Showing posts with label Global Housing Watch. Show all posts

Friday, November 16, 2018

Housing View – November 16, 2018

On cross-country:

- Living and Leaving: Housing, Mobility and Welfare in the European Union – World Bank

- Why house prices in global cities are falling – Economist

- Comment – On building typologies of housing systems in the OECD – IDEAS

On the US:

- California Midterm Results: Funding for Affordable Housing and a Rent Control Defeat – New York Times

- Collateral Damage: The Impact of Foreclosures on New Home Mortgage Lending in the 1930s – NBER

- No boom, no bust in US housing – Financial Times

- Local Banks, Credit Supply, and House Prices – Federal Reserve Bank of New York

- Income Tax Expenditures for Housing and Homeownership – Tax Policy Center

- Housing America’s Older Adults 2018 – Harvard Joint Center for Housing Studies

- Housing Sentiment Continues Downward Trend Despite Favorable Economy – Fannie Mae

- Buy young, earn more: Buying a house before age 35 gives homeowners more bang for their buck – Urban Institute

- Consumer-Lending Discrimination in the Era of FinTech – UC Berkeley

- Supply Skepticism: Housing Supply and Affordability – NYU Furman Center

- Why Cities Must Tackle Single-Family Zoning – CityLab

On other countries:

- [Australia] Assessing the Effects of Housing Lending Policy Measures – Reserve Bank of Australia

- [China] A Fifth of China’s Homes Are Empty. That’s 50 Million Apartments – Bloomberg

- [France] New or old, why would housing price indices differ? An analysis for France – IDEAS

- [France] The impact of the 2014 increase in the real estate transfer taxes on the French housing market – IDEAS

- [France] Paris property benefits from Brexit bounce – Financial Times

- [France] Does issuing building permits reduce the cost of land? – Bourgogne Franche‑Comté

- [Italy] Home is where the ad is: online interest proxies housing demand – EPJ Data Science

- [Slovak Republic] Housing Policy in the Slovak Republic – Slovak University of Technology in Bratislava

- [Spain] La demanda sigue impulsando nuevos proyectos de inversión residencial – BBVA

- [United Kingdom] The collapse in public ownership of land – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Living and Leaving: Housing, Mobility and Welfare in the European Union – World Bank

- Why house prices in global cities are falling – Economist

- Comment – On building typologies of housing systems in the OECD – IDEAS

On the US:

- California Midterm Results: Funding for Affordable Housing and a Rent Control Defeat – New York Times

- Collateral Damage: The Impact of Foreclosures on New Home Mortgage Lending in the 1930s – NBER

- No boom,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, November 14, 2018

Macroprudential Policies and House Prices in Europe: An Overview of Recent Experiences

From the IMF’s latest Regional Economic Outlook report for Europe:

