Showing posts with label Global Housing Watch. Show all posts

Friday, April 19, 2019

Housing View – April 19, 2019

On cross-country:

- “The housing affordability gap is equivalent to 1% of global GDP” – Housing Europe

- Residential investment opportunities in Africa – which sectors are on the rise? – Knight Frank

- The Economic Defense of Sprawl (And What’s Wrong With It) – Planetizen

- Connecting commodities to house price booms – Financial Times

On the US:

- The Democratic coalition is split over housing costs in cities – The Economist

- When’s the Next Housing Crisis? – Wall Street Journal

- The Danger in Using Monetary Policy to Address Housing Affordability: A Lesson from the Great Recession – George Mason University

- Why Rent Control Isn’t An Affordable Housing Solution – Forbes

- The Sustainability of First-Time Homeownership – Federal Reserve Bank of New York

- Housing Finance Reform: First Do No Harm – Wall Street Journal

- The Next Housing Boom Looks More Sustainable – Bloomberg

- Silicon Valley Housing Crisis Ensnares Stanford – Wall Street Journal

- West Coast Homebuyers Get One Benefit From Sales Slowdown – Bloomberg

- Research: When Airbnb Listings in a City Increase, So Do Rent Prices – Harvard Business Review

- Seattle takes a small step against gentrification – Los Angeles Times

- Below-Average Growth in Home Remodeling Expected by 2020 – Harvard Joint Center for Housing Studies

On other countries:

- [Canada] China’s Property Market Is Feeling the Stimulus Effect – Bloomberg

- [China] Housing Policy and Economic Growth in China – Reserve Bank of Australia

- [China] Building a Case For Chinese Property – Wall Street Journal

- [China] Shenzhen joins top five cities with most expensive housing – Financial Times

- [Egypt] Egypt’s house prices falling sharply – Global Property Guide

- [Germany] A referendum to expropriate apartments from big landlords in Berlin – The Economist

- [Germany] Berlin Housing Backlash Spurs Drive to Nationalize Real Estate – Bloomberg

- [Germany] In Berlin, rising rents fuel a movement urging city government to buy back apartments – Los Angels Times

- [Germany] Capital Flows, Real Estate, and City Cycles: Micro Evidence from the German Boom – Deutsche Bundesbank

- [Hungary] Hungary prepares rate fixing plan for $3.16 bln mortgage stock – Reuters

- [Ireland] Brexit Jobs Spur Dublin Real Estate Boom – Bloomberg

- [United Arab Emirates] UAE’s property prices fall further – Global Property Guide

- [United Kingdom] Council housing is making a comeback in Britain – The Economist

- [United Kingdom] Landlords face curbs on evicting tenants at short notice – Financial Times

On cross-country:

- “The housing affordability gap is equivalent to 1% of global GDP” – Housing Europe

- Residential investment opportunities in Africa – which sectors are on the rise? – Knight Frank

- The Economic Defense of Sprawl (And What’s Wrong With It) – Planetizen

- Connecting commodities to house price booms – Financial Times

On the US:

- The Democratic coalition is split over housing costs in cities – The Economist

- When’s the Next Housing Crisis?

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, April 15, 2019

House Prices in Myanmar

From the IMF’s latest report on Myanmar:

“However, the near-term outlook has weakened. Economic growth is expected to remain below potential (…) in 2018/19 due to weakening export demand and subdued private construction activity related to the deleveraging by banks and corporates as real estate prices continue to correct from elevated levels.”

From the IMF’s latest report on Myanmar:

“However, the near-term outlook has weakened. Economic growth is expected to remain below potential (…) in 2018/19 due to weakening export demand and subdued private construction activity related to the deleveraging by banks and corporates as real estate prices continue to correct from elevated levels.”

Posted by at 9:50 AM

Labels: Global Housing Watch

Friday, April 12, 2019

Housing View – April 12, 2019

On cross-country:

- Residents’ revenge: how citizens are taking on city developers – Financial Times

- Global Residential Cities Index-Q4 2018 – Knight Frank

- Impact of weak substitution between owning and renting a dwelling on housing market – Journal of Housing and the Built Environment

- A new housing ecosystem: $3.8 trillion under one roof – McKinsey

On the US:

- The Coming Trump Housing Crisis – Wall Street Journal

- Young businesses are more vulnerable to housing market shocks – University of Chicago

- Netflix series hypes the Sunset Strip’s luxury real estate sizzle – Los Angeles Times

- Senate Confirms Trump Pick to Lead Housing-Finance Overhaul – Wall Street Journal

- The Political Battle Over California’s Suburban Dream – Citylab

- Housing Sentiment Surges Just in Time for Spring Homebuying Season – Fannie Mae

- Slowing U.S. Housing Sector Still Shaped by Great Recession – Federal Reserve Bank of St. Louis

