Friday, January 18, 2013

House Prices in Hong Kong

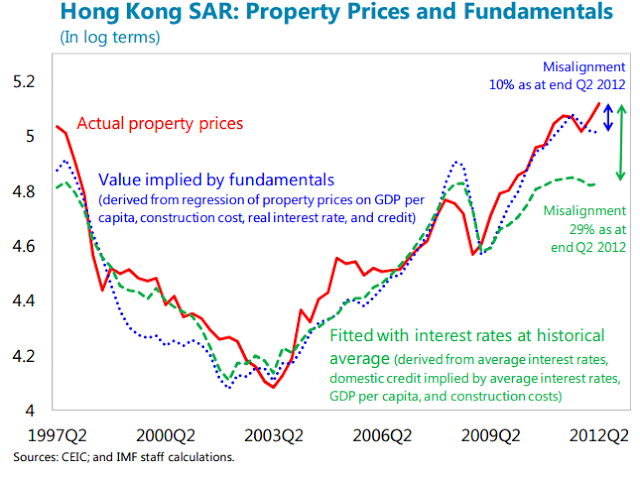

Two different pricing models are examined, which provide some mild, but on balance inconclusive, evidence that prices are higher than suggested by current fundamentals.

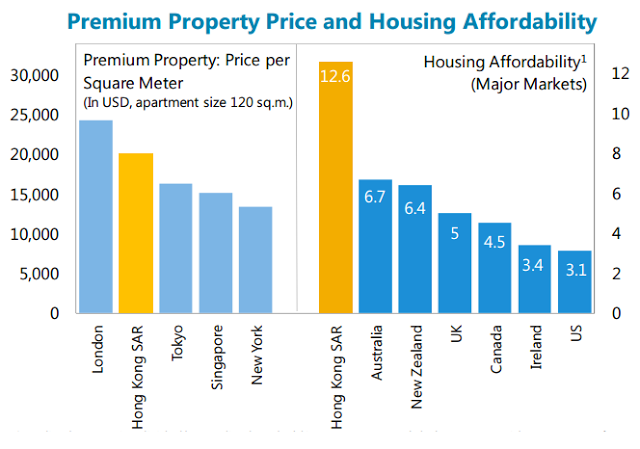

Housing in Hong Kong SAR is expensive. Compared to other regions, house prices in Hong Kong SAR are less affordable as measured by the ratio of median household income to median house price. In absolute terms, U.S. dollars per square meter, prices are also relatively expensive and premium real estate prices are on par or higher than in other high-cost housing.

A regression-based approach indicates prices are about 10 percent above the level suggested by current macroeconomic fundamentals.However, the fundamentals themselves are in some sense abnormal, as loose global monetary conditions have pushed down considerably Hong Kong SAR’s real interest rate. The real interest rate, moreover, is a key driver of housing prices in the model. To illustrate the impact of the eventual normalization of global monetary conditions, the regression estimates were used to calculate the price that would prevail if the real interest rate was at its 2003–07 average, with a concomitant change to credit. This exercise suggests that housing prices are some 30 percent higher than they would be if Hong Kong SAR’s real interest rate returned to the 2003–07 average. An asset pricing model, however, finds that prices are broadly consistent with fundamentals. The model compares the market price with a benchmark based on an equilibrium relationship between prices, rents, and cost of ownership. The basis for assessing misalignment from fundamentals is that the cost of owning a house (imputed rent) should be the same as the cost of renting a similar house for the same time period. By this measure, smaller-sized flats are found to be some 7 percent above the benchmark while the luxury end of the market is found to be slightly below the corresponding benchmark.

From the latest IMF’s report on Hong Kong’s economy:

Two different pricing models are examined, which provide some mild, but on balance inconclusive, evidence that prices are higher than suggested by current fundamentals.

Housing in Hong Kong SAR is expensive. Compared to other regions, house prices in Hong Kong SAR are less affordable as measured by the ratio of median household income to median house price. In absolute terms, U.S. dollars per square meter,

Posted by at 12:41 PM

Labels: Global Housing Watch

Wednesday, January 9, 2013

The Myth of the Jobless Recovery

From Slate:

You may have heard of the idea of a “jobless recovery,” a recovery in which the economy grows but doesn’t add jobs because of structural problems or because firms are adding robots instead or whatnot. Some hot new research from Laurence Ball, Daniel Leigh, and Prakash Loungani says the problem here is there’s no such thing as a jobless recovery and the classic Okun’s Law link between GDP growth and employment is holding up fine. If recent recoveries haven’t packed much job-creating punch it’s because the recoveries have been unusually slow in terms of GDP growth as well.

