Tuesday, April 2, 2013

How Labor Markets Can Support Workers, Economic Growth

IMF staff have taken a fresh look at how labor markets can support workers and growth.

The unemployment rate in advanced economies exceeds 8 percent, with much higher unemployment rates among the young. A third of all young unemployed have been without work for six months or longer.

Countries face the challenge of putting these millions of people back to work and getting the young started in their careers. A new IMF Staff Discussion Note—Labor Market Policies and IMF Advice in Advanced Economies during the Great Recession—reviews IMF advice to help countries meet this challenge

The paper was written by Olivier Blanchard, the IMF’s Economic Counselor and Research Department Director, along with his colleagues Florence Jaumotte and Prakash Loungani.

Weak demand

The IMF has diagnosed high unemployment to be a result primarily of weak aggregate demand, the paper notes. Hence, it has advised that monetary and fiscal policies support demand to the extent possible, alongside generous unemployment insurance to help people cope with the human costs of being out of work.

At the onset of the crisis, the IMF called for a coordinated global fiscal stimulus, which prevented “a much worse collapse in demand than actually took place.” Along with fiscal stimulus, the paper mentions the role of policies to promote work-sharing programs, particularly in Germany, and concludes that the positive experience “has led to a reassessment of such policies at the IMF and elsewhere.”

While in a number of countries high debt has now made fiscal consolidation unavoidable, the paper recommends that such consolidation should proceed as gradually as possible and be accompanied by supportive monetary policy.

While supportive macro policies are a central part of the IMF’s advice, the paper’s focus is on the design of labor market policies and institutions to reduce average unemployment rates and boost medium-run growth.

Micro flexibility

Productivity growth—the ultimate source of gains in incomes—requires reallocation of resources from low to high productivity jobs and firms. Labor markets must permit this “micro flexibility.”

Research strongly suggests that micro flexibility is better achieved by protecting workers through unemployment insurance than employment protection. Unemployment insurance, combined with support for job searchers, makes it easier for workers to move between jobs while safeguarding their welfare.

While there is an important role for employment protection, if excessive it impedes the necessary reallocation process. The authors also recommend that dual employment protection—where high employment protection for those on permanent contracts coexists with lighter regulation on temporary contracts—should be avoided. Such a system makes the burden of adjustment fall on those on temporary contracts, who are often the young. The concentration of unemployment among the youth in many countries is a result of this duality, the authors argue, noting that the IMF has advised reducing duality in Italy, Portugal, and Spain.

Macro flexibility

Labor market policies and institutions should allow economies to adjust to macroeconomic shocks while minimizing unemployment—this is “macro flexibility.” The paper suggests that to support this flexibility, a collective bargaining structure based on a combination of national and firm-level bargaining seems attractive.

While national agreements provide coordination and help wages and prices respond to macroeconomic shocks, firm-level agreements can help wages adjust to the circumstances that companies face. The authors recognize, however, that there are also examples of efficient bargaining at the sectoral level. What seems to be important in all cases is not so much the specific arrangements as trust among social partners.

For a number of euro area countries (the so-called “periphery” or “South”), the path to recovery is through enhanced competitiveness. The two options for doing so are increasing productivity and cutting relative wages. When this needs to be done urgently, the near-term burden often falls on wage cuts because raising productivity can take a long time.

While it would be best for governments, employers, and workers to agree on wage cuts, this typically has not happened. Absent such agreements, the IMF has suggested accelerating the adjustment through various options. These include making wages reflect productivity at the firm level and, in some cases, decreasing wages in the public sector.

Not all of the burden of adjustment should be borne by the “South.” The authors note that reversing the competitiveness gap in the euro area “implies accepting higher inflation in the North of the currency union than in the South”.

The start of a discussion?

As the title of the series suggests, IMF Staff Discussion Notes are published to elicit comments and further debate on topical issues. While the paper already reflects inputs from some international institutions and trade unions, there is a need for a fuller discussion on many open issues, particularly on collective bargaining.

From IMFSurvey Magazine

IMF staff have taken a fresh look at how labor markets can support workers and growth.

The unemployment rate in advanced economies exceeds 8 percent, with much higher unemployment rates among the young. A third of all young unemployed have been without work for six months or longer.

Countries face the challenge of putting these millions of people back to work and getting the young started in their careers.

Posted by at 5:56 PM

Labels: Inclusive Growth

Monday, February 18, 2013

Global House Price Watch

Global Housing Market: Spring in the air?