- The Rise of the Radical Suburbs – Architect

- Chipping Away at the Mortgage Deduction – Wall Street Journal

On other countries:

- [Canada] Chinese Real-Estate Investors Wary of Vancouver Head to Toronto – Bloomberg

- [Canada] Canadian Home Building Rebounds From Deep Freeze: Housing Update – Bloomberg

- [China] China’s Easing of Residency Requirements Could Boost Cooling Property Market – Bloomberg

- [Czech Republic] Czech Republic’s housing structure – ING

- [Germany] Housing for the People – Jacobin

- [Hong Kong] Hong Kong plans to house 1 million people on artificial islands – World Economic Forum

- [Lithuania] Lithuania’s modest house price rises – Global Property Guide

- [Netherlands] ING: Expats and foreign students raise Amsterdam house prices – ING

- [Romania] Romania’s housing market cooling – Global Property Guide

- [Spain] Spain’s housing market continues to grow stronger – Global Property Guide

- [South Africa] Johannesburg’s hipster gentrification project is at risk of crumbling – Quartz

- [Sweden] Sweden’s house price boom is officially over – Global Property Guide

- [United Kingdom] Construction Sector: Modernisation and Sustainable Housing Supply – UK Parliament

- [United Kingdom] HBF Policy Conference 2019: ‘Confronting the housing crisis’, John Stewart memorial presentation – London School of Economics

On cross-country:

- Residents’ revenge: how citizens are taking on city developers – Financial Times

- Global Residential Cities Index-Q4 2018 – Knight Frank

- Impact of weak substitution between owning and renting a dwelling on housing market – Journal of Housing and the Built Environment

- A new housing ecosystem: $3.8 trillion under one roof – McKinsey

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, April 5, 2019

Housing View – April 5, 2019

On cross-country:

- Affordable Housing Crisis Spreads Throughout World – Wall Street Journal

- Film Director: Don’t Just Blame Gentrification for Housing Crisis – Wall Street Journal

- Mind the data gap: commercial property prices for policy – Bank for International Settlements

On the US:

- Bank Balance Sheets and Liquidation Values: Evidence from Real Estate Collateral – SSRN

- Expectations During the U.S. Housing Boom: Inferring Beliefs from Actions – NBER

- Banks’ Real Estate Exposure and Resilience – Federal Reserve Bank of San Francisco

- American Families Can’t Afford the Rent – Harvard Joint Center for Housing Studies

- San Francisco Fed Says Banks Could Weather a Big Hit to Housing – Bloomberg

- The Link Between Local Zoning Policy and Housing Affordability in America’s Cities – George Mason University

- Wall Street Puts the Squeeze on the Housing Market – Bloomberg

- California Home Prices Are So High, Even High-Income Households Can’t Keep Up – Zillow

- What’s Keeping Lower-Income Families from Homeownership? – Freddie Mac

- Are Planners Partly to Blame for Gentrification? – Citylab

- Mapping America’s Next Tech Hubs: A Look at Housing Market and Migration Trends in Atlanta, Austin, D.C. and Other Hot Destinations for Tech Companies – Redfin

- These Low-Income Communities Should Prepare for an Influx of Cash – Zillow

- Homebuying Startups Keep Raising Money in Softer Housing Market – Bloomberg

- Housing Prices, Supply, and Innovation – Cato Institute

- Upzoning Under SB 50: The Influence of Local Conditions on the Potential for New Supply – University of California, Berkeley

- The Neighborhoods Where Housing Costs Devour Budgets – Citylab

- Available Affordable Housing Is Down Across The State, Report Finds – wbur

- The Growing Shortage of Affordable Housing for the Extremely Low Income in Massachusetts – Federal Reserve Bank of Boston

On other countries:

- [Australia] What do house prices do to jobs? – Macro Business

- [Canada] Toronto Housing Market Steadies as Sellers Bide Their Time – Bloomberg

- [Canada] Canada’s house price boom takes off – Global Property Guide

- [Czech Republic] Czech mortgage market continues to fall in February – ING

- [Indonesia] The housing market in Indonesia rarely makes big moves – Global Property Guide

- [Ireland] Ireland Property Rush Risks Repeat of Crisis – Bloomberg

- [Japan] What Housing Crisis? In Japan, Home Prices Stay Flat – Wall Street Journal

- [Japan] NIMBYs Argue New Housing Supply Doesn’t Make Cities Affordable. They’re Wrong. – Reason

- [Latvia] Latvia’s house price rises decelerating – Global Property Guide

- [New Zealand] Household Leverage and Asymmetric Housing Wealth Effects- Evidence from New Zealand – Reserve Bank of New Zealand

- [Singapore] Singapore’s house price rises accelerating – Global Property Guide

- [Switzerland] Slowdown inevitable for house prices in Switzerland – Global Property Guide

