Showing posts with label Global Housing Watch. Show all posts

Wednesday, January 16, 2019

Housing Market in Finland

The IMF’s latest report on Finland says:

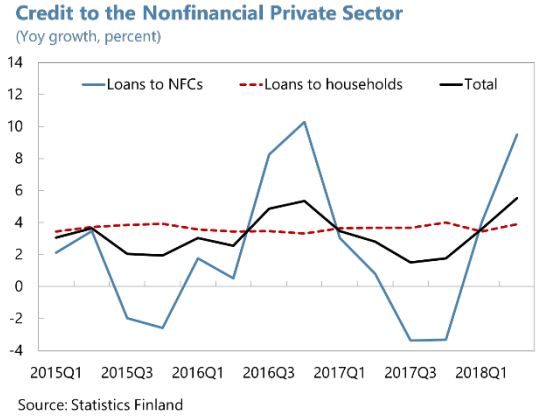

“Credit has expanded moderately overall, but housing corporation loans and consumer credit have been rising more rapidly. Total loan growth to the private nonfinancial sector has remained broadly constant at around 3½ percent for the past five years. Most lending to households has been in the form of secured lending for housing, which has grown around 4 percent. Corporate loan growth has rebounded strongly in the second quarter of the year after a sharp contraction in the second half of 2017. Two lending categories stand out:

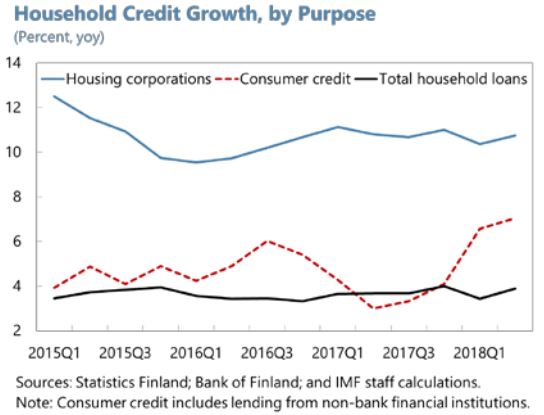

Loans to housing corporations have been expanding rapidly—above 10 percent—for many years. The drivers—expansion of the housing stock and renovation of rental properties—are

healthy. But the shareholders of housing corporations include homeowners, making these de facto indirect loans to households, and households might thereby be tempted to take on more debt than can easily be repaid.Consumer credit has been increasing steadily—above 7 percent y/y in the second quarter of 2018—and now accounts for 12 percent of aggregate household debt, driven by credit

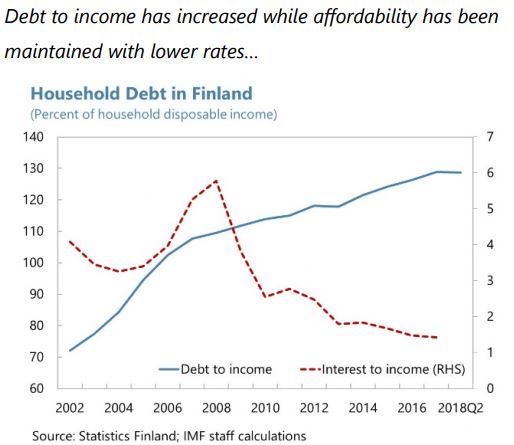

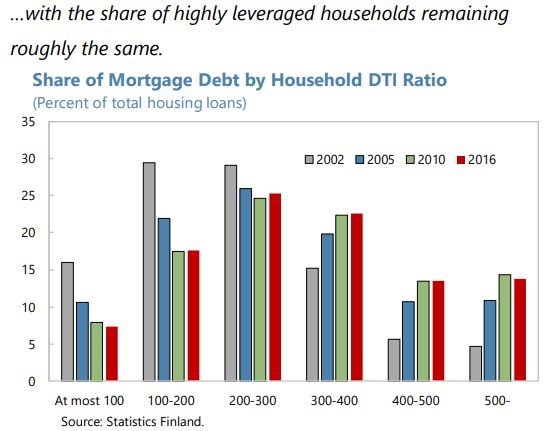

institutions easing lending standards and a rapid increase in non-bank lending. The expansion has been associated with an increase in payment defaults.Household debt has been increasing steadily, despite the increase in real disposable incomes. Saving rates are lower than peers, although some of the difference is attributable to Finland’s public pension system. Household debt remains lower than Nordic peers, but is expected to increase further. Highly-indebted households (i.e. those with debt greater than four times their income) accounted for over a quarter of borrowing in 2016; preliminary survey data for 2017 indicate that the typical new borrower for housing purchases is taking on leverage of 4½ times income. The share of floating rate loans in household lending is high, exacerbating households’ vulnerabilities to interest rate and/or income shocks, although this is mitigated by the prevalence of mortgages with annuity repayments.

