Friday, December 19, 2014

House Prices in Netherlands

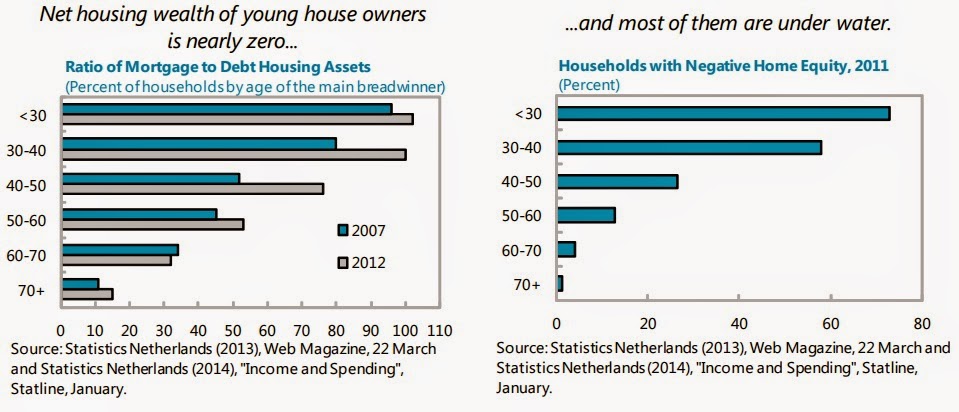

“The global recession and regulatory tightening have helped deflate the housing prices with the losses falling disproportionately on the younger generations. House prices have declined by 27 percent in real terms since their peak in late 2008. The deflation of Dutch housing prices has caused massive losses of wealth which are unevenly distributed across generations. Younger house buyers are burdened by the lion’s share of losses in housing wealth. In addition to greater housing losses, younger households have not have sufficient time to accumulate pension claims and other (financial) assets households under the age of 35 have negligible levels of net worth,” Read the full article…

Posted by at 8:02 PM

Labels: Global Housing Watch

Wednesday, December 10, 2014

IIMB-IMF Conference on Housing Markets, Financial Stability and Growth

Inaugural Address

R V Verma, Former Chairman, NHB

Session 1: Macroprudential Policies

Chair: Arvind Virmani, Former ED, IMF

Ratna Sahay, IMF

How to Manage Housing Booms: What Does the Cross-Country Evidence Show? (PPT)

Jihad Dagher, IMF

Housing Finance and Real Estate Booms: A Cross-Country Perspective

Discussant: Hans Genberg, Bank Negara Malaysia and SEACEN (PPT)

Session 2: Frontiers of Housing Research

Chair: Hans Genberg, Bank Negara Malaysia and SEACEN

Inho Song, Korea Development Institute

Housing as a Unique Asset

Discussant: Mico Loretan, Swiss National Bank (PPT)

Chetan Subramanian, IIM-Bangalore

Asset Price Bubbles and Endogenous Growth

Discussant: Romar Correa, University of Mumbai

Session 3: Housing Finance

Chair: K Kanagasabapathy, Former Adviser-in-charge, MPD, RBI

Veronica Warnock, University of Virginia

Developing Housing Finance Systems: A Global Perspective

Simon Walley, World Bank

Housing the World: Leveraging Private Sector Resources for the Public Good (PPT)

Frank Warnock, University of Virginia

Housing Finance in Latin America: What is Holding it Back?

Discussants: R. S. Deshpande, Former Director, ISEC

Devi Prasad, Former Director, FPI

Chair: R. S. Deshpande, Former Director, ISEC

Somik Lall, World Bank

Urbanization and Housing Investment (PPT)

Discussant: Frank Warnock, University of Virginia

Tony Venables, Oxford

Housing in African Cities: Why it Matters and What is Going Wrong (PPT)

Discussant: Ashima Goyal, IGIDR, Mumbai (PPT)

Chair: Ashima Goyal, IGIDR, Mumbai

Hites Ahir, IMF

House Prices in Emerging Markets (PPT)

Mick Silver, IMF

Real Estate Price Measurement: Availability and Importance (PPT)

Discussant: Manoranjan Sharma, GM, Canara Bank

Alessandro Rebucci, Johns Hopkins University

Capital Flows, House Prices and the Macroeconomy (PPT)

Discussant: Mick Silver, IMF (PPT)

Chair: Alok Sheel, Secretary, Government of India

Presenter: H. A. C. Prasad, MoF, Gol; Lalit Kumar, National Housing Bank and Charan Singh, IIM-Bangalore

Housing Market in India (PPT)

Roundtable: Senior management from State Bank of India, ICICI, State Bank of Mysore and Canara Bank