- [Switzerland] Swiss Regulator Calls for Measures to Avert Property Bubble – Bloomberg

- [United Kingdom] Should tenants fear the rise of the corporate landlord? – Financial Times

On cross-country:

- Affordable Housing Crisis Spreads Throughout World – Wall Street Journal

- Film Director: Don’t Just Blame Gentrification for Housing Crisis – Wall Street Journal

- Mind the data gap: commercial property prices for policy – Bank for International Settlements

On the US:

- Bank Balance Sheets and Liquidation Values: Evidence from Real Estate Collateral – SSRN

- Expectations During the U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, April 4, 2019

Assessing the Risk of the Next Housing Bust

From the IMF’s latest Global Financial Stability report:

“There’s good news for people living in Las Vegas, Miami and Phoenix: the risk of a housing bust like the one they endured during the global financial crisis is fairly small. For folks in Toronto and Vancouver, however, the picture hasn’t improved since 2008, and the risk of a large decline in house prices remains elevated.

Those are among the insights generated by the IMF’s new tool for assessing the danger of a severe downturn in home prices. Homeowners, of course, are keenly interested in the value of what is probably their biggest asset. But there is also a strong link between home prices, the financial system, and the economy. The link is especially powerful when prices go down – as we explain in Chapter Two of the IMF’s twice-yearly Global Financial Stability Report.

Why do home prices matter for the broader economy? Housing construction and related spending on things like home improvements account for one-sixth of the US and euro-area economies, making them among the largest components of GDP. What’s more, mortgages and other housing-related lending are a big part of banks’ assets in many countries, so changes in house prices affect the health of the banking system.

Boom-bust cycle

It’s no surprise, then, that more than two-thirds of financial crises in recent decades were preceded by a boom-bust cycle in home prices, and that central banks in the United States, China, Australia, and elsewhere have recently expressed concern about large increases in home prices.

Fortunately, the IMF’s new tool can help policy makers gauge the likelihood of a future housing downturn and take early steps to help limit the damage. The tool, dubbed House Prices at Risk, feeds into the Fund’s growth-at-risk model, which links financial conditions to the danger of an economic downturn (see the October 2017 GFSR .)

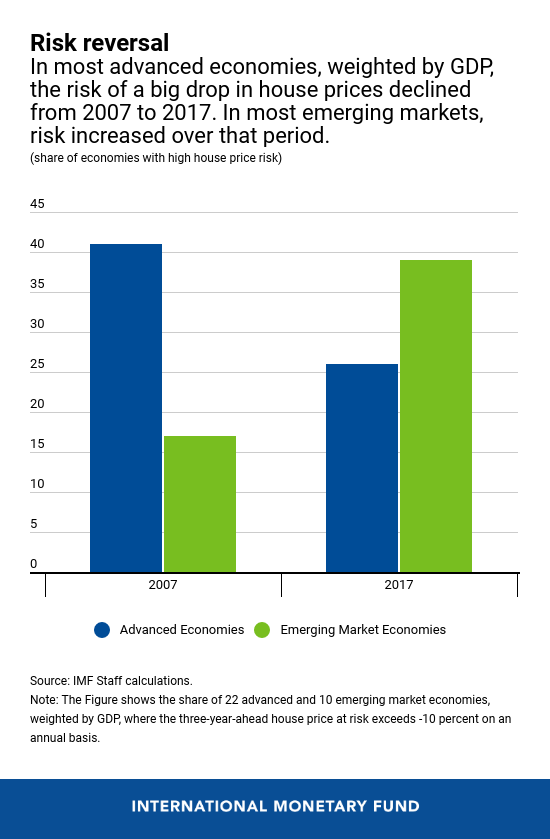

Our study encompasses data from 22 advanced economies, 10 emerging-market economies, and the major cities in those countries. We found that in most advanced economies in our sample, weighted by GDP, the odds of a big drop in inflation-adjusted house prices were lower at the end of 2017 than 10 years earlier but remained above the historical average. In emerging markets, by contrast, riskiness was higher in 2017 than on the eve of the global financial crisis. Nonetheless, downside risks to house prices remain elevated in more than 25 percent of these advanced economies and reached nearly 40 percent in emerging markets in our study. Among them, China stands out, especially its Eastern provinces.”

Continue reading here.

From the IMF’s latest Global Financial Stability report:

“There’s good news for people living in Las Vegas, Miami and Phoenix: the risk of a housing bust like the one they endured during the global financial crisis is fairly small. For folks in Toronto and Vancouver, however, the picture hasn’t improved since 2008, and the risk of a large decline in house prices remains elevated.

Those are among the insights generated by the IMF’s new tool for assessing the danger of a severe downturn in home prices.

Posted by at 10:06 AM

Labels: Global Housing Watch

Subscribe to: Posts