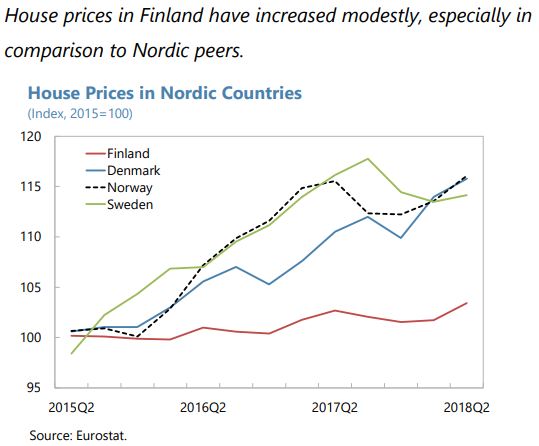

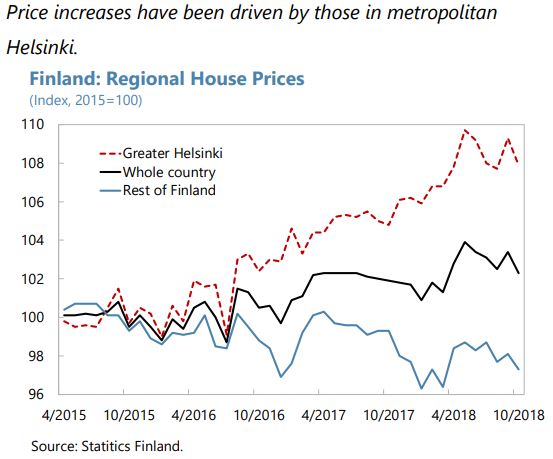

Residential real estate markets do not seem overheated overall, but demand still exceeds supply in major metropolitan areas, and commercial real estate may expose the economy to shocks. Housing starts and completions have been elevated, but price increases in greater Helsinki suggest demand still outstrips supply. Across the whole country, house price increases have been modest, especially in comparison to Nordic peers, with house price deflation in regions outside greater Helsinki. Price-to-income and price-to-rent ratios have not risen much during the recent economic recovery. Low and declining yields in commercial real estate suggest relatively high valuations.

The authorities have tightened credit policies. A floor of 15 percent on the average risk weight for housing loans took effect in January for institutions using internal risk-based (IRB) models. Effective July, the maximum loan-to-collateral (LTC) ratio for housing loans (excluding loans on first homes) was cut from 90 to 85 percent.

The recent tightening is appropriate, but policy could be more effective if the toolkit were modified. Although overall household debt and leverage are not high in comparison with other Nordic countries, there are some cohorts that are increasingly vulnerable to income and/or interest rate shocks—which, in view of the concentration of total lending in real estate, opens the financial system to risks.

The current cap on mortgage loans relative to collateral could usefully be replaced with a cap relative to the value of the property, as is common in other countries. And because the

underlying problem is more the level of debt than housing valuations, it would be useful for the authorities to have debt-based macroprudential tools (such as debt-to-income or debt-service to-income caps) at their disposal should leverage become more stretched. Applying such tools well depends on accurate information. Staff supports the recent Justice Ministry recommendation for the establishment of a “positive credit register”—i.e. a database that credit firms and the FINFSA could use to obtain real-time information about customers’ debt and income levels. A new challenge arises from non-bank lending, including online platforms such as peer-to-peer lending, which is not being recorded in credit statistics and registers.The growing reliance on consumer credit, especially that provided by non-banks and via digital platforms, raises additional concerns. Some of these outlets are not regulated and provide cross border financing. Attempts were made to circumvent legally-binding interest rate caps, raising the question of whether borrowers—especially those dealing with non-bank lenders—are sufficiently informed about the conditions of their loans. The authorities are amending the legislation on interest rate caps to close loopholes. Additional consumer protection measures are needed and require more data collection, especially on consumer lending provided through digital platforms. Tighter prudential requirements to demonstrate creditworthiness could also be considered.

