Showing posts with label Forecasting Forum. Show all posts

Friday, July 6, 2018

Climate Change and NYU Volatility Institute

From Francis Diebold’s Blog:

“There is little doubt that climate change — tracking, assessment, and hopefully its eventual mitigation — is the burning issue of our times. Perhaps surprisingly, time-series econometric methods have much to offer for weather and climatological modeling (e.g., here), and several econometric groups in the UK, Denmark, and elsewhere have been pushing the agenda forward.

Now the NYU Volatility Institute is firmly on board. A couple months ago I was at their most recent annual conference, “A Financial Approach to Climate Risk”, but it somehow fell through the proverbial (blogging) cracks. The program is here, with links to many papers, slides, and videos. Two highlights, among many, were the presentations by Jim Stock (insights on the climate debate gleaned from econometric tools, slides here) and Bob Litterman (an asset-pricing perspective on the social cost of climate change, paper here). A fine initiative!”

From Francis Diebold’s Blog:

“There is little doubt that climate change — tracking, assessment, and hopefully its eventual mitigation — is the burning issue of our times. Perhaps surprisingly, time-series econometric methods have much to offer for weather and climatological modeling (e.g., here), and several econometric groups in the UK, Denmark, and elsewhere have been pushing the agenda forward.

Now the NYU Volatility Institute is firmly on board.

Posted by at 5:32 PM

Labels: Energy & Climate Change, Forecasting Forum

Wednesday, July 4, 2018

Worries about the yield curve

From a new Econbrowser post by James Hamilton:

“Why does a low or negative spread predict future economic weakness? One factor may be the Fed’s tightening cycle. Historically the inflation rate would at times start climbing above where the Fed wanted it. The Fed responded by raising the short-term rate, the traditional instrument of monetary policy. The market response of long-term rates to the higher short rates was significantly more muted. The result is that the yield spread narrowed as the tightening cycle continued. The Fed often found itself behind the curve, and the last short-term rate hikes were likely a contributing factor to some historical economic recessions.

But we’re still very early in the current tightening cycle. The 3-month Treasury bill has not gone up so far by nearly as much as it did in previous complete cycles, and inflation is still very moderate. So I don’t think it’s time to run for cover just yet. However, if the Fed were to raise the short rate by another 100 basis points without any move up in long rates, we would be into inverted territory, and I would be very concerned. Not a danger sign yet, but definitely an indicator to keep watching.”

From a new Econbrowser post by James Hamilton:

“Why does a low or negative spread predict future economic weakness? One factor may be the Fed’s tightening cycle. Historically the inflation rate would at times start climbing above where the Fed wanted it. The Fed responded by raising the short-term rate, the traditional instrument of monetary policy. The market response of long-term rates to the higher short rates was significantly more muted.

Posted by at 10:37 AM

Labels: Forecasting Forum

Monday, July 2, 2018

Can the Income-Expenditure Discrepancy Improve Forecasts?

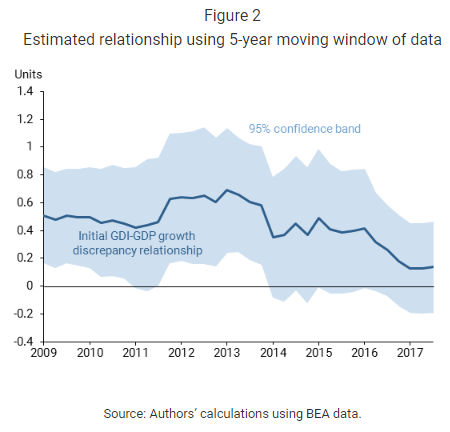

A new paper finds that “Gross domestic income and gross domestic product—GDI and GDP—measure aggregate economic activity using income and expenditure data, respectively. Discrepancies between the initial estimates of quarterly growth rates for these two measures appear to have some predictive power for subsequent GDP revisions. However, this power has weakened considerably since 2011. Similarly, the first revision to GDP growth has less predictive power in forecasting subsequent revisions since 2011. One possible explanation is that evolving data collection and estimation methods have helped improve initial GDP and GDI estimates.”

A new paper finds that “Gross domestic income and gross domestic product—GDI and GDP—measure aggregate economic activity using income and expenditure data, respectively. Discrepancies between the initial estimates of quarterly growth rates for these two measures appear to have some predictive power for subsequent GDP revisions. However, this power has weakened considerably since 2011. Similarly, the first revision to GDP growth has less predictive power in forecasting subsequent revisions since 2011. One possible explanation is that evolving data collection and estimation methods have helped improve initial GDP and GDI estimates.”

