Showing posts with label Global Housing Watch. Show all posts

Wednesday, February 27, 2019

Macro Aspects of Housing

From a paper by Charles Ka Yui Leung and Joe Cho Yiu Ng:

“This paper aims to achieve two objectives. First, we demonstrate that with respect to business cycle frequency (Burns and Mitchell, 1946), there was a general decrease in the association between macroeconomic variables (MV) and housing market variables (HMV) following the global financial crisis (GFC). However, there are macro-finance variables that exhibited a strong association with the HMV following the GFC. For the medium-term business cycle frequency (Comin and Gertler, 2006), we find that while some correlations exhibit the same change as the business cycle counterparts, others do not. These “new stylized facts” suggest that a reconsideration and refinement of existing “macro-housing” theories would be appropriate. We also provide a review of the recent literature, which may enhance our understanding of the evolving macro-housing-finance linkage.”

From a paper by Charles Ka Yui Leung and Joe Cho Yiu Ng:

“This paper aims to achieve two objectives. First, we demonstrate that with respect to business cycle frequency (Burns and Mitchell, 1946), there was a general decrease in the association between macroeconomic variables (MV) and housing market variables (HMV) following the global financial crisis (GFC). However, there are macro-finance variables that exhibited a strong association with the HMV following the GFC.

Posted by at 10:13 AM

Labels: Global Housing Watch

Friday, February 22, 2019

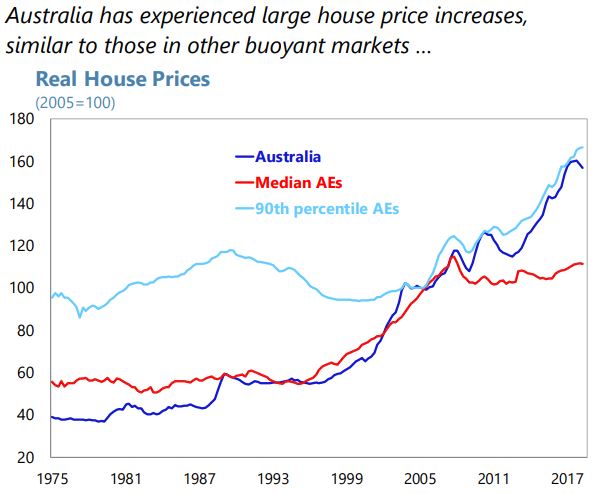

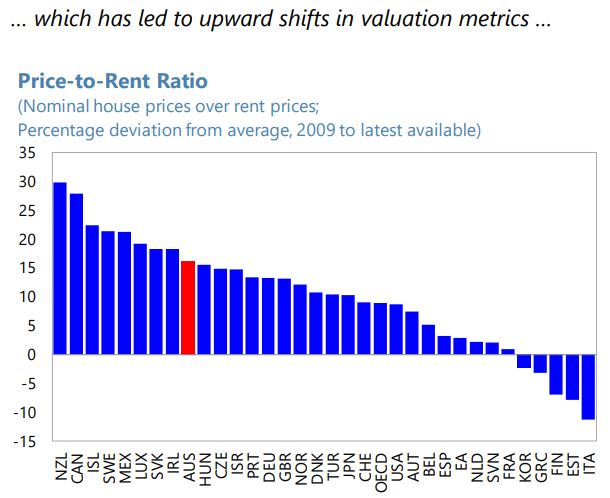

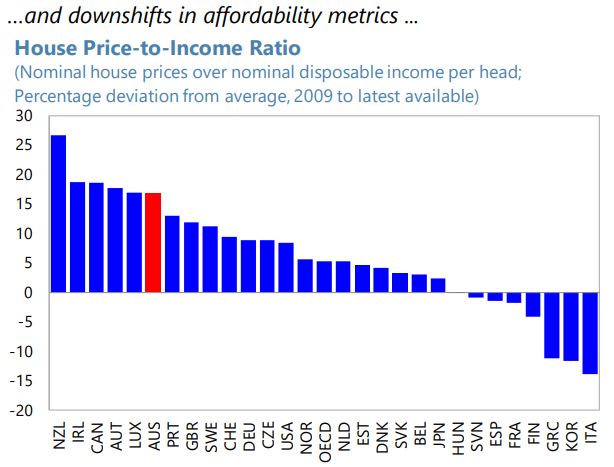

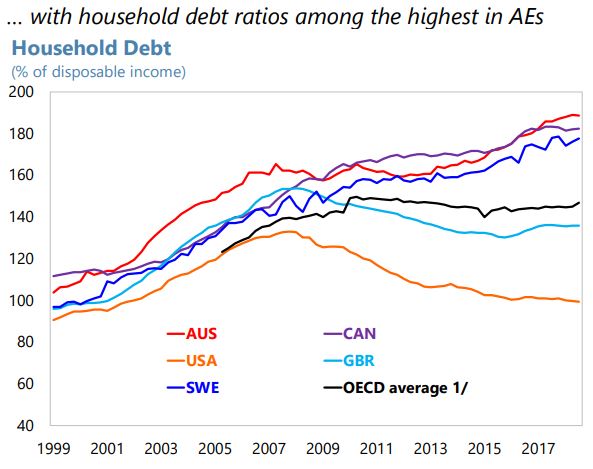

Housing Market in Australia

From the IMF’s latest report on Australia:

“The housing market correction is helping housing affordability. Foreign and domestic investor demand has moderated, thereby enhancing opportunities for first-time home buyers and purchases by owner-occupiers more broadly. On the supply side, progress has been made in using City Deals, agreements across all levels of government that integrate planning and infrastructure delivery for new developments and redevelopments. A prominent example―the City Deal for western Sydney―encompasses the development of the urban area around the new airport. Two states (Western Australia and Tasmania) introduced or announced housing-related tax policy measures discriminating between residents and non-residents since the last Article IV Consultation.

Housing supply reforms will remain critical to restoring housing affordability. While the housing market correction will help, it is unlikely to be sufficient for inclusive, broad-based affordability and growth. The underlying demand for housing is widely expected to remain strong with a robust economic growth outlook for and high population growth in urban areas. At the same time, broad affordability will also be a precondition for a significant reduction in