Macroprudential authority tools should not be expected to solve underlying supply problems. The authorities have already implemented measures to expand housing supply in urban areas, including Helsinki. The government provides considerable support for social housing, which should make it easier to move across regions. But property taxation could be deterring mobility: recurrent property taxes collected by municipalities tend to be low, with some exceptions, while transaction tax rates are steeper at 4 percent.”

The IMF’s latest report on Finland says:

“Credit has expanded moderately overall, but housing corporation loans and consumer credit have been rising more rapidly. Total loan growth to the private nonfinancial sector has remained broadly constant at around 3½ percent for the past five years. Most lending to households has been in the form of secured lending for housing, which has grown around 4 percent. Corporate loan growth has rebounded strongly in the second quarter of the year after a sharp contraction in the second half of 2017.

Posted by at 10:56 AM

Labels: Global Housing Watch

Tuesday, January 15, 2019

The Key to Gentrification

From EconoSpeak:

“In the world of urban politics, there is probably no more potent populist rallying cry than the demand to halt gentrification. Activists have fought it on multiple fronts: zoning, development subsidies, permitting, rent control—every lever housing policies afford. But what if they’re mistaking cause for effect, hacking away at the visible manifestations of the problem while leaving the problem itself intact?

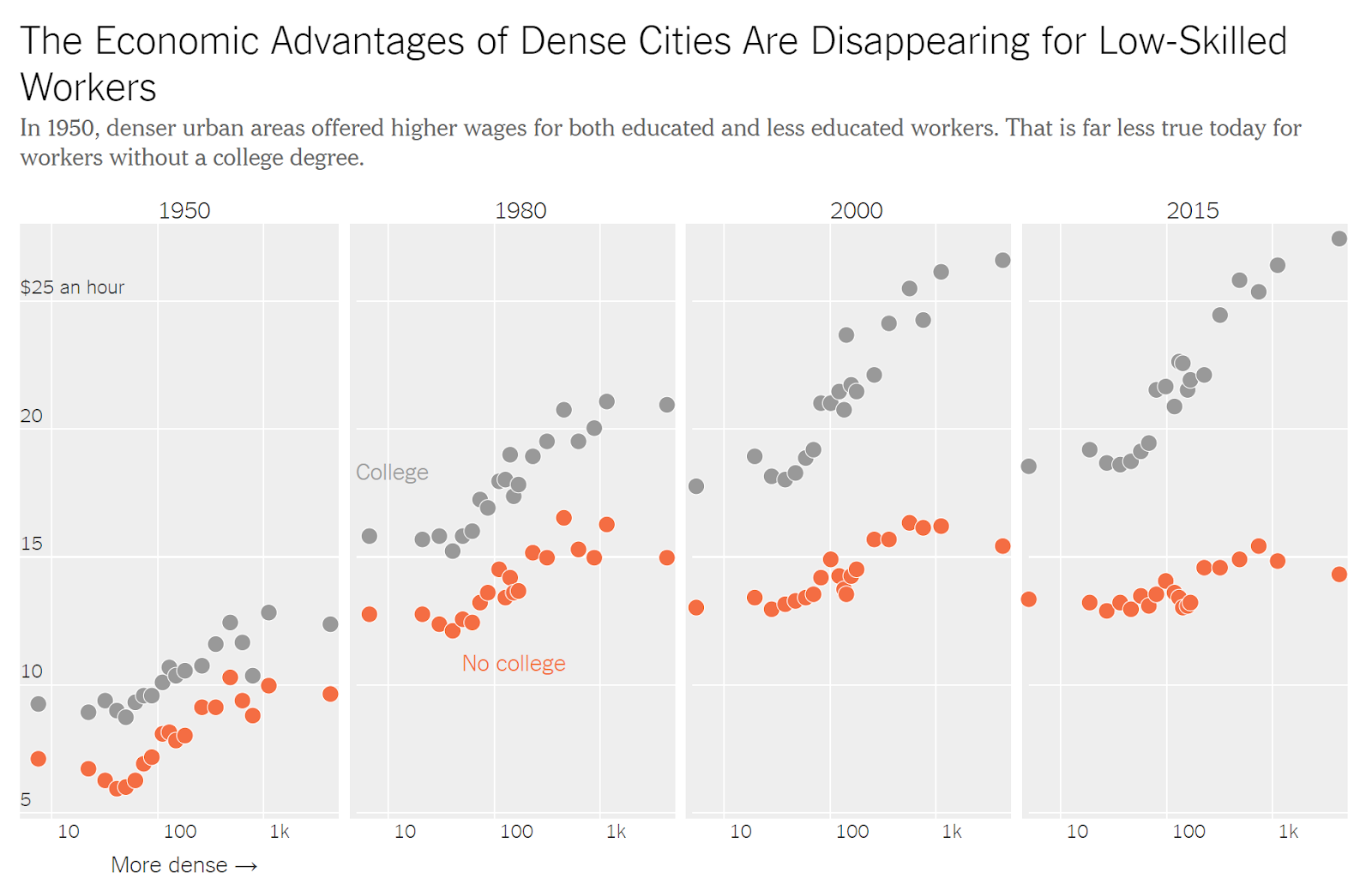

Pivot to an important article in today’s New York Times, reporting on recent research David Autor of MIT presented at the economics meetings in Atlanta earlier this month. It’s all summed up in this set of charts:

As you can see from the tiny print at the top, the data are being read horizontally within each chart, from less dense regions (rural areas) on the left to high density cities on the right. The question being asked in the article is, if you live in a rural area or a small town, how much benefit can you get from moving to a big city? In the early post-WWII period, the answer was “a lot” for both the majority holding only a high school diploma and the few with a college BA. By 2015 the situation had changed: it was still a good move for college grads but there was little to be gained by those with only a high school education—and probably even less when you factor in the increased cost of living. That’s an interesting story.

