Thursday, August 2, 2012

Is Long-Term Unemployment Pushing Up Structural Unemployment?

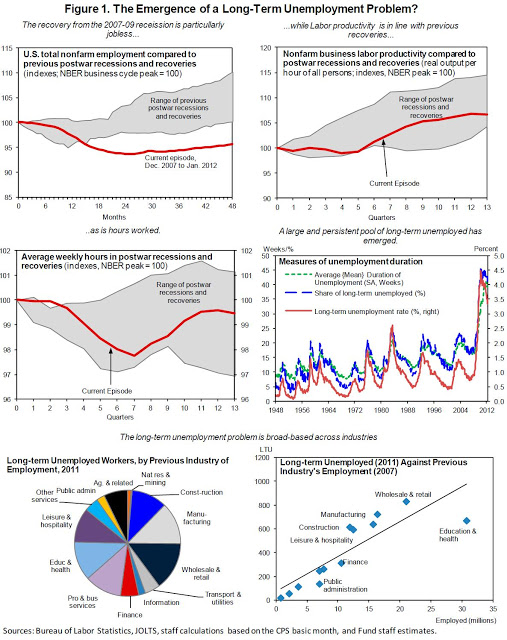

A new IMF report on US structural unemployment says that

while high long-term unemployment has not yet morphed into a permanent structural problem, it does pose an upward risk to the structural rate of unemployment. We have found that long-term unemployed are significantly less likely to find a job now than before the crisis, and that the loss in labor market matching efficiency observed since the recession is entirely due to a worsening of the labor matching of the long-term unemployed. Together, these results point to a risk that the structural rate of unemployment might be greater now than before the crisis.

Hence, forceful measures should be introduced that reduce long-term unemployment and address the risks associated with long spells of unemployment, namely skills erosion and a weaker attachment to the labor force. These measures include policies to increase demand for the long-term unemployed in the short run (active labor market policies, ALMP). When appropriately designed, such policies have been shown to be effective in improving employment and earnings prospects of long-term unemployed workers (Card et al, 2010; Card and Levine, 2000; Heinrich et al., 2008; Hotz et al., 2006). In particular, as discussed in the Staff report, a significant increase in ALMP resources is warranted given the persistently large pool of long-term unemployed and the risk that, as duration lengthens, their skills and attachment to the workforce might erode. Indeed, in terms of resources per long-term unemployed, the United States spends relatively little on active labor market policies, both compared to other OECD countries, and relative to its own pre-recession levels.

A new IMF report on US structural unemployment says that

while high long-term unemployment has not yet morphed into a permanent structural problem, it does pose an upward risk to the structural rate of unemployment. We have found that long-term unemployed are significantly less likely to find a job now than before the crisis, and that the loss in labor market matching efficiency observed since the recession is entirely due to a worsening of the labor matching of the long-term unemployed.

Posted by at 3:34 PM

Labels: Inclusive Growth

House Prices in the US

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP), including loosened eligibility criteria through the elimination of debt service-to-income cutoffs, and the tripling of incentives for investors to carry out principal reductions under HAMP’s Principal Reduction Alternative (PRA) (Box 5). Recent data suggests that the October 2011expansion of HARP seems to have led to a significant increase in HARP refinancing. The share of loans that have benefited from a principal reduction under the modification program (Home Affordable Modification program of HAMP) has also been on the rise, and early signs show that the tripling of the incentives for principal reductions is receiving interest from investors, and is likely to spur further principal reductions in the future. The recent State Attorneys General Settlement with the major banks, which resolved claims about improper foreclosures and abuses in servicing the loans, could lead in the medium run to a non-trivial reduction in foreclosures, including through up to $34 billion of principal reduction. Early signs indicate that the settlement has led banks to delay foreclosures and also to increasingly substitute them with “short sales” of underwater properties, which are less costly and count toward the banks’ commitment for principal reduction under the settlement. The authorities highlighted that greater reliance on short sales, as opposed to foreclosures, could support the housing market going forward.

The mission welcomed this progress, but also noted that more aggressive policy action may be warranted to accelerate the resolution of the housing crisis. As noted in the Fed’s November 2011 white paper, housing markets do not self-correct efficiently and, absent forceful policies to support the market, prices could fall below their equilibrium levels due to feedback loops from prices to demand and supply. If house prices are anticipated to decline, potential buyers could stay out of the market even if interest rates are low. Moreover, a decline in prices reduces housing equity, triggering further defaults and foreclosures. Foreclosures, in turn, put renewed downward pressure on prices, not only by adding to the supply of houses for sale, but also because they lead to a destruction of value and impose “deadweight” losses on the economy, hurting consumer wealth and credit availability.