related macro-financial vulnerabilities. As planning, zoning, and other reforms affect supply and prices with long lags, housing supply reforms should, therefore, not be delayed because of the housing market correction. City Deals are a useful catalyst for the large-scale development or redevelopment of urban areas. Nevertheless, this instrument has limited reach, although the Regional Deals envisaged by the government would provide for a welcome extension. Some states should still take the opportunity for further streamlining and consolidation in planning and zoning regulation.

Broader tax reforms that also address housing and land use would reinforce the impact of supply-side measures. Stamp duties should be replaced by broader land taxes, which would strengthen incentives for efficient land use. Within the context of a broader tax reform, gradual lowering of capital gains discounts and limits on negative gearing for investors would reduce structural incentives for leveraged investment by households, including in residential real estate. A more limited capital gains tax exemption for owner-occupiers should also be considered.

The housing policy measures discriminating nonresident buyers should be reconsidered. As the role of foreign buyers in residential real estate markets has started to decline, the discriminatory measures should be reconsidered, as they may no longer be needed to address housing market imbalances. They should be replaced by alternative and effective non-discriminatory measures where possible (e.g., a general surcharge on all vacant property).

The state governments of New South Wales and Victoria noted that the fall in housing prices in Sydney and Melbourne was larger than originally projected in their budgets. Nevertheless, despite their limited progress on zoning and planning reform to reduce impediments to housing supply and affordability, they expected house prices to find support from both housing demand and supply factors. The authorities highlighted that City Deals could be important tools to foster urban housing supply. City Deals have allowed all levels of government to coordinate planning and construction decisions, thereby facilitating infrastructure provision which can in turn support housing supply expansion. Deals agreed on or announced in 2018 included Darwin, Geelong, Hobart, and Perth. There are also plans underway to pilot Regional Deals outside of the major urban areas.”

From the IMF’s latest report on Australia:

“The housing market correction is helping housing affordability. Foreign and domestic investor demand has moderated, thereby enhancing opportunities for first-time home buyers and purchases by owner-occupiers more broadly. On the supply side, progress has been made in using City Deals, agreements across all levels of government that integrate planning and infrastructure delivery for new developments and redevelopments. A prominent example―the City Deal for western Sydney―encompasses the development of the urban area around the new airport.