But there’s another way to read these charts, vertically, comparing wage gaps at any particular time and place between these two education-defined groups. In 1950 the gap was relatively small; in the densest cities the college crowd made about 30% more per hour than the high schoolers. By 2015 they made almost twice as much. And don’t forget that the rise of inequality is virtually fractal: similar gaps have opened up within the top 20%, and within the top 5%, 1% and .01%. The whole rightward tail of the distribution has elongated, pulling ever further from the median.”

Continue reading here.

From EconoSpeak:

“In the world of urban politics, there is probably no more potent populist rallying cry than the demand to halt gentrification. Activists have fought it on multiple fronts: zoning, development subsidies, permitting, rent control—every lever housing policies afford. But what if they’re mistaking cause for effect, hacking away at the visible manifestations of the problem while leaving the problem itself intact?

Pivot to an important article in today’s New York Times,

Posted by at 10:46 AM

Labels: Global Housing Watch, Inclusive Growth

Friday, January 11, 2019

Housing View – January 11, 2019

On the US:

- Housing finance issues to watch in 2019 – Urban Institute

- Experts weigh in on housing reform at House hearing – Housing Wire

- The Price of Residential Land for Counties, ZIP codes, and Census Tracts in the United States – Federal Housing Finance Agency

- Leaving Households Behind: Institutional Investors and the U.S. Housing Recovery – Federal Reserve Bank of Philadelphia

- Real-estate agents say government shutdown is impacting the housing market – MarketWatch

- Chinese buyers expand their reach in the US housing market as the middle class gets in on the act – CNBC

- What actions can policymakers take to avert the brewing national housing crisis? – Washington Post

- 2018 Roundup: Our Most Popular Blogs of the Year – Harvard Joint Center for Housing Studies

- Appraising Home Purchase Appraisals – Federal Reserve Bank of Philadelphia

- California Housing Development Is A ‘Disaster Waiting To Happen’ – NPR

- Is Housing the Business Cycle, 2019? – Econbrowser

- Elizabeth Warren’s Housing Crisis Plan Hints at Reparations – Citylab

- Substance Use Disorder Treatment Centers and Property Values – NBER

- Affordable homes or investment assets? – Washington Post

- The American Dream Isn’t for Black Millennials – New York Times

- Rich Cities Created the Housing Shortage – Wall Street Journal

- Housing Confidence Down as More Americans Believe It’s a Bad Time to Buy a Home – Fannie Mae