G. S. Sandhu, Former Secretary, Financial Services, MoF, GoI

Here are links to papers and presentations for the conference. A link to the speech by Ratna Sahay will be posted later. Scroll down for links to papers and presentations on housing finance (by Frank Warnock, Veronica Warnock, Simon Walley); on urbanization (Somik Lall, Tony Venables); house prices in emerging markets (Hites Ahir, Mick Silver and Alessandro Rebucci); and the housing market in India (H. A. C. Prasad, Lalit Kumar, and Charan Singh). Also, see a blog by Min Zhu on Managing House Price Booms in Emerging Markets, Read the full article…

Posted by at 10:51 AM

Labels: Global Housing Watch

Thursday, November 20, 2014

Does Growth Lower Unemployment? (Was Krugman Right Yet Again)?

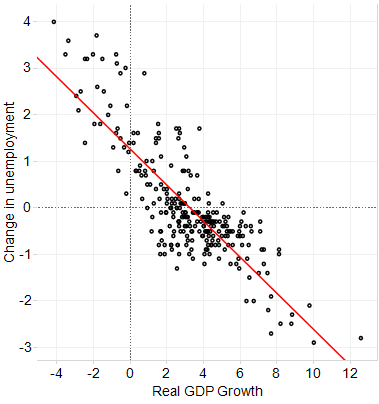

On July 9, 2011 when U.S. unemployment was at record highs, Paul Krugman wrote: “Why is unemployment remaining high? Because growth is weak — period, full stop, end of story.” Krugman went on to appeal to an old relationship known as Okun’s Law: “Historically, low or negative growth has meant rising unemployment, fast growth falling unemployment (Okun’s Law).”

How well has Okun’s Law held up in the 3 ½ years since Krugman wrote? The evidence for the period 1947 to the present is shown below. It is evident that, for the U.S., Okun’s Law has held up quite well, as I have noted before.

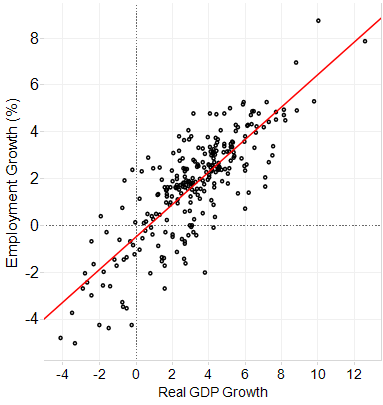

In a recent presentation at Oberlin College, I also looked at how well Okun’s Law holds across the world. If you don’t want to flip through the (fascinating) 100-slide presentation, I did a short summary this week for the IMF’s blog.

On July 9, 2011 when U.S. unemployment was at record highs, Paul Krugman wrote: “Why is unemployment remaining high? Because growth is weak — period, full stop, end of story.” Krugman went on to appeal to an old relationship known as Okun’s Law: “Historically, low or negative growth has meant rising unemployment, fast growth falling unemployment (Okun’s Law).”

How well has Okun’s Law held up in the 3 ½ years since Krugman wrote? Read the full article…

