Monday, September 14, 2015

Macroprudential Policies in the Philippines

The IMF’s report on the Philippines points out the macroprudential policies that have been implemented. The report says: “In light of the acceleration in credit growth in 2014 and risks of domestic asset price booms, the BSP [Central Bank of Philippines] conducted stress tests on banks’ real estate loan exposures and required corrective actions, enhanced monitoring of banks’ exposures to all types of real estate, and provided guidance on real estate mortgage loans, setting their maximum loan value at 60 percent of the appraised value. These measures have helped to restrain credit growth to the real estate sector. Single borrower limits (set at 25 percent of core capital) should be strictly enforced with the additional 25 percent allowance for exposures to PPPs allowed to lapse.”

The IMF’s report on the Philippines points out the macroprudential policies that have been implemented. The report says: “In light of the acceleration in credit growth in 2014 and risks of domestic asset price booms, the BSP [Central Bank of Philippines] conducted stress tests on banks’ real estate loan exposures and required corrective actions, enhanced monitoring of banks’ exposures to all types of real estate, and provided guidance on real estate mortgage loans,

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, September 11, 2015

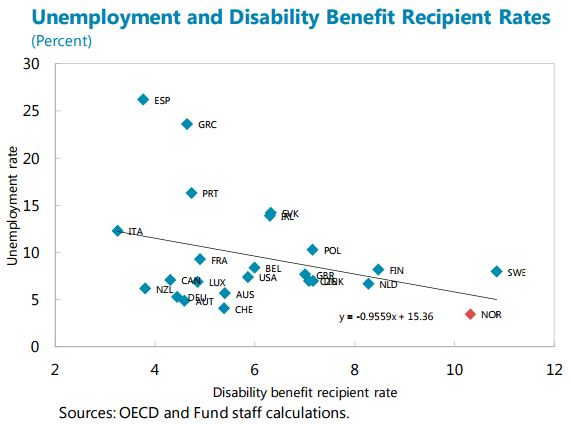

What Lies Behind Norway’s Low Unemployment Rate?

The unemployment rate in Norway is one of the lowest among OECD countries. At the same time, according to an IMF report, absence from work due to sickness “is the highest among the OECD countries, and so is expenditure on health related benefits, which is more than 5 percent of GDP. About one-fifth of the working age population receives income supports related to health problems or disability, which is nearly everybody who is not working. Read the full article…

Posted by at 9:00 AM

Labels: Inclusive Growth

Wednesday, September 9, 2015

Norway: Peak in Oil Fortunes?

“Norway’s half century of good fortune from its oil and gas wealth may have peaked,” according to an IMF report. “Oil and gas production will continue for many decades on current projections, but output and investment have flattened out, and the spillovers from the offshore oil and gas production to the mainland economy may have turned from positive to negative. Thus far, economic policy has needed to focus on managing the windfall, and Norway’s institutions have been a model for other countries. Read the full article…

Posted by at 5:35 PM

Labels: Energy & Climate Change

Monday, September 7, 2015

Labor Day Special: How Countries Rank on Whether Growth Creates Jobs

|

| Turkey’s Labour and Social Security Minister Ahmet Erdem (center), surrounded by Labour and Employment Ministers of the G20, poses for a family photo during the G20 Ministerial meeting in Ankara, Turkey on Sept 3. (AFP) |

Does economic growth lead to job creation in the short run (over a year)? This new report ranks the G20 countries on how well they are able to translate short run growth into more jobs. Check your guesses against the answers in the report.

Turkey’s Labour and Social Security Minister Ahmet Erdem (center), surrounded by Labour and Employment Ministers of the G20, poses for a family photo during the G20 Ministerial meeting in Ankara, Read the full article…

Posted by at 11:47 AM

Labels: Inclusive Growth

Thursday, August 27, 2015

Behind the commodities bust

First was the dot-com bubble, then the housing bubble. Now comes the commodities bubble. We don’t fully understand the stock market’s current turmoil, but we know it’s driven at least in part by a bubble of raw material prices. Their collapse weighs on world stock markets through fears of slower economic growth and large financial losses.

All bubbles share similar characteristics. There’s a strong, enthusiastic demand for some object (whether stocks, homes, oil or tulips). High demand pushes up prices, which inspires more demand. Prices ultimately reach unsustainable levels so that when spending slows, the bubble implodes. Commodities have now traced this familiar path.

As the Economist reminds us, raw material prices respond to different influences. Weather affects crops; technology (a.k.a. “fracking”) affects oil recovery. Still, despite these variations, prices of many commodities — not just oil — have followed roughly similar trajectories in recent years. They have dropped steeply, according to figures from the International Monetary Fund.

Here are declines for five commodities from 2012 through July 2015: oil, down 48 percent; iron ore, 60 percent; copper, 31 percent; palm oil, 39 percent; and wheat, 37 percent. Many commodity prices have continued to fall.

The bubble formed on hopes that China’s rapid growth would feed an ever-expanding appetite for raw materials, says economist John Mothersole of the consulting firm IHS Global Insight. Demand and prices would remain high indefinitely. Although prices fell after the 2008-09 financial crisis, China’s huge “stimulus” package — intended to offset the crisis’s drag — sent them up again, says Mothersole. China’s demand seemed destined to stay strong, as economic growth would stabilize at a high level.

It didn’t. In 2010, China’s economy grew 10 percent; the IMF expects 6.8 percent in 2015 and 6.3 percent in 2016. Other economists think growth could be lower. As a result, much of the added production capacity — mines and the like — to supply China isn’t needed. “There’s a new commodities era,” says economist Rabah Arezki, head of the IMF’s commodities research. “Everyone was rushing to invest. Now they have to adjust to a new lower level of demand.”

Continue reading here.

|

| Workers carry pipes to install an irrigation line in a coffee farm in Santo Antonio do Jardim, Brazil, last year. (Paulo Whitaker/Reuters) |

By Bob Samuelson [The Washington Post]:

First was the dot-com bubble, then the housing bubble. Now comes the commodities bubble. We don’t fully understand the stock market’s current turmoil, but we know it’s driven at least in part by a bubble of raw material prices. Their collapse weighs on world stock markets through fears of slower economic growth and large financial losses.

All bubbles share similar characteristics. There’s a strong,

Posted by at 4:27 AM

Labels: Energy & Climate Change

Subscribe to: Posts