- It’s a Wonderful Loan: A Short History of Building and Loan Associations – Federal Reserve Bank of Richmond

- See How Landlords Pack Section 8 Renters Into Poorer Neighborhoods – Citylab

- As Fewer Young Adults Wed, Married Couples’ Wealth Surpasses Others’ – Federal Reserve Bank of St. Louis

- America’s Housing Crisis Could Imperil Trump’s Presidency – Citylab

- Survey: First Home Nightmares – Porch

- US housing market uncertainty prompts Lennar to scrap guidance – Financial Times

On other countries:

- [Australia] Australia’s house price slide prompts worries about economy – Financial Times

- [Canada] What happened when Vancouver residents built new homes in their backyards – Financial Times

- [China] China house price gains no longer a certainty: central bank adviser – Reuters

- [China] Empty Homes and Protests: China’s Property Market Strains the World – New York Times

- [China] China warns cities to cut reliance on property, developers’ shares fall – Reuters

- [Netherlands] Amsterdam Houses Head for Record Prices – Bloomberg

- [New Zealand] New Zealand’s house prices are rising again – Global Property Guide

- [Slovak Republic] Slovak Republic’s house price rises slowing – Global Property Guide

- [United Kingdom] Cheer up, millennials! It will become easier to buy a house – Economist

Photo by Aliis Sinisalu

On the US:

- Housing finance issues to watch in 2019 – Urban Institute

- Experts weigh in on housing reform at House hearing – Housing Wire

- The Price of Residential Land for Counties, ZIP codes, and Census Tracts in the United States – Federal Housing Finance Agency

- Leaving Households Behind: Institutional Investors and the U.S. Housing Recovery – Federal Reserve Bank of Philadelphia

- Real-estate agents say government shutdown is impacting the housing market – MarketWatch

- Chinese buyers expand their reach in the US housing market as the middle class gets in on the act – CNBC

- What actions can policymakers take to avert the brewing national housing crisis?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 3, 2019

Housing View – January 3, 2019 [2019 AEA Annual Meeting Special Edition]

Below is a preliminary list of papers that will presented at this year’s AEA Annual Meeting on January 4-6 in Atlanta, Georgia.

On housing and cycles

- Is Housing the Business Cycle? A Multi-resolution Analysis for OECD Countries – Paper

- The First Housing Bubble? Prices and Turnover in Amsterdam, 1582-1810 – Paper

- Residential Investment and Recession Predictability – Paper

- Residential House Prices, Commercial Real Estate and Bank Failures – Paper and Presentation

- Perception of House Price Risk and Homeownership – Paper

- The Effects of Local Risk on Homeownership – Paper and Presentation

- What Drove the 2003-2006 House Price Boom and Subsequent Collapse? Disentangling Competing Explanations – Paper

- Expectations During the U.S. Housing Boom: Inferring Beliefs from Actions – Paper

- The Housing Boom and Bust: Model Meets Evidence – AEA

- Spatial Estimates of Bubbles: Tokyo House Prices and Rents – AEA

On housing and mortgage

- Brokerage Choice, Dual Agency and Housing Market Strength – Paper

- Villains or Scapegoats? The Role of Subprime Borrowers in Driving the U.S. Housing Boom – Paper

- Financial Fragility with SAM? – Paper

- Structuring Mortgages for Macroeconomic Stability – Paper

- A Crisis of Missed Opportunities? Foreclosure Costs and Mortgage Modification During the Great Recession – Paper

- Mortgage Design and Slow Recoveries: The Role of Recourse and Default – Paper

- Correlation in Mortgage Defaults – Paper

- State Dependency and the Efficacy of Monetary Policy: The Refinancing Channel – Paper

- No Job, No Money, No Refi: Frictions to Refinancing in a Recession – Paper

- Mortgage Losses: Loss on Sale and Holding Costs – Paper and Presentation

- Can Lending Restrictions on “Exotic” Lending Dampen Housing Price Volatility? A Panel VAR Exploration – AEA