Posted by at 10:59 AM

Labels: Global Housing Watch

Housing View – February 22, 2019

On cross-country:

- Peter Praet: On the importance of real estate statistics – European Central Bank

On the US:

- Housing Is Already in a Slump. So It (Probably) Can’t Cause a Recession. – New York Times

- Despite contrary claims, African-Americans believe in the American dream — even millennials – American Enterprise Institute

- Oregon’s Rent Control Bill Would Ultimately Please Nobody – Cato Institute

- HUD Funding Bill Will Launch Housing Voucher Mobility Demonstration – Center on Budget and Policy Priorities

- Housing investment, sea level rise, and climate change beliefs – Economic Letters

- “Debtless” Housing Boom Leads Household Wealth Recovery – Federal Reserve Bank of St. Louis

- A Red-State Take on a YIMBY Housing Bill – Citylab

- Why Unions Must Bargain for Affordable Housing—and How – American Prospect

- Without Amazon HQ2, What Happens to Housing in Queens? – Citylab

- The Super Bowl: Key Housing Indicator – NPR

- Yet another sign from the housing market of a looming recession – HousingWire

- A Shortage of Short Sales: Explaining the Underutilization of a Foreclosure Alternative – Federal Reserve Bank of Philadelphia

- Recession not likely before 2021, housing economists say – The Orange County Register

- The Federal Shutdown Damaged Housing Voucher Programs – American Prospect

On other countries:

- [Australia] The Housing Slump Down Under Is Getting Serious – Bloomberg

- [Canada] Montreal’s Real-Estate Market Is About to Eclipse Vancouver’s – Bloomberg

- [China] The Effect of a Subway on House Prices: Evidence from Shanghai – Real Estate Economics

- [China] China Property ‘Stealth Easing’ Spreads in Boost to Home Prices – Bloomberg

- [Greece] Greece to Subsidize Mortgage Payments to Tackle Bad Loan Crisis – Bloomberg

- [China] China developers snap up distressed real estate debt – Financial Times

- [Greece] Athens property boom: Greeks left out as prices rise – BBC

- [Hong Kong] The Hong Kong property bubble that won’t burst – Financial Times

- [United Kingdom] Research reveals who made the most money from UK property – Financial Times

On cross-country:

- Peter Praet: On the importance of real estate statistics – European Central Bank

On the US:

- Housing Is Already in a Slump. So It (Probably) Can’t Cause a Recession. – New York Times

- Despite contrary claims, African-Americans believe in the American dream — even millennials – American Enterprise Institute

- Oregon’s Rent Control Bill Would Ultimately Please Nobody – Cato Institute

- HUD Funding Bill Will Launch Housing Voucher Mobility Demonstration – Center on Budget and Policy Priorities

- Housing investment,

Posted by at 5:14 AM

Labels: Global Housing Watch

Tuesday, February 19, 2019

Housing Market in Slovenia

From the IMF’s latest report on Slovenia:

“Housing prices have completed their recovery from the deep slump during the double-dip crisis (2008–14) and continue to grow robustly, but current valuations do not point to overheating. The authorities have adopted macroprudential policy tools preemptively and continue to monitor developments. Easing supply constraints on the housing market could help to moderate future price increases.

Residential real estate prices rose at their fastest pace in 2017 since the outbreak of the crisis, recording the third highest rate in the euro area and a record number of transaction. Prices of used apartments in Ljubljana increased by 14.8 percent during 2017, compared to the national average increase of 11.8 percent. The overall housing price index rose 13.4 percent during the year to 2018: Q2.

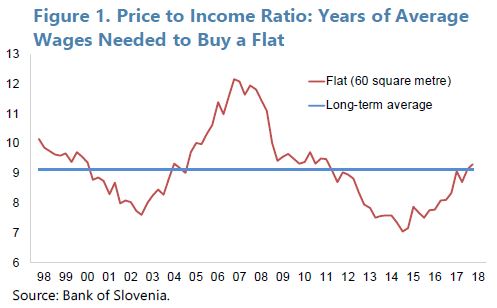

Housing remains affordable in historical and international comparison, and further appreciation in real house prices is likely. Wages and disposable incomes have increased since 2008, while real estate prices have only just reached their pre-crisis level. By some measures, the ratio of real estate prices to incomes stood at their long-term average in 2018 (Figure 1). At 54.4 percent, Slovenia has the second-lowest urbanization rate in the EU. Continued urbanization and growth in household incomes are expected to fuel continued appreciation of real estate prices.