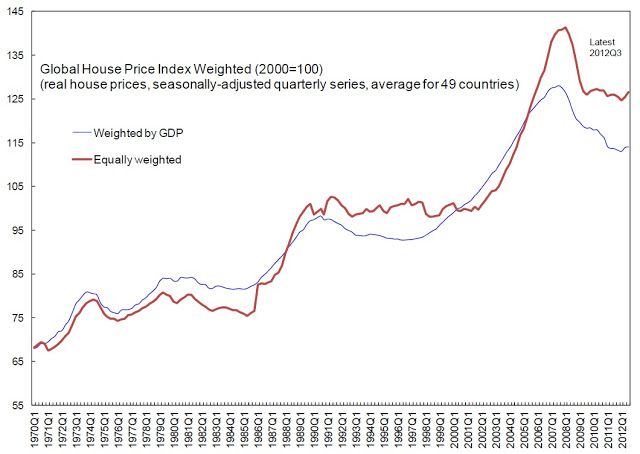

In a special report on house prices on March 30th 2002, the Economist said that if there is one single factor that has saved the world economy from a deep recession it is the housing market. In contrast, during the Great Recession (December 2007 to June 2009), the housing market was cast as the villain of the piece. How has the housing market fared since the end of the Great Recession? An updated global index of house prices has shown a mild sign of an uptick. Both the equally-weighted index and GDP-weighted index measures of global house prices show signs of improvement in house prices (see Chart 1).

Chart 1. Global House Price Index

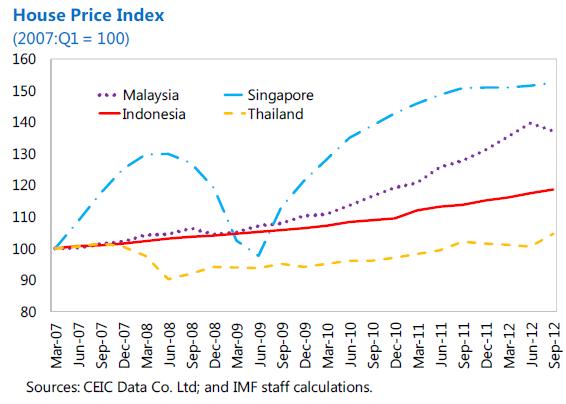

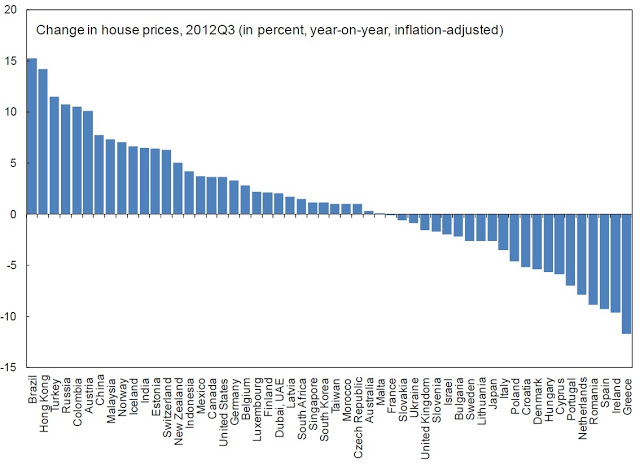

Zooming in, house prices around the world have followed different trajectories. In some parts of the world, house prices have appreciated or recovered, in others they continue to fall. For example, house prices for the United States have improved, while the outlook for house prices in a good part of Europe is gloomy.

Chart 2. House Prices around the World

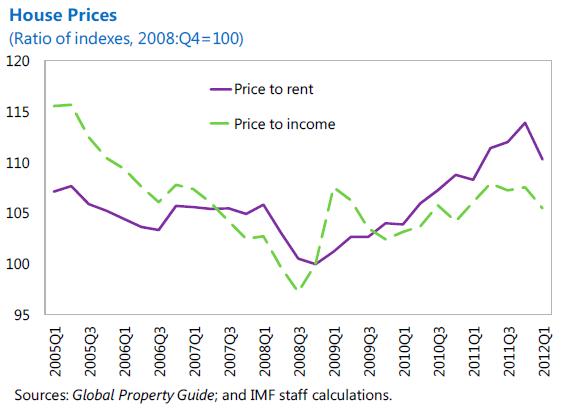

Still room for house price correction?

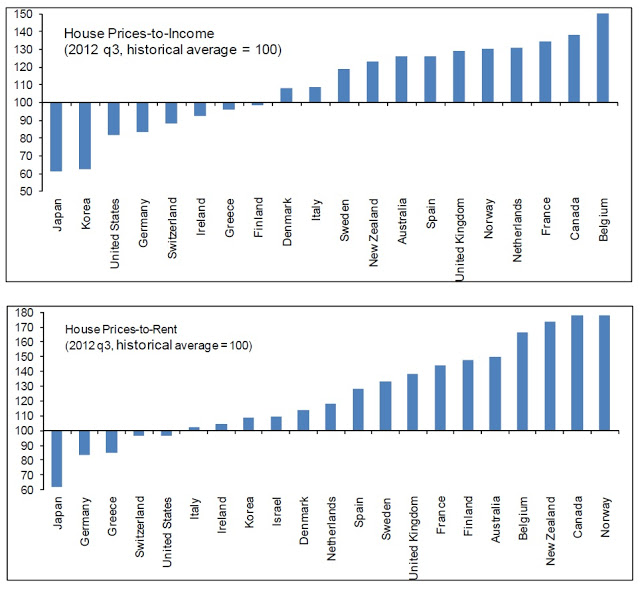

Chart 3 shows that in Canada, Belgium, Australia, United Kingdom and others, the house prices-to-income ratio and the house prices-to-rent ratio is still above historical averages. At the the other end, in Japan, United States, Germany, Greece and other countries, these rations are now below historical averages.