I liked that paper because I recently sat through the presentation of an economics paper showing that one leading explanation for jobless recoveries—a reversal of traditional “labor hoarding” behavior patterns—is wrong and based on bad data. It turns out, in other words, that counter-cyclical productivity doesn’t explain jobless recoveries both because productivity isn’t counter-cyclical and because there are no jobless recoveries.

From Slate:

You may have heard of the idea of a “jobless recovery,” a recovery in which the economy grows but doesn’t add jobs because of structural problems or because firms are adding robots instead or whatnot. Some hot new research from Laurence Ball, Daniel Leigh, and Prakash Loungani says the problem here is there’s no such thing as a jobless recovery and the classic Okun’s Law link between GDP growth and employment is holding up fine.

Posted by at 11:47 AM

Labels: Inclusive Growth

Monday, January 7, 2013

Growth Forecast Errors and Fiscal Multipliers

A new paper investigates the relation between growth forecast errors and planned fiscal consolidation during the crisis. The authors find that, in advanced economies, stronger planned fiscal consolidation has been associated with lower growth than expected, with the relation being particularly strong, both statistically and economically, early in the crisis. A natural interpretation is that fiscal multipliers were substantially higher than implicitly assumed by forecasters. The weaker relation in more recent years may reflect in part learning by forecasters and in part smaller multipliers than in the early years of the crisis.

A new paper investigates the relation between growth forecast errors and planned fiscal consolidation during the crisis. The authors find that, in advanced economies, stronger planned fiscal consolidation has been associated with lower growth than expected, with the relation being particularly strong, both statistically and economically, early in the crisis. A natural interpretation is that fiscal multipliers were substantially higher than implicitly assumed by forecasters. The weaker relation in more recent years may reflect in part learning by forecasters and in part smaller multipliers than in the early years of the crisis.

Posted by at 2:50 PM

Labels: Forecasting Forum

Saturday, December 29, 2012

House Prices in France

According to a new report, “Macroeconomic risks related to a correction in real estate prices appear to be relatively contained. The increase in housing prices (over 100 percent in real terms since the mid 1990s) has been supported by stronger fundaments (higher population growth, relatively low supply of housing, and low household indebtedness) than in other countries with rising real estate prices, but also by tax incentives that have fueled demand without addressing underlying supply constraints. There is a perception of price overvaluation, especially in Paris (by 10-20 percent at end-2011 according to staff estimates). However, there is no housing glut or household debt overhang that could trigger a sudden price adjustment. Moreover, stress tests suggest that banks are well placed to absorb the impact of a possible sizable price adjustment owing to tight underwriting criteria (emphasizing sustainability of the borrower’s income, not collateral value) and the absence of nonrecourse loans. The impact of a possible price correction on private demand would also be contained reflecting weak evidence of wealth effects on consumption.”

According to a new report, “Macroeconomic risks related to a correction in real estate prices appear to be relatively contained. The increase in housing prices (over 100 percent in real terms since the mid 1990s) has been supported by stronger fundaments (higher population growth, relatively low supply of housing, and low household indebtedness) than in other countries with rising real estate prices, but also by tax incentives that have fueled demand without addressing underlying supply constraints.

Posted by at 10:25 PM

Labels: Global Housing Watch

Friday, December 28, 2012

Macroprudential Policies and Housing Prices

Several countries in Central, Eastern and Southeastern Europe used a rich set of prudential instruments in response to last decade’s credit and housing boom and bust cycles. A new paper collects detailed information on these policy measures in a comprehensive database covering 16 countries at a quarterly frequency. The authors use this database to investigate whether the policy measures had an impact on housing price inflation. Their evidence suggests that some—but not all—measures did have an impact. These measures were changes in the minimum CAR and non-standard liquidity measures (marginal reserve requirements on foreign funding, marginal reserve requirements linked to credit growth).

Several countries in Central, Eastern and Southeastern Europe used a rich set of prudential instruments in response to last decade’s credit and housing boom and bust cycles. A new paper collects detailed information on these policy measures in a comprehensive database covering 16 countries at a quarterly frequency. The authors use this database to investigate whether the policy measures had an impact on housing price inflation. Their evidence suggests that some—but not all—measures did have an impact.

Posted by at 12:43 AM

Labels: Global Housing Watch

Subscribe to: Posts