Saturday, April 20, 2013

Krugman on why this global recovery is different

Posted by at 11:42 AM

Labels: Forecasting Forum

What Next for the Eurozone? Macroeconomic Policy and the Recession

Posted by at 11:01 AM

Labels: Inclusive Growth

Wednesday, April 17, 2013

How the IMF became the friend who wants us to work less and drink more

From the Washington Post:

The International Monetary Fund has a reputation, hard earned over the decades, of being the annoying friend who is always telling you to be more responsible. Eat more vegetables! Put in more hours at the office! Do you really need that second glass of wine?

Similarly, it has historically been the IMF’s role to tell countries to behave themselves economically: Cut those deficits! Let’s see some tighter monetary policy! Do you really need such a generous public welfare system?

But something strange has changed in the world economy, which is evident in the Fund’s latest edition of the World Economic Outlook. The IMF is now among the strongest voices against excessive fiscal austerity and tight money.

The Fund is most direct in its prescriptions for Britain, which has had a stagnant economy for the past three years as deficit-reduction has gone into effect. Sure, the language is that ofinternational bureaucratese (“In the United Kingdom, where recovery is weak owing to lackluster demand, consideration should be given to greater near-term flexibility in the fiscal adjustment.”). But there is no mistaking the message: Hey, David Cameron! Slow down with the deficit reduction!

Similarly, the Fund worries that the United States is reducing deficits too fast under the sequester spending cuts. “In the United States, the concern is that the budget sequester will lead to excessive consolidation,” says the WEO. Continue reading the Washington Post article here.

From the Washington Post:

The International Monetary Fund has a reputation, hard earned over the decades, of being the annoying friend who is always telling you to be more responsible. Eat more vegetables! Put in more hours at the office! Do you really need that second glass of wine?

Similarly, it has historically been the IMF’s role to tell countries to behave themselves economically: Cut those deficits! Let’s see some tighter monetary policy!

Posted by at 10:03 AM

Labels: Forecasting Forum

Tuesday, April 16, 2013

Why is the Global Recovery So Weak?

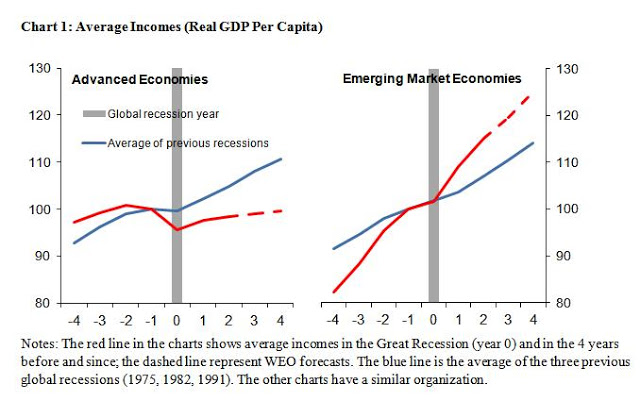

The Great Recession has been followed by the Not-So-Great Recovery. The IMF’s World Economic Outlook (WEO) shows that average incomes in advanced economies are rising, and are projected to rise, at a much slower rate than in past global recoveries. In contrast, incomes in emerging markets are growing at a much faster pace than during past recoveries—see chart 1. The WEO discusses several reasons for this divergence in fortunes.

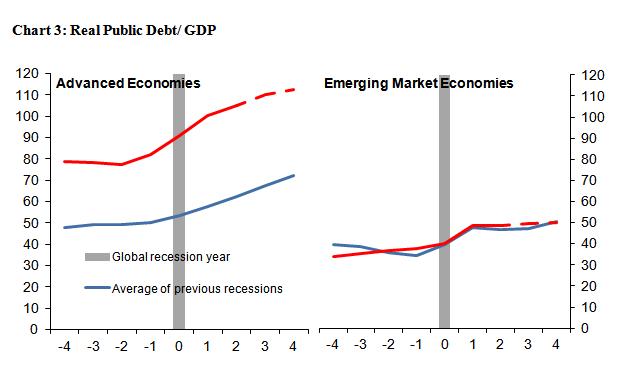

Caution about fiscal stimulus in advanced countries likely reflects the fact that they entered the Great Recession with much higher levels of debt than in the past—see Chart 3.