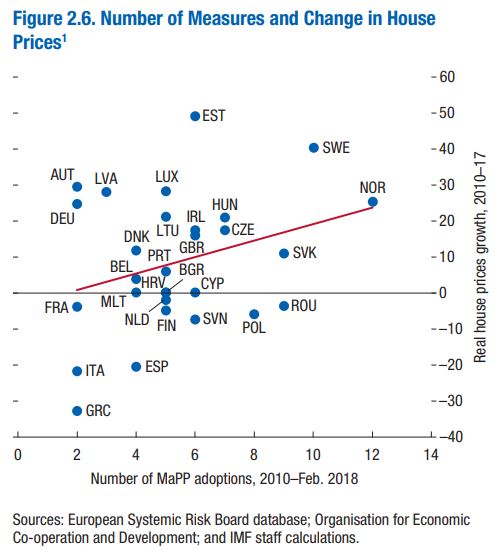

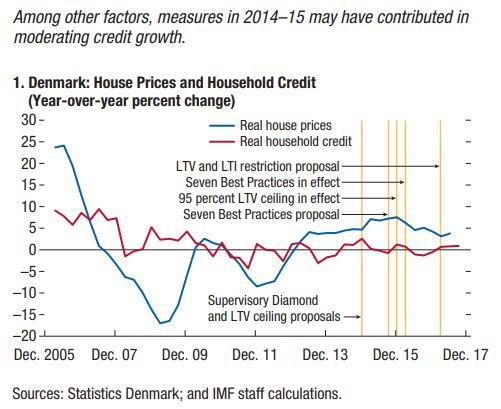

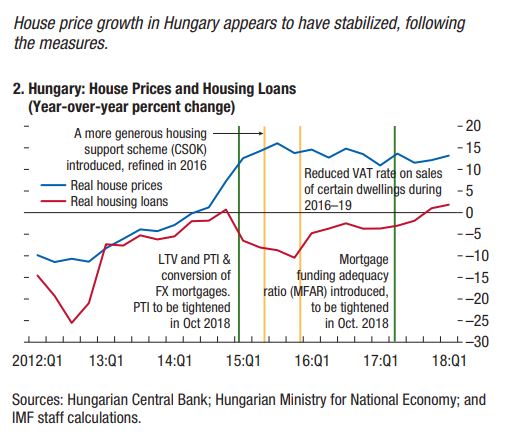

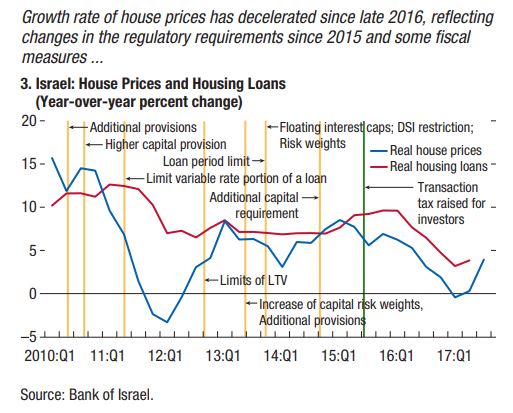

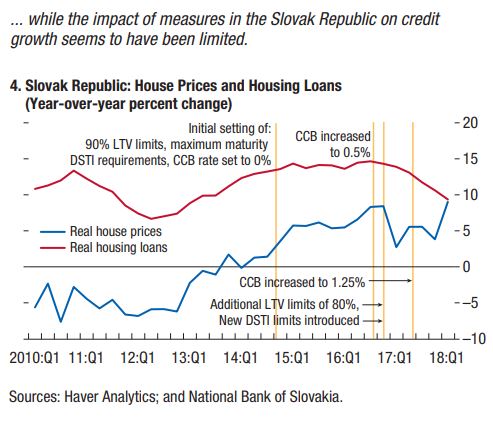

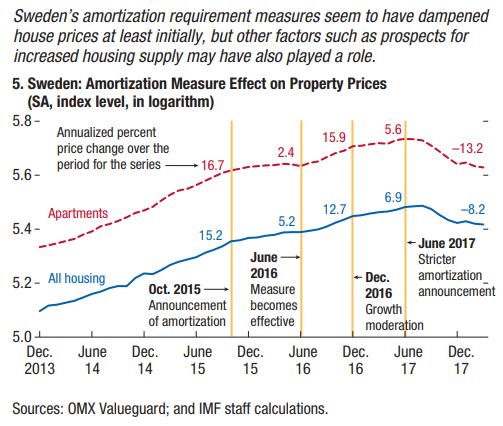

“This chapter documents the increasing use of macroprudential policies (MaPPs) in Europe in recent years to build financial resilience, contain general and sectoral credit growth, and limit house price increases. Considering these objectives and drawing from case studies, the chapter finds evidence that borrower-side measures, supported by lender-side measures, helped limit the share of riskier mortgages, thereby building resilience. Evidence is more mixed as to the ability of MaPPs to contain house price and overall credit growth against the backdrop of a still-accommodative monetary policy and other factors.

Macroprudential Measures in European Countries

The recent reacceleration in house prices has prompted the adoption of MaPPs in several European countries. Though credit and house price concerns are not yet generalized, house prices have increased substantially in several European countries over the past few years (…). In most of these countries, higher house prices have been accompanied by rising household debt (…) and rapid household credit growth (…).

To contain the buildup of systemic risks, especially in the residential housing market, many European countries have strengthened their MaPPs (…). While MaPPs have been

implemented across Europe, countries with larger postcrisis increases in house prices and household debt tended to adopt more MaPPs (…).The main objectives of the recently introduced MaPPs, as stated by country authorities, were improving financial stability, building financial resilience, and containing general and sectoral credit growth. Within these broader objectives, policies were generally focused on protecting borrowers, strengthening banking systems, and slowing down house price increases (…). The latter was an objective in most economies, but particularly in the Czech Republic, Estonia, Norway, and Sweden.