Posted by at 9:14 AM

Labels: Forecasting Forum

Wednesday, June 27, 2018

World Economic Outlook Forecast Tracker

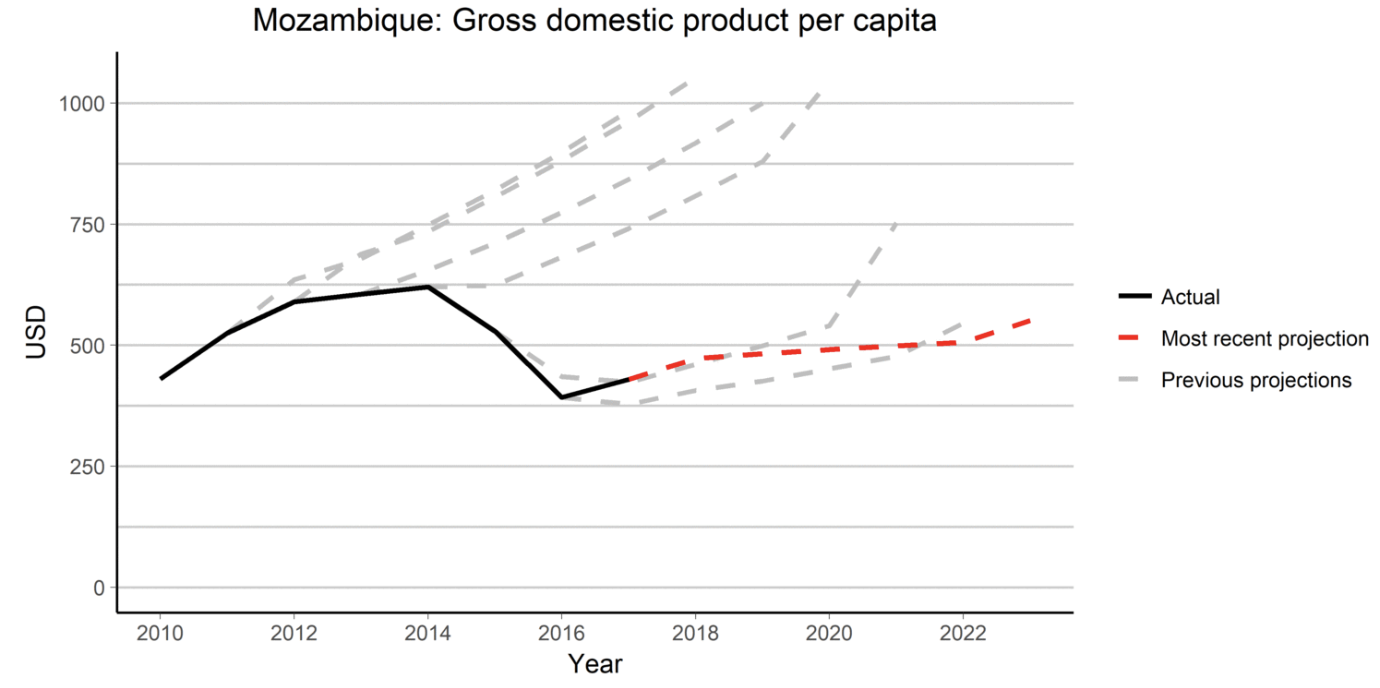

David Mihalyi and Tommy Morrison at NRGI created a World Economic Outlook Forecast Tracker that enables users to see how IMF economic projections have evolved over time. On it, you can select from an expansive list of countries and country groupings to track how IMF forecasts evolved year-to-year for dozens of economic indicators, such as GDP growth, government revenues and the budget deficit as well as the price of various commodities. The app shows an animated plot of the forecasts and historical values over 10 years, as well as providing a data download and a plot download (example attached).

David Mihalyi and Tommy Morrison at NRGI created a World Economic Outlook Forecast Tracker that enables users to see how IMF economic projections have evolved over time. On it, you can select from an expansive list of countries and country groupings to track how IMF forecasts evolved year-to-year for dozens of economic indicators, such as GDP growth, government revenues and the budget deficit as well as the price of various commodities.

Posted by at 8:27 PM

Labels: Forecasting Forum

Monday, June 25, 2018

Yahoo! Launches Recession Prep Guide

From a new post by Julia A. Seymour :

“New York Times economist Paul Krugman immediately reacted to the 2016 election of Donald Trump by warning of a possible “global recession.” Perhaps Yahoo! was taking pointers for its latest series. Even though the economy has been doing well, Yahoo! Finance just launched “Your Next-Recession Survival Guide” warning it is “time to prepare for the economic downturn, which could occur as early as 2020.” The new series began June 20.

[…]

In general, forecasting is unreliable. Financial Times wrote in 2014 that an analysis of all 1990s economic forecasts concluded there was great similarity between them and “the predictive record of economists was terrible.” Prakash Loungani, the author of the study, said “The record of failure to predict recessions is virtually unblemished.” ”

My paper is available here.

From a new post by Julia A. Seymour :

“New York Times economist Paul Krugman immediately reacted to the 2016 election of Donald Trump by warning of a possible “global recession.” Perhaps Yahoo! was taking pointers for its latest series. Even though the economy has been doing well, Yahoo! Finance just launched “Your Next-Recession Survival Guide” warning it is “time to prepare for the economic downturn, which could occur as early as 2020.”

Posted by at 10:10 AM

Labels: Forecasting Forum

Subscribe to: Posts