Box 1.1 does not get into an “an assessment of whether the different policy mix in this recession and recovery was appropriate. The response of policies may have been reasonable given the respective room available for fiscal and monetary policies in advanced economies. But there are also concerns. Even though monetary policy has been effective, policymakers had to resort to unconventional measures. Even with these measures, the zero bound on interest rates and the extent of financial disruption during the crisis have lowered the traction of monetary policy. This, together with the extent of slack in these economies, may have amplified the impact of contractionary fiscal policies. Four years into a weak recovery, policymakers may therefore need to worry about the risk of overburdening monetary policy because it is being relied on to deliver more than it has traditionally.”

Read Box 1.1 from the WEO here for the full analysis.

The Great Recession has been followed by the Not-So-Great Recovery. The IMF’s World Economic Outlook (WEO) shows that average incomes in advanced economies are rising, and are projected to rise, at a much slower rate than in past global recoveries. In contrast, incomes in emerging markets are growing at a much faster pace than during past recoveries—see chart 1. The WEO discusses several reasons for this divergence in fortunes.

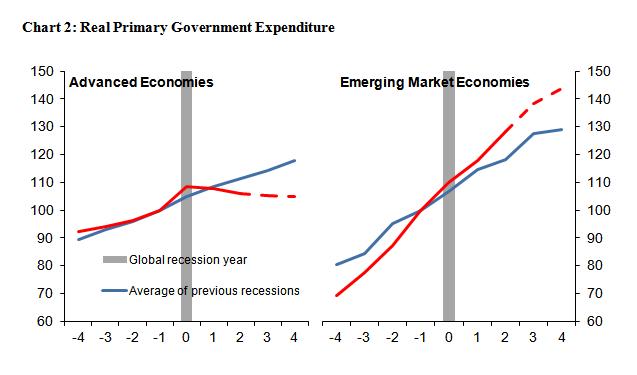

Box 1.1 of the WEO notes the divergence in fiscal polices. Read the full article…

Posted by at 12:25 PM

Labels: Forecasting Forum

Thursday, April 4, 2013

IMF Urges Caution on Union Policy

A WSJ blog notes: Changing euro-zone labor-market institutions has been one of the main goals of the bailout programs managed by the International Monetary Fund and euro-zone authorities over the last three years.

The thinking is: Europe’s labor markets – particularly those in the euro-zone periphery – need overhauls to allow wages to keep pace with changes in productivity and economic circumstances. This sounds like dry stuff, but it’s been one of the fund’s more controversial bailout recommendations. Making labor markets more “flexible” has in practice meant reducing the role of labor unions in wage-setting across much of southern Europe, leaving unions none-too-pleased with their more limited powers.

In a paper published on Friday, IMF economists led by Olivier Blanchard took a somewhat soul-searching look at the fund’s labor-market advice over the last three years. One interesting finding: The fund should “tread carefully” in its recommendations on collective bargaining, the paper suggests, since evidence about what kinds of bargaining arrangements work best is mixed. Read the full article here.

A WSJ blog notes: Changing euro-zone labor-market institutions has been one of the main goals of the bailout programs managed by the International Monetary Fund and euro-zone authorities over the last three years.

The thinking is: Europe’s labor markets – particularly those in the euro-zone periphery – need overhauls to allow wages to keep pace with changes in productivity and economic circumstances. This sounds like dry stuff, but it’s been one of the fund’s more controversial bailout recommendations.

Posted by at 9:26 PM

Labels: Inclusive Growth

Subscribe to: Posts