Showing posts with label Global Housing Watch. Show all posts

Monday, October 1, 2018

Sectoral Booms and Misallocation of Managerial Talent: Evidence from the Chinese Real Estate Boom

From a new IMF working paper by Yu Shi:

“This paper identifies a new mechanism leading to inefficiency in capital reallocation at the extensive margin when an economy experiences a sectoral boom. I argue that imperfections in the financial market and capital barriers to entry in the booming sector create a misallocation of managerial talent. Using comprehensive firm-level data from China, I first provide evidence that more productive firms reallocate capital to the booming real estate sector, and demonstrate that the pattern is likely driven by fewer financial constraints on these firms. I then use a structural estimation to verify the talent misallocation. Finally, I calibrate a dynamic model and find that the without the misallocation, the TFP growth in the manufacturing sector would have improved by 0.5% per year.”

From a new IMF working paper by Yu Shi:

“This paper identifies a new mechanism leading to inefficiency in capital reallocation at the extensive margin when an economy experiences a sectoral boom. I argue that imperfections in the financial market and capital barriers to entry in the booming sector create a misallocation of managerial talent. Using comprehensive firm-level data from China, I first provide evidence that more productive firms reallocate capital to the booming real estate sector,

Posted by at 10:31 AM

Labels: Global Housing Watch

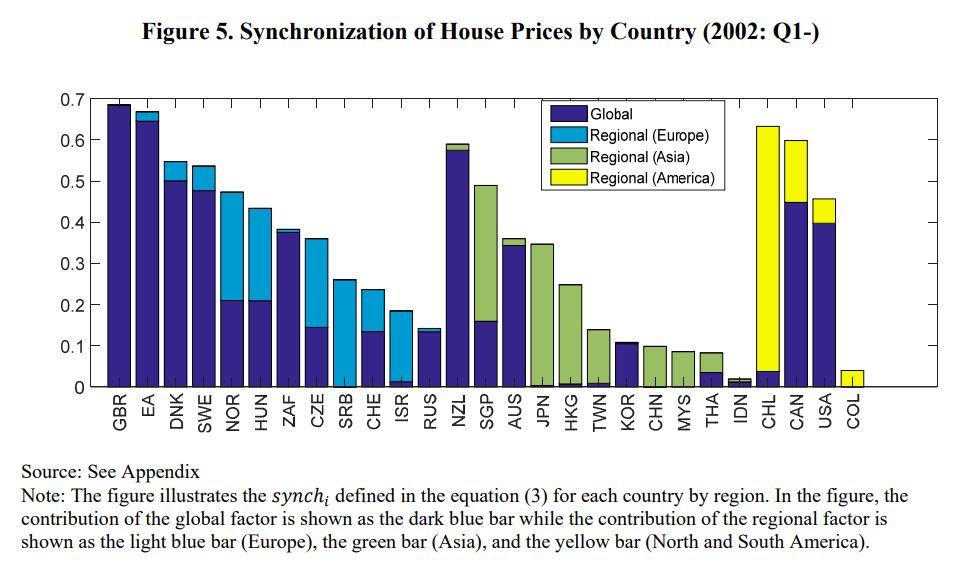

House Price Synchronization and Financial Openness: A Dynamic Factor Model Approach

From a new IMF working paper by Mitsuru Katagiri:

“This paper investigates the developments in house price synchronization across countries by a dynamic factor model using a country- and city-level dataset, and examines what drives the synchronization. The empirical results indicate that: (i) the degree of synchronization has been rising since the 1970s, and (ii) a large heterogeneity in the degree of synchronization exists across countries and cities. A panel and cross-sectional regression analysis show that the heterogeneity of synchronization is partly accounted for by the progress in financial and trade openness. Also, the city-level analysis implies that the international synchronization is mainly driven by the city-level connectivity between large and international cities.”

From a new IMF working paper by Mitsuru Katagiri:

“This paper investigates the developments in house price synchronization across countries by a dynamic factor model using a country- and city-level dataset, and examines what drives the synchronization. The empirical results indicate that: (i) the degree of synchronization has been rising since the 1970s, and (ii) a large heterogeneity in the degree of synchronization exists across countries and cities. A panel and cross-sectional regression analysis show that the heterogeneity of synchronization is partly accounted for by the progress in financial and trade openness.

Posted by at 10:28 AM

Labels: Global Housing Watch

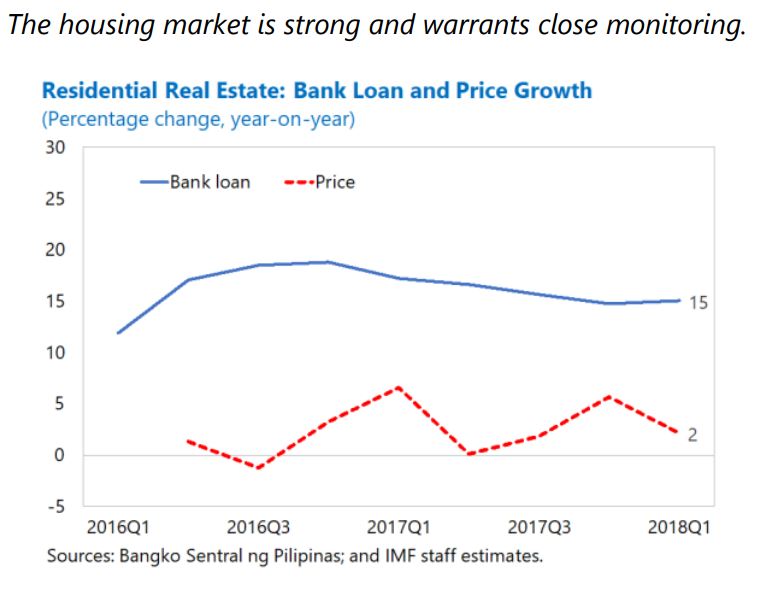

House Prices in Philippines

The latest IMF report on Philippines points out that:

