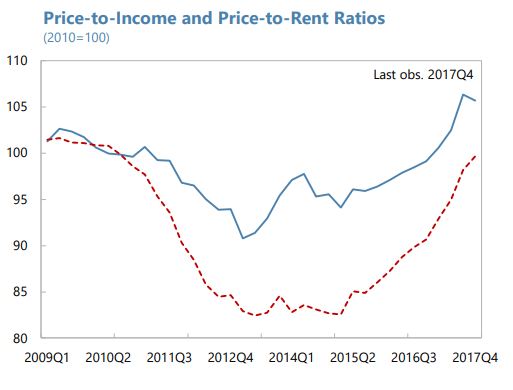

House Prices in Portugal

The IMF’s new report on Portugal says:

“Housing prices continue to increase, but there is no significant overvaluation yet. Following a decline of 18 percent in real terms over 2010–13, housing prices have since increased by

about 20 percent in real terms (7.9 percent in 2017), especially in Lisbon, Porto and the Algarve region. While the increases have been driven largely by transactions on existing dwellings by non-residents, the share of housing transactions financed by Portuguese mortgages has been growing since 2015 (reaching 41 percent in the last quarter of 2017). Estimates in the ECB’s May 2018 Financial Stability Review suggest that there are incipient signs of overvaluation in the residential real estate market. The authorities should continue to improve the quality of real estate data and related analytical tools, and to monitor mortgage markets and the evolution of risks to banks from developments in real estate markets.”

The IMF’s new report on Portugal says:

“Housing prices continue to increase, but there is no significant overvaluation yet. Following a decline of 18 percent in real terms over 2010–13, housing prices have since increased by

about 20 percent in real terms (7.9 percent in 2017), especially in Lisbon, Porto and the Algarve region. While the increases have been driven largely by transactions on existing dwellings by non-residents, the share of housing transactions financed by Portuguese mortgages has been growing since 2015 (reaching 41 percent in the last quarter of 2017).

Posted by at 10:44 AM

Labels: Global Housing Watch

Friday, September 7, 2018

Housing View – September 7, 2018

On cross-country:

- Global developments in residential property prices – first quarter of 2018 – Bank for International Settlements

- Hypostat 2018: recent developments in housing and mortgage markets in Europe and beyond – European Mortgage Federation

- The effect of house prices on household borrowing: A new approach – VOX

- Global luxury house prices: performance in 2018 so far – Knight Frank

On the US:

- The story of a house: how private equity swooped in after the subprime crisis – Financial Times

- Measuring Gentrification: Using Yelp Data to Quantify Neighborhood Change – NBER

- Liquidity vs. Wealth in Household Debt Obligations: Evidence from Housing Policy in the Great Recession – NBER

- Lessons from the financial crisis: The central importance of a sustainable, affordable and inclusive housing market – Brookings

- Three ways to strengthen the affordable rental housing supply – Urban Institute

On other countries:

- [Australia] Australia’s property boom ends as credit squeeze begins – Financial Times

- [Brazil] Can Housing Be Affordable Without Being Efficient? – World Resources Institute

- [China] China struggles to heed Xi’s call to develop rental housing – Financial Times

- [China] Housing Affordability in Urban China: A Comprehensive Overview – SSRN

- [Hong Kong] Hong Kong’s hot property sector show signs of cooling – Financial Times

- [Hong Kong] Hong Kong’s Runaway Property Market May Be Heading for a Fall – Bloomberg

- [Netherlands] Netherlands’ housing market remains strong – Global Property Guide

- [United Kingdom] History Dependence in the Housing Market – Centre for Economic Performance

- [United Kingdom] London housing: the bearish Brexit take – Financial Times

- [United Kingdom] Can house prices teach us anything about schools? – BBC

Photo by Aliis Sinisalu

On cross-country:

- Global developments in residential property prices – first quarter of 2018 – Bank for International Settlements

- Hypostat 2018: recent developments in housing and mortgage markets in Europe and beyond – European Mortgage Federation

- The effect of house prices on household borrowing: A new approach – VOX

- Global luxury house prices: performance in 2018 so far – Knight Frank

On the US:

- The story of a house: how private equity swooped in after the subprime crisis – Financial Times

- Measuring Gentrification: Using Yelp Data to Quantify Neighborhood Change – NBER

- Liquidity vs.

Posted by at 10:26 AM

Labels: Global Housing Watch

Thursday, September 6, 2018

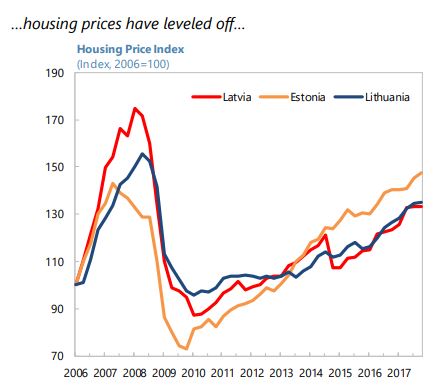

Housing Market in Latvia

The IMF’s latest report on Latvia says:

“Improve access to housing. Current rental regulations discourage investment in rental housing. Below-market rents are common—a legacy of Soviet-era rental agreements—and rental dispute resolution mechanisms are time consuming and costly. More rental housing would facilitate labor mobility and help stem emigration.”