- Mortgage Design and Housing Market – AEA

- House Price Markups and Mortgage Defaults – AEA

- Will Housing Mortgagors Increase Their Consumptions after Paying off Loans?-Evidence from Urban China – AEA

- Home Equity Withdrawal via Credit Card Borrowing-Micro Evidence from China – AEA

- Rental Markets and the Effect of Credit Conditions on House Prices – Paper

- Mortgage Lending: Evidence from a Correspondence Field Experiment – AEA

- Fueling the Credit Crisis – AEA

- Strategic or Illiquid Mortgage Default? Evidence from Household Bank Account Data– AEA

- The Impact of Liquidity Regulation on Bank Mortgage Lending – AEA

- How Is Financial Literacy Important in Mortgage Market? Different Evidence from Urban China – AEA

- The Impact of Repossession Risk on Mortgage Default – AEA

- Mortgage Prepayment and Path-Dependent Effects of Monetary Policy – AEA

- Mortgage Finance Development Across the World – AEA

On housing policy

- Mortgage Debt, Hand-to-Mouth Households, and the Monetary Policy Transmission – Presentation

- Heterogeneous Spillovers Of Housing Credit Policy – Paper

- The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco – Paper

- The Effect of Tax Reform on Tax Liabilities of Owners and Renters – Paper

- Intermediated Credit Supply and Endogenous Household Leverage Constraints – Paper

- Real Estate Asset Bubbles and Monetary Policy: The Channel between Central Bank’s Balance Sheet and Firms’ Balance Sheets – Paper

- Tax Reform, Homeownership Costs, and House Prices – Paper

- The Effect of Government Mortgage Guarantees on Homeownership – Paper

- Loan to Value Limits and House Prices – AEA

- Empirics on the Causal Effects of Rent Control in Germany – AEA

- An Urban Equilibrium Model with Rent Controls Applied to Paris Urban Area – AEA

- Monetary Policy, Heterogeneity, and the Housing Channel – AEA

- Can Lending Restrictions on “Exotic” Lending Dampen Housing Price Volatility? A Panel VAR Exploration – AEA

- Mortgage Pricing and Monetary Policy – AEA

On housing supply

- Fewer players, fewer homes: concentration and the new dynamics of housing supply – Paper and Presentation

- What’s Lost in the Aggregate: Lessons from a Local Index of Housing Supply Elasticities – Paper

- New Construction and Mortgage Default – Paper and Presentation

- Spatial Misallocation in Chinese Housing and Land Markets – AEA

On housing affordability

- Targeting In-Kind Transfers Through Market Design: A Revealed Preference Analysis of Public Housing Allocation – Paper

- Affordable Housing and City Welfare – Paper

- Political Control of the State Legislature and Municipal Bond Financing for Affordable Housing – Paper

- Waiting Lists, Lotteries and Public Housing: Natural Experiment Evidence from Amsterdam – Paper

- Affordable Housing in Westchester County – Paper

- How (Not) to Allocate Affordable Housing – AEA

- The Public-Housing Allocation Problem: Theory and Evidence from Pittsburgh – AEA

- Not In My Neighbor’s Back Yard? Laneway Homes and Neighbors’ Property Values – AEA

- Does Affordable Housing Participation Reduce Default and Prepayment? The Case for the Montgomery County MPDU Program – AEA

On housing and evictions

- Does Eviction Cause Poverty? Quasi-experimental Evidence from Cook County, IL – Paper

- The Effect of Residential Evictions on Low-Income Adults – AEA

- Health Insurance and Housing Stability: The Effect of Medicaid Expansion on Evictions – AEA

On housing, investors, and speculation

- Out-of-Town Home Buyers and City Welfare – Paper

- Economic Consequences of Housing Speculation – Paper

- Speculative Dynamics of Prices and Volume – Paper

- Expectations During the U.S. Housing Boom: Inferring Beliefs from Actions – Paper

- Speculative Asset Bubbles: The Primary Drivers of “Systemic” Banking Crises in Post-war Advanced Economies – Presentation

- Buying Up Elm Street: Institutional Investors and the Housing Recovery – AEA

- Speculating on Superstition: Evidence from Housing Transactions in Hungry Ghost Months in Singapore – AEA