Posted by at 10:23 AM

Labels: Global Housing Watch

Friday, September 28, 2018

Housing View – September 28, 2018

On the US:

- Perception of House Price Risk and Homeownership – NBER

- Affordable Housing: Hard Way and Easy Way – Cato Institute

- Barriers to Accessing Homeownership Down Payment, Credit, and Affordability – 2018 – Urban Institute

- Texas Property Taxes Soar as Homeowners Confront Rising Values – Federal Reserve Bank of Dallas

- The housing bubble, the credit crunch, and the Great Recession: A reply to Paul Krugman – Brookings

- America Needs to Revive the American Dream of Homeownership – Bloomberg

- How Much Will Homeowners Spend to Rebuild & Repair After Hurricane Florence? – Harvard Joint Center for Housing Studies

- Affordable housing is just the beginning of YIMBY – VOX

- Builders Slump as U.S. Housing Market Shifts to the Slow Lane – Bloomberg

- Is There a Better Way to Measure Housing Affordability? – Harvard Joint Center for Housing Studies

- Elizabeth Warren’s Ambitious Fix for America’s Housing Crisis – The Atlantic

- School shootings affect school quality, housing value – University of Illinois at Urbana – Champaign

- Building More Houses Isn’t Always the Answer – Bloomberg

On other countries:

- [Chile] ¿Cómo influye la cercanía del Metro en el valor de una propiedad? – CNN

- [China] Understanding Real Estate Price Dynamics: The Case of Housing Prices in Five Major Cities of China – Journal of Housing Economics

- [China] How Much Would China’s GDP Respond to a Slowdown in Housing Activity? – Federal Reserve Bank of Kansas City

- [China] China Developers’ Funding Source at Risk in Sales Crackdown – Bloomberg

- [Germany] Germany sets out measures to tackle affordable housing shortage – Reuters

- [Germany] Germany’s soaring housing prices spark calls for reform – Deutsche Welle

- [Hong Kong] Higher interest rates threaten overvalued property markets – Financial Times

- [Hong Kong] Hong Kong at greatest risk of housing bubble: UBS – Financial Times

- [United Kingdom] Is Richmond the Nimbyest place in London? – Financial Times

Photo by Aliis Sinisalu

On the US:

- Perception of House Price Risk and Homeownership – NBER

- Affordable Housing: Hard Way and Easy Way – Cato Institute

- Barriers to Accessing Homeownership Down Payment, Credit, and Affordability – 2018 – Urban Institute

- Texas Property Taxes Soar as Homeowners Confront Rising Values – Federal Reserve Bank of Dallas

- The housing bubble, the credit crunch,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, September 21, 2018

Housing View – September 21, 2018

On cross-country:

- Q2 2018: Global house price boom – strong house price rises continue in Europe and parts of Asia – Global Property Guide

- Eurozone housing market cycle is maturing – ING

- Disillusion mounts in Europe’s housing market – ING

On the US:

- Price-to-Income Ratios are Nearing Historic Highs – Harvard Joint Center for Housing Studies

- Why do so many affordable-housing advocates reject the law of supply and demand? – Washington Post

- The Mortgage Market Is Back a Decade After the Credit Crisis—With New Risks – Bloomberg

- Jeff Bezos Homeless Pledge Follows Amazon Fight Against Housing Tax – Bloomberg

- Census: Renters’ Incomes Still Lagging Behind Housing Costs – Center on Budget and Policy Priorities

- New evidence shows manufactured homes appreciate as well as site-built homes – Urban Institute

- ‘As safe as houses’: How a small corner of the US mortgage market nearly brought down the global financial system – Bank of England

- Does Rising Housing Inventory Signal the Beginning of a Buyer’s Market? – First American

- The Wealth Hiding in Your Neighborhood – Institute for Policy Studies

- Luxury Real Estate Boom Adds to Risk of Climate Disruption – Institute for Policy Studies

- Tough Times Ahead for Housing – Wall Street Journal

On other countries:

- [Brazil] Brazil’s house prices still falling, but outlook positive – Global Property Guide

- [China] China’s Weakest Housing Markets Flash Red in Cautionary Tale – Bloomberg

- [China] One of China’s Wildest Housing Markets Is Broken – Bloomberg

- [China] How China’s plan to develop rental housing backfired – Reuters

- [Chile] Chile’s house prices continue to rise modestly, despite the imposition of 19% VAT on property sales – Global Property Guide

- [Ireland] Ireland sets up land agency as anger grows at housing shortage – Reuters

- [Ireland] Dublin’s Housing Crisis Reaches a Boiling Point – CityLab

- [Malta] Malta house price growth outstrips Hong Kong to take top ranking – Financial Times

- [New Zealand] New Zealand’s house prices are rising again – Global Property Guide

- [South Korea] Korea imposes tougher taxes on properties to curb price surge – Reuters

- [Ukraine] Ukraine’s house price falls accelerating – Global Property Guide

- [United Kingdom] Is UK property still a good investment? – Financial Times

- [United Kingdom] K. House Prices at Risk From Brexit – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- Q2 2018: Global house price boom – strong house price rises continue in Europe and parts of Asia – Global Property Guide

- Eurozone housing market cycle is maturing – ING

- Disillusion mounts in Europe’s housing market – ING

On the US:

- Price-to-Income Ratios are Nearing Historic Highs – Harvard Joint Center for Housing Studies

- Why do so many affordable-housing advocates reject the law of supply and demand?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts