Tuesday, February 12, 2019

Housing Market in the Netherlands

From the latest IMF report on the Netherlands:

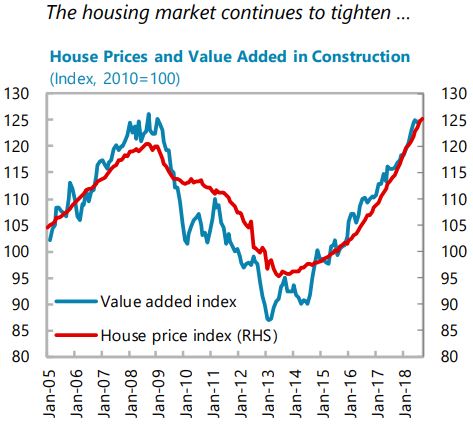

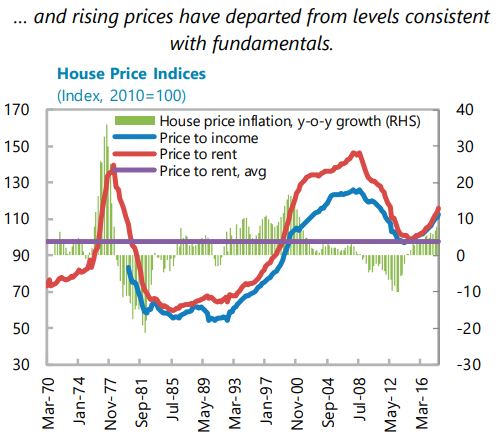

“The housing market is dominated by social housing (with a wait time exceeding a decade in some cases) and owner-occupied houses with significant shortages. The absence of a robust private rental market leaves young households, in particular, with little alternative to purchasing owner-occupied housing with high leverage and thin financial buffers. Rent controls, regulations, and inadequate means-testing result in long waiting lists for social housing. Elevated demand for owner-occupied houses was encouraged by generous mortgage interest deductibility (MID) in the past, which also boosted house prices. As macro-prudential policies were tightened recently, households’ debt has stabilized at about 250 percent of net disposable income, but it remains the second highest among OECD countries. Overborrowing on mortgages has contributed to the accumulation of household debt. When housing prices declined sharply after the global financial crisis (GFC), many mortgages were underwater and private consumption contracted sharply as households attempted to rebuild their net worth. Nevertheless, household overborrowing on mortgages is not a significant source of systemic risk in the financial sector even though it is a threat to the macro-economy

To reduce household debt and improve housing affordability, it is necessary to increase housing supply, tighten macro-prudential policies, and further reduce the debt bias in the tax system. Liberalizing rent controls for higher-income households and improving means-testing for social housing would help optimize allocation and improve housing supply. In addition, private investment should be encouraged by relaxing restrictions on zoning plans and simplifying administrative procedures for building permits. Lowering the maximum loan-to-value (LTV) ratio to no more than 90 percent (from 100 percent currently) and capping the debt service to income (DSTI) ratio to limit its procyclicality should be considered. The authorities plan to accelerate the phasing down of MID by 3 percentage points per year starting from 2020 until the basic rate of 37.05 percent is reached is a welcome step. Further phasing down of MID, to bring it at a neutral level compared with taxation of investment in other type of assets, would not only generate additional revenues but also help address the current debt bias of households.

The authorities emphasized that the focus is currently on increasing housing supply, while giving due consideration to possible tighter macro-prudential policies. To increase supply, the authorities are taking actions to improve coordination among the main stakeholders, including the relevant ministries, subnational governments, and private investors to reduce building preparation time, stimulate the transformation of suitable areas like outdated industrial areas for housing, and increase the amount of new construction plans. The authorities noted that the coalition agreement does address previous IMF recommendations to lower the MID but does not follow the previous IMF and Financial Stability Committee (FSC) recommendation to further lower LTV limits beyond the 100 percent ratio. The authorities noted that a lower LTV limit would make it more difficult, especially for younger households, to buy a house, while the middle-range rental market is already tight. The Dutch Central Bank and the Financial Market Authority noted that the current DSTI framework has procyclical elements. Increasing risk weights on mortgages in banks’ balance sheets and activating the countercyclical buffer could be considered if household debt continues to rise due to further tightening of the housing market.”

Posted by at 2:27 PM

Labels: Global Housing Watch

Subscribe to: Posts