In some countries (Estonia, Norway, Switzerland), the relaxation of lending standards was a major concern. Constraining the rise in the share of loans denominated in foreign currency was a prominent goal in Hungary. The various capital buffers adopted beginning in 2013, in line with the EU Capital Requirements Directive (CRD IV), were aimed at containing not only housing sector imbalances, but also credit cycle swings.”

Continue reading here.

From the IMF’s latest Regional Economic Outlook report for Europe:

“This chapter documents the increasing use of macroprudential policies (MaPPs) in Europe in recent years to build financial resilience, contain general and sectoral credit growth, and limit house price increases. Considering these objectives and drawing from case studies, the chapter finds evidence that borrower-side measures, supported by lender-side measures, helped limit the share of riskier mortgages, thereby building resilience. Evidence is more mixed as to the ability of MaPPs to contain house price and overall credit growth against the backdrop of a still-accommodative monetary policy and other factors.

Posted by at 2:30 PM

Labels: Global Housing Watch

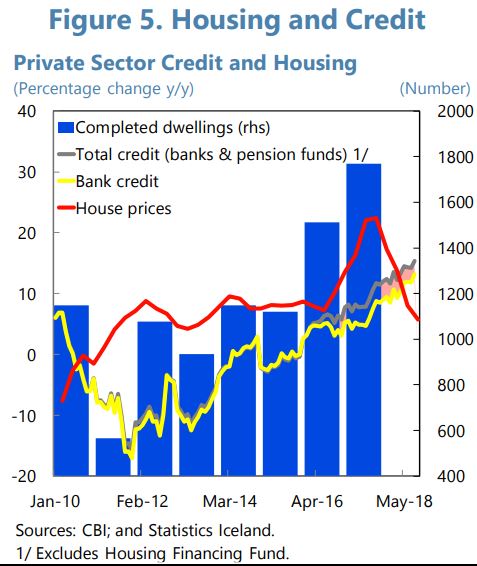

House Prices in Iceland

The IMF’s latest report on Iceland says that:

“The real estate markets have cooled. The rate of growth of housing prices fell from a peak of 24 percent y/y in July 2017 to 6 percent 12 months later, while that for commercial real estate slowed from 19 percent y/y to 15 percent. A robust supply response was key, although slowing tourism growth also helped—including by limiting private rental demand via Airbnb (see for instance Eliasson and Ragnarsson, 2018). Residential investment and commercial construction continue to expand briskly.”

Also, see a separate report on Inflation Targeting in Iceland–The Issue of Housing Costs here.

The IMF’s latest report on Iceland says that:

“The real estate markets have cooled. The rate of growth of housing prices fell from a peak of 24 percent y/y in July 2017 to 6 percent 12 months later, while that for commercial real estate slowed from 19 percent y/y to 15 percent. A robust supply response was key, although slowing tourism growth also helped—including by limiting private rental demand via Airbnb (see for instance Eliasson and Ragnarsson,