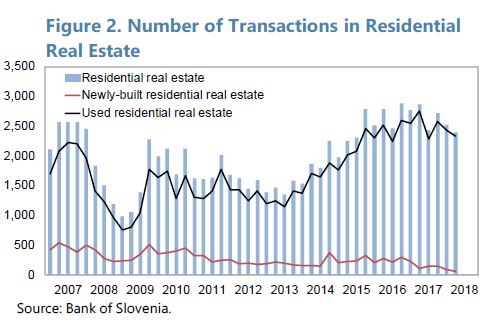

The supply of new residential housing has failed to keep pace with demand. The stock of housing in Slovenia is low by regional standards with 410 units per 1000 residents (compared to 547 in Austria and 524 in Croatia). The number of residential real estate transactions has been rising after 2013, yet the sales of newly-built units has dropped further from very low levels (Figure 2). The lack of supply response is related to the bankruptcy of major construction companies during the crisis years, the reluctance of banks to finance new construction, and constraints placed on new construction by urban planning and regulation.

Mortgage financing is not a significant driver of housing price developments. Slovenia has a comparatively high level of owner-occupied housing (77 percent of households, compared to 60 percent in the euro area, but comparable to other CEE countries). Only about 10 percent of households have a mortgage (19 percent in the euro area), and about a third of recent housing transactions was carried out with equity (i.e., without bank financing). The growth in mortgage lending has been positive since 2013, nearly reaching 5 percent year-on-year in 2017, but has since fallen back to below 4 percent.

The BoS has adopted macro-prudential policy tools as a preemptive step. Current data do not point to an overheating housing market or exposure by the banking sector. However, continued price increases and the inflexible supply response suggest the need for close monitoring. Guidance to banks on loan-to-value and DSTI ratios related to residential real estate transactions and a countercyclical capital buffer were implemented in 2016. In 2018, the applicability of the ratios was expanded to include not only mortgages but all household debt, prompted by rapidly growing consumer lending (albeit from a low level). Early adoption of the tools affords the banking sector time to adjust and monitor lending practices accordingly.

The government seeks to improve the supply of social housing. In 2015, Slovenia adopted its National Housing Program 2015–25 which calls for a new rental policy and an increase in social housing stock for the benefit of vulnerable groups, including young families and the elderly. The National Housing Fund, currently financing social housing investments by municipalities, could become a direct supplier, alleviating shortages of affordable housing.

Urban planning practices could be reformed to ease the supply of new housing. Zoning restrictions and the effort and time required to obtain all required permits before starting new construction projects impede the market response to rising house prices. Regulatory reform could therefore help to increase supply and slow the increases in real estate prices and rents.”

From the IMF’s latest report on Slovenia:

“Housing prices have completed their recovery from the deep slump during the double-dip crisis (2008–14) and continue to grow robustly, but current valuations do not point to overheating. The authorities have adopted macroprudential policy tools preemptively and continue to monitor developments. Easing supply constraints on the housing market could help to moderate future price increases.

Residential real estate prices rose at their fastest pace in 2017 since the outbreak of the crisis,

Posted by at 3:28 PM

Labels: Global Housing Watch

Housing Market in Nepal

From the IMF’s latest report on Nepal:

“Existing macroprudential measures, including the loan-to-value ratios on car loans and residential real estate, and limits on real estate sector exposure have helped to contain credit growth, but need to be tightened further. Staff welcomes the authorities’ stated intention to

adhere to the ceiling on the loan-to-deposit (LTD) ratio—so-called credit-to-core capital cum deposit (CCD) ratio.2 Several carve-outs have been introduced over time to provide more room for credit growth. These carve-outs, including the recent decision to allow funds obtained through interbank borrowing to count as deposits, should be phased out and the authorities should resist banks’ pressures for further effective relaxation of the CCD ratio and other macroprudential rules.”

From the IMF’s latest report on Nepal:

“Existing macroprudential measures, including the loan-to-value ratios on car loans and residential real estate, and limits on real estate sector exposure have helped to contain credit growth, but need to be tightened further. Staff welcomes the authorities’ stated intention to

adhere to the ceiling on the loan-to-deposit (LTD) ratio—so-called credit-to-core capital cum deposit (CCD) ratio.2 Several carve-outs have been introduced over time to provide more room for credit growth.

Posted by at 3:23 PM

Labels: Global Housing Watch

Subscribe to: Posts