Posted by at 5:36 PM

Labels: Inclusive Growth

Wednesday, October 22, 2014

House Prices in Cyprus

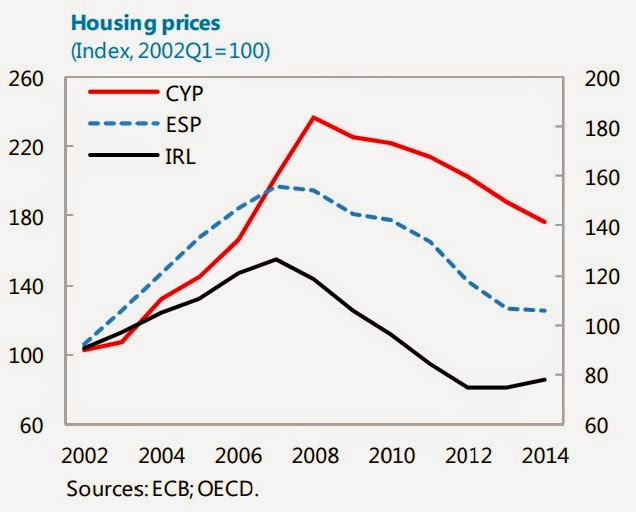

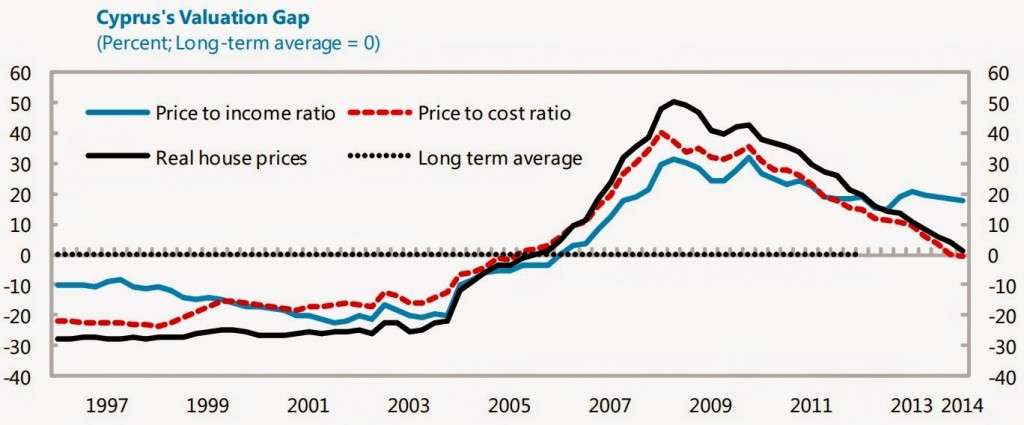

“The [housing market] boom, which took place during 2004–08, was among the largest in the euro-area, and was driven by FDI and rapid credit growth. The bust was triggered by a decline in FDI following the onset of the global crisis in 2008 and was exacerbated by falling domestic output and employment starting with 2009. Despite their sizeable decline to date, housing prices may have further room to fall before reaching equilibrium. House prices have already declined by 26 percent since their peak in 2008. However, according to common house price ratios, the overvaluation gap is around 0–20 percent, with an average across methodologies of 7 percent. According to a housing market model, the valuation gap is around 14 percent,” says a new IMF study on the Housing Market in Cyprus: From Boom to Bust. Read the complete study here.

“The [housing market] boom, which took place during 2004–08, was among the largest in the euro-area, and was driven by FDI and rapid credit growth. The bust was triggered by a decline in FDI following the onset of the global crisis in 2008 and was exacerbated by falling domestic output and employment starting with 2009. Despite their sizeable decline to date, housing prices may have further room to fall before reaching equilibrium. House prices have already declined by 26 percent since their peak in 2008.

Posted by at 3:39 PM

Labels: Global Housing Watch

Monday, October 20, 2014

House Prices in Singapore

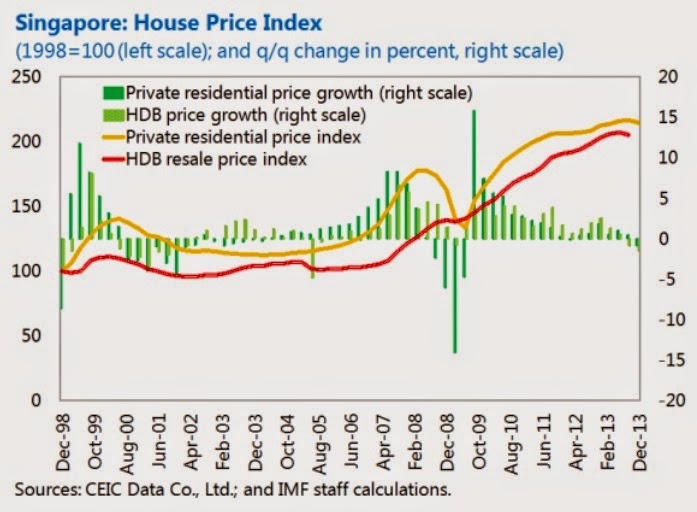

“Singapore’s housing market is cooling. Both private and public house price growth turned negative in late-2013, and declined by 1.3 percent and 1.6 percent (q/q), respectively, in the first quarter of 2014. Indicators on the quantity side also indicate a softening of the market: the number of housing transactions has been decreasing; house supply conditions, which had tightened in the mid-2000s due to rising population, have been easing; and vacancy rates are rising. Going forward, further downward pressure on house price is expected with a large supply of new housing set to come on the market in the coming years,” according to the IMF’s latest economic report on Singapore.

“Singapore’s housing market is cooling. Both private and public house price growth turned negative in late-2013, and declined by 1.3 percent and 1.6 percent (q/q), respectively, in the first quarter of 2014. Indicators on the quantity side also indicate a softening of the market: the number of housing transactions has been decreasing; house supply conditions, which had tightened in the mid-2000s due to rising population, have been easing; and vacancy rates are rising. Going forward,

Posted by at 2:36 PM

Labels: Global Housing Watch

Subscribe to: Posts