Posted by at 2:19 PM

Labels: Global Housing Watch

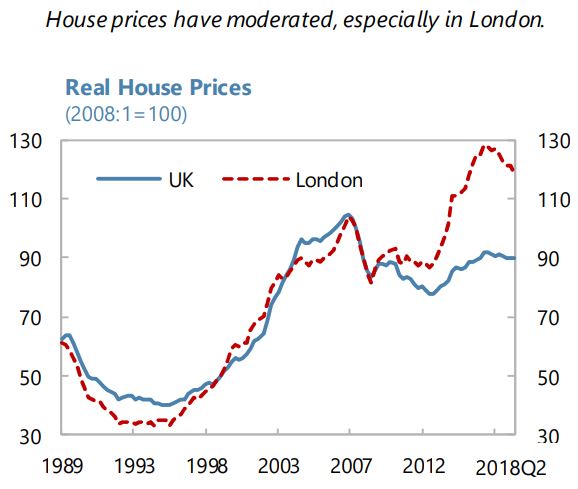

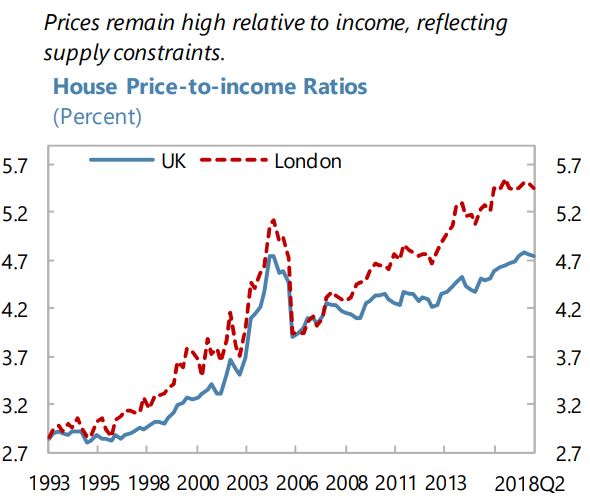

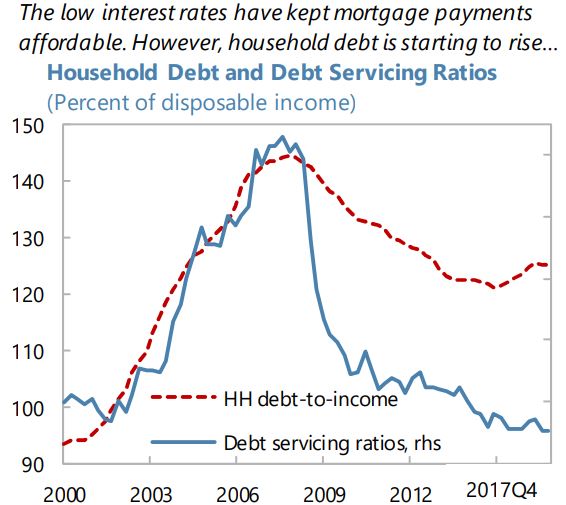

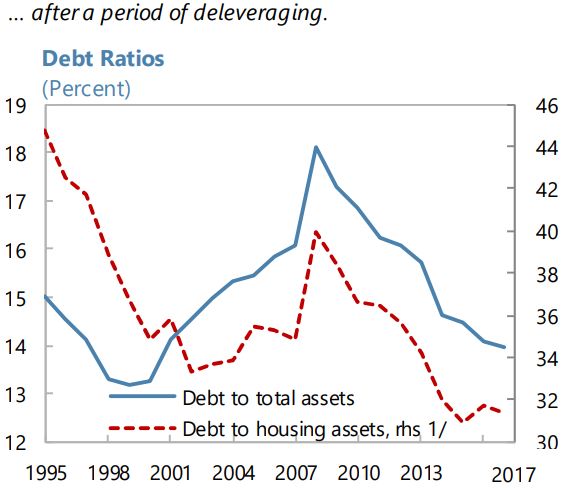

House Prices in United Kingdom

From the IMF’s latest report on the United Kingdom:

“Mortgage lending growth has been moderate, owing in part to subdued demand, as well as macroprudential measures taken in recent years. Despite the recent moderation in residential house price growth (and outright declines in parts of London), house prices remain high relative to incomes (…). The ratio of new mortgage loans at relatively high loan-to-income (LTI) ratios has increased somewhat in the last two years, although the share of highly indebted households remains low. Since 2014, mortgage lenders have been required to test whether borrowers could still afford their mortgages in a stressed rates scenario.”

From the IMF’s latest report on the United Kingdom:

“Mortgage lending growth has been moderate, owing in part to subdued demand, as well as macroprudential measures taken in recent years. Despite the recent moderation in residential house price growth (and outright declines in parts of London), house prices remain high relative to incomes (…). The ratio of new mortgage loans at relatively high loan-to-income (LTI) ratios has increased somewhat in the last two years,

Posted by at 2:13 PM

Labels: Global Housing Watch

Friday, November 9, 2018

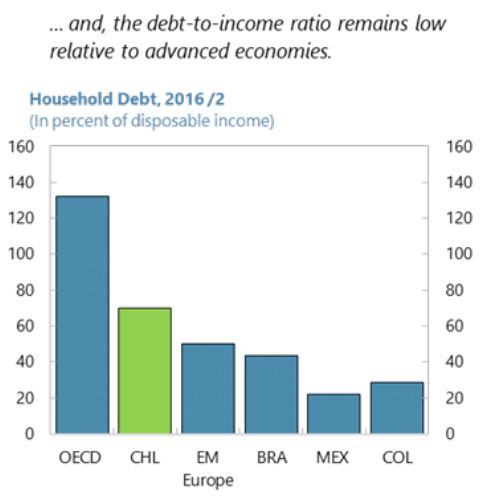

Chile: Housing Market Developments

Posted by at 4:20 PM

Labels: Global Housing Watch

Subscribe to: Posts