Chart 3. House Prices Relative to Incomes & Rents: Current Ratios Compared With Historical Averages

Assessing the outlook for house prices requires a more detailed look than just these historical ratios. In recent months, IMF staff have written about the outlook in Canada, Denmark, France, Hong Kong, Ireland and South Korea.

Global Housing Market: Spring in the air?

In a special report on house prices on March 30th 2002, the Economist said that if there is one single factor that has saved the world economy from a deep recession it is the housing market. In contrast, during the Great Recession (December 2007 to June 2009), the housing market was cast as the villain of the piece. How has the housing market fared since the end of the Great Recession?

Posted by at 5:53 PM

Labels: Global Housing Watch

Friday, February 15, 2013

House Prices in Canada

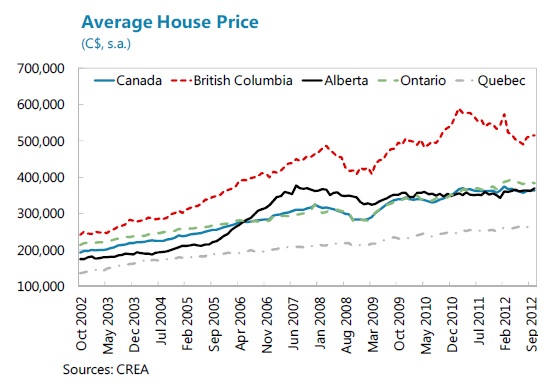

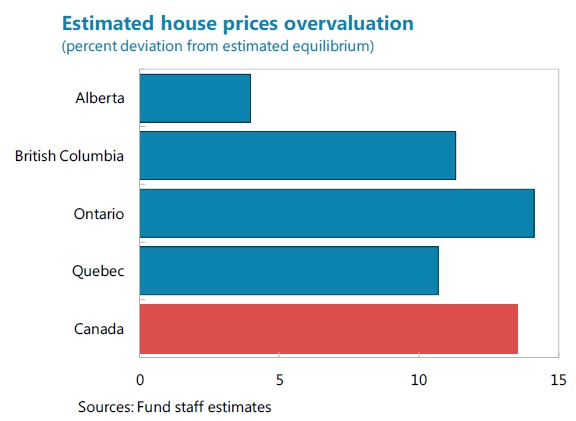

House price growth moderated in 2012, although with some regional variation. National house prices fell 1.2 percent over the second half of 2012, driven mainly by the sharp retrenchment in British Columbia. In turn, this was mainly the consequence of a sharp correction of prices in the Vancouver area, where condos prices were down to their 2010 levels as of December 2012. On a yearly basis, national house prices index is still up by about 3.5 percent in 2012, slightly down from the 6 percent growth in 2011, with Toronto, Calgary and in particular Regina posting the largest increases, according to a new IMF report on Canada.

Moreover, the report points out that house prices are still on the strong side. As of December 2012, at a national level house prices were still almost 30 percent above their January 2009 trough. In Q3:2012, the house price-to-rent ratio was 60 percent above its historical average in Canada, more than in any other advanced economies with the only exception of Norway and Belgium. Price-to-income ratios also look high, and at almost 40 percent above their long-term average are among the highest.

House price growth moderated in 2012, although with some regional variation. National house prices fell 1.2 percent over the second half of 2012, driven mainly by the sharp retrenchment in British Columbia. In turn, this was mainly the consequence of a sharp correction of prices in the Vancouver area, where condos prices were down to their 2010 levels as of December 2012. On a yearly basis, national house prices index is still up by about 3.5 percent in 2012,

Posted by at 1:54 AM

Labels: Global Housing Watch

Thursday, January 24, 2013

House Prices in Denmark

The latest IMF’s report on Denmark says that:

The Danish housing market continued its decline through 2011 and the first half of 2012, despite a short respite in 2010. Real house prices have fallen by 26 percent since their peak in 2007Q1, after a two-year period in which prices rose by over 60 percent. Housing starts declined by 17 percent in 2011, and by 28 percent in the first half of 2012 relative to the first six months of 2011. Year-on-year prices for the residential properties fell by 5–6 percent in 2012 Q2.

Indicators of house price misalignment are mixed. The price-to-income ratio and price-to-rent ratio remain above their 1970–2010 historical averages but by less than one standard deviation (0.7 and 0.9 respectively).

The housing market remains vulnerable. Mortgage loans with variable rates and deferred amortization loans (interest-only for 10 years) account for 74 and 56 percent of the mortgages respectively. Given the high debt levels of Danish households, this creates a threat of higher delinquencies should rates rise or incomes fall.

The latest IMF’s report on Denmark says that:

The Danish housing market continued its decline through 2011 and the first half of 2012, despite a short respite in 2010. Real house prices have fallen by 26 percent since their peak in 2007Q1, after a two-year period in which prices rose by over 60 percent. Housing starts declined by 17 percent in 2011, and by 28 percent in the first half of 2012 relative to the first six months of 2011.

Posted by at 2:48 PM

Labels: Global Housing Watch

Subscribe to: Posts