The IMF’s 2012 annual report on the US economy says that “house prices have shown some firming recently, with a surprising increase in Q1 2012.” It also highlights that

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP),

Posted by at 3:33 PM

Labels: Global Housing Watch

Thursday, July 26, 2012

Successful Austerity in the United States, Europe and Japan

According to a new IMF working paper:

The large fiscal legacies of the global financial crisis have reignited the debate around the impact of fiscal policy onto economic activity during fiscal consolidations. The analysis in this paper shows that withdrawing fiscal stimuli too quickly in economies where output is already contracting can prolong their recessions without generating the expected fiscal saving. This is particularly true if the consolidation is centred around cuts to public expenditure—likely reflecting the fact that reductions in public spending have powerful effects on the consumption of financially-constrained agents in the economy—and if the size of the consolidation is large. Large consolidations make recessions more likely even when made at an expansion time. From a policy perspective this is especially relevant for periods of positive, though low growth. Accordingly, frontloading consolidations during a recession seems to aggravate the costs of fiscal adjustment in terms of output loss, while it seems to greatly delay the reduction in the debt-to-GDP ratio—which, in turn, can exacerbate market sentiment in a sovereign at times of low confidence, defying fiscal austerity efforts altogether. Again this is even truer in the case of consolidations based prominently on cuts to public spending.

Thus, a gradual fiscal adjustment, with a balanced composition of cuts to expenditure and tax increases boosts the chances that the consolidation will successfully (and rapidly) translate into lower debt-to-GDP ratios. Monetary policy can likely help alleviate further the pain of fiscal withdrawal if it is used proactively via reduction in the real interest rate.

According to a new IMF working paper:

The large fiscal legacies of the global financial crisis have reignited the debate around the impact of fiscal policy onto economic activity during fiscal consolidations. The analysis in this paper shows that withdrawing fiscal stimuli too quickly in economies where output is already contracting can prolong their recessions without generating the expected fiscal saving. This is particularly true if the consolidation is centred around cuts to public expenditure—likely reflecting the fact that reductions in public spending have powerful effects on the consumption of financially-constrained agents in the economy—and if the size of the consolidation is large.

Posted by at 7:45 PM

Labels: Inclusive Growth

Thursday, July 19, 2012

IMF Says Global Recovery Weak and Vulnerable; Depends on Resolving Euro Area Crisis

An already sluggish global recovery shows signs of further weakness, mainly because of continuing financial problems in Europe and slower-than-expected growth in emerging economies, the IMF said July 16 in a regular update to its World Economic Outlook.

An already sluggish global recovery shows signs of further weakness, mainly because of continuing financial problems in Europe and slower-than-expected growth in emerging economies, the IMF said July 16 in a regular update to its World Economic Outlook.

Posted by at 2:05 PM

Labels: Forecasting Forum

Tuesday, July 3, 2012

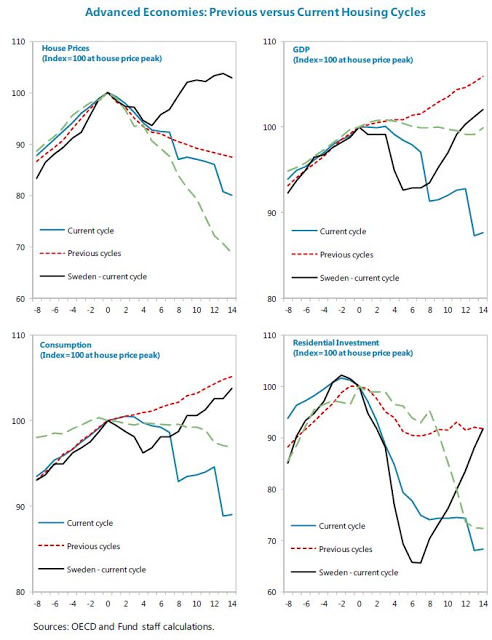

How Vulnerable Is Sweden’s Housing Market?

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value. Indeed, in the two years to 2011 Q2, residential investment (+37 percent) took off again, contrary to more muted developments during the previous recovery, offsetting the sharp drop in new homebuilding experienced during the global crisis.

Going forward, several factors may indicate further downward pressure on house prices. First, price-to-income and price-to-rent ratios remain 1.1 and 1.4 standard deviations respectively above historical averages. Second, staff’s model-based estimates from the Early Warning Exercise (EWE) and Vulnerability Exercise for Advanced Countries (VEA) suggest an overvaluation around 11–12 percent, exceeding the 10 percent threshold. (The EWE real estate model combines these three indicators to create a heat map for house price valuation.) Moreover, the predicted path of house prices based on WEO income projections suggests a decline of almost 5-6 percent through 2017.

These indicators put Sweden among the advanced countries where a house price correction is most likely to take place. Yet, the point estimate for the house price disequilibrium (the difference between actual prices and estimated equilibrium or long-run prices) is not large by historical standards, and Sweden ranks only 9th among 22 advanced economies in the VEA sample in terms of potential overvaluation. Furthermore, other components of residential real estate vulnerability (namely, potential impact on GDP, household balance sheets, and mortgage market characteristics) remain moderate or low in Sweden, compared to other advanced economies. That said, with most mortgages being “rollover” mortgages with terms of at most five years, any future interest rate increases could put additional strains on already highly indebted households.

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value.

Posted by at 2:24 PM

Labels: Global Housing Watch

Subscribe to: Posts