The IMF’s latest report on Latvia says:

“Improve access to housing. Current rental regulations discourage investment in rental housing. Below-market rents are common—a legacy of Soviet-era rental agreements—and rental dispute resolution mechanisms are time consuming and costly. More rental housing would facilitate labor mobility and help stem emigration.”

Posted by at 10:34 AM

Labels: Global Housing Watch

Friday, August 31, 2018

Housing View – August 31, 2018

On cross-country:

- Big City Housing Doesn’t Have to Be So Expensive – Bloomberg

- The Impact of Housing Costs on Regional Income Inequality – Federal Reserve Bank of St. Louis

- What Airbnb really does to a neighbourhood – BBC

On the US:

- Amazon HQ2: How did we get here? What comes next? – Brookings

- The Politics of Homeownership – Citylab

- The Trump Tax Cuts Were Supposed to Depress Housing Prices. They Haven’t. – New York Times

- Maybe we CAN build our way out of an urban housing shortage – Public Square

Photo by Aliis Sinisalu

On cross-country:

- Big City Housing Doesn’t Have to Be So Expensive – Bloomberg

- The Impact of Housing Costs on Regional Income Inequality – Federal Reserve Bank of St. Louis

- What Airbnb really does to a neighbourhood – BBC

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, August 27, 2018

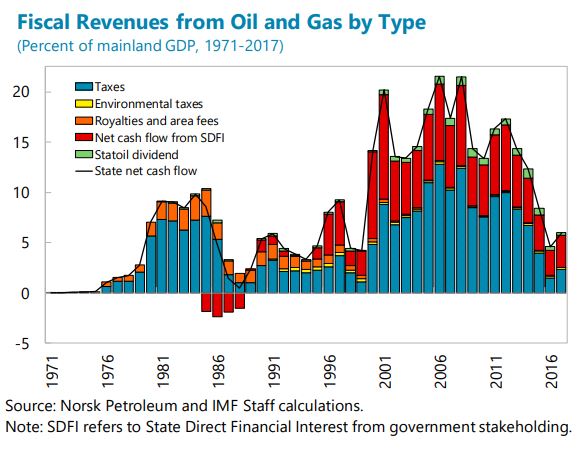

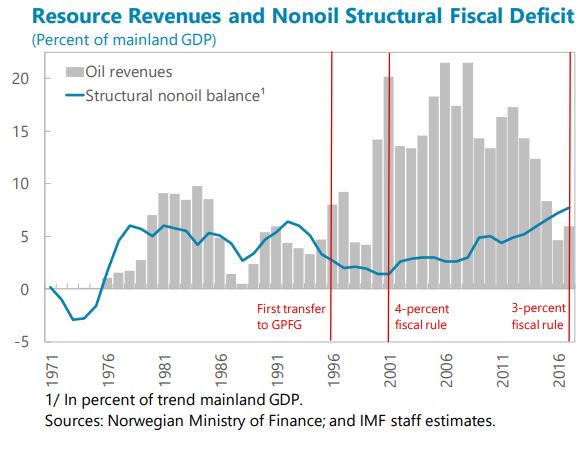

Counting the Oil Money and the Elderly: Norway’s Public Sector Balance Sheet

A new IMF working paper by Ezequiel Cabezon and Christian Henn says:

“Based on a permanent income analysis, Gagnon (2018) has prominently suggested that Norway has saved too much, thereby free-riding on the rest of the world for demand. Our public sector balance sheet analysis comes to the opposite conclusion, chiefly because it also accounts for future aging costs. Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP. But its nonoil fiscal deficits have grown very large (to almost 8 percent of mainland GDP) and aging pressures are only commencing. Therefore, Norway’s intertemporal financial net worth (IFNW) is negative, at about -240 percent of mainland GDP. As IFNW represents an intertemporal budget constraint, this implies that Norway’s savings are likely insufficient to address aging costs without additional fiscal action.”

A new IMF working paper by Ezequiel Cabezon and Christian Henn says:

“Based on a permanent income analysis, Gagnon (2018) has prominently suggested that Norway has saved too much, thereby free-riding on the rest of the world for demand. Our public sector balance sheet analysis comes to the opposite conclusion, chiefly because it also accounts for future aging costs. Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP.

Posted by at 1:50 PM

Labels: Global Housing Watch, Inclusive Growth

Subscribe to: Posts