On housing and the sharing economy

- Which Neighborhood Joins the Sharing Economy and Why? – The Case of the Short-term Rental Market in New York City – Paper

- Cash to Spend: Credit Constraints, IPO Lockups, and House Prices – Paper

- Can Landlords be Paid to Stop Avoiding Voucher Tenants? – Paper

On housing, the environment, and natural disasters

- Toxic Assets: How the Housing Market Responds to Environmental Information Shocks – Paper

- Aircraft Noise Pollution, Soundproofing, and Lagging House Price Adjustments: Evidence from the Minneapolis-St. Paul International Airport – Paper

- Natural Disasters and Housing Markets: The Tenure Choice Channel – Paper

On housing and transportation

- Commuting, Labor and Housing Market Effects of Mass Transportation: Welfare and Identification – Paper and Presentation

- International Travel Costs and Local Housing Markets – Paper

On housing and everything else

- Getting High or Getting Low? – Paper

- Allocation of Education, School District Policy and Housing Market Efficiency – Presentation

- Why Are Housing Demand Curves Upward Sloping? – Paper and Presentation

- The Cross-Section of Expected Housing Returns – Paper

- Amenity Migration within a Millennial City Evidence from Washington DC Tax Data, 2005-2014 – Paper and Presentation

- Getting More by Asking for Less? – Paper

- Magnification of the ‘China Shock’ Through the United States Housing Market – Paper and Presentation

- Valuing Housing Services in the Era of Big Data: A User Cost Approach Leveraging Zillow Microdata – Paper

- The Propagation of Regional Shocks in Housing Markets: Evidence from Oil Price Shocks in Canada – Paper

- Housing Wealth, Health and Deaths of Despair – Paper

- What Happens After You Overpay for Your House – Paper and Presentation

- When Birth or Death Hits Home: House Prices, Rents and Demography in Paris and Amsterdam, 1400-present – Presentation

- Residential House Prices, Commercial Real Estate and Bank Failures – Paper and Presentation

- Perception of House Price Risk and Homeownership – Paper

- Attitudes Toward and Perceptions of the Ambiguity of House and Stock Prices – Paper

- Housing Wealth and Consumption: New Evidence from Household-Level Panel Data – AEA

- Sorting or Steering: Experimental Evidence on the Economic Effects of Housing Discrimination and Its Consequences for Environmental Justice – AEA

- Real Estate News and REIT Returns – AEA

- The Impact of Housing Quality on Health and Labor Market Outcomes: The German Reunification – AEA

- Sexual Orientation, Gender, Pregnancy, and Family Composition Discrimination in Machine Learning, Building Vintage and Property Values – AEA

- The Impacts of Racial Discrimination on Housing Choice and Welfare in the United States – AEA

- House Prices, Migration, and the Evolution of the Wealth Distribution – AEA

*AEA indicates that neither the paper or presentation is available at the moment.

**This post has been updated on January 5 to add missing papers, and to add links to presentations and papers to existing papers.

Below is a preliminary list of papers that will presented at this year’s AEA Annual Meeting on January 4-6 in Atlanta, Georgia.

On housing and cycles

Posted by at 10:42 AM

Labels: Global Housing Watch

Friday, December 28, 2018

Housing Market in Bolivia

The IMF’s latest report on Bolivia says:

“Credit quotas should be relaxed to limit poor-quality credit growth. Interest caps should also be removed so that lending decisions better reflect intrinsic risks. This would remove distortions in the allocation of credit and support desirable allocation of resources in support of growth. ASFI is urged to monitor closely capital quality for its ability to absorb potential shocks and to scrutinize possible risks arising from rapid credit growth to housing. In this context, the Fund welcomes the opportunity to assist the authorities to prepare a real estate price index and urges rapid progress.”

The IMF’s latest report on Bolivia says:

“Credit quotas should be relaxed to limit poor-quality credit growth. Interest caps should also be removed so that lending decisions better reflect intrinsic risks. This would remove distortions in the allocation of credit and support desirable allocation of resources in support of growth. ASFI is urged to monitor closely capital quality for its ability to absorb potential shocks and to scrutinize possible risks arising from rapid credit growth to housing.

Posted by at 10:15 AM

Labels: Global Housing Watch

Subscribe to: Posts