Wednesday, December 23, 2015

Understanding China’s Housing Market

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”, in 2013. “End of the golden era: China’s property market is cooling off, at long last”, in 2014. These days, together with the housing market, analysts are also expressing concerns about the overall health of the Chinese economy. Here is one headline from 2015: “Coming down to earth: Chinese growth is losing altitude. Will it be a soft or hard landing?”

So why China’s housing market has not seen a bust yet? At last weekend’s conference in Shenzhen on December 18-19, leading experts on China’s housing market provided some answers. The conference—International Symposium on Housing and Financial Stability in China—was organized by the Chinese University of Hong Kong in Shenzhen, International Monetary Fund, and Princeton University.

Getting the facts right: housing and mortgage market

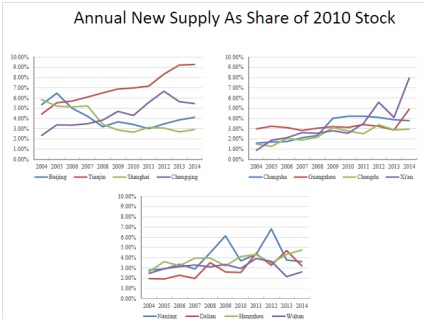

New research by Joe Gyourko (University of Pennsylvania) and his co-authors provides facts on China’s housing market from a supply and demand perspective. “In China, different housing markets behave very differently. A boom in Beijing and Shenzhen doesn’t mean a boom everywhere”, Gyourko said at the conference.

In his presentation, Gyourko made two key points. First point: there is substantial heterogeneity across cities in the balance between housing supply and demand. At one end, housing supply has outpaced demand in the interior part of the country. Specifically, housing supply has outpaced demand by at least 30 percent in twelve major markets and by 10 to 29 percent in another eight markets. On the other end, housing demand has outpaced supply in most major eastern markets. These include: Beijing, Hangzhou, Shanghai, and Shenzhen. Second point: markets such as Beijing, despite their strong measured fundamentals, should be considered somewhat risky because homes there trade at very high multiples of rent.

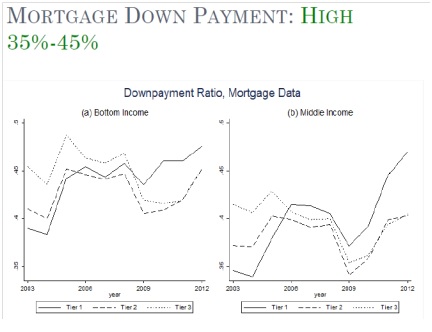

Another new piece of research, by Hanming Fang (University of Pennsylvania) and his co-authors, provides facts on China’s housing market from the mortgage market perspective. They have constructed a set of house price indices for 120 major cities in China and used a comprehensive data set of mortgage loans from 2003 to 2013. In his presentation, Fang showed that the Chinese housing boom has been accompanied by strong growth in income, and high mortgage down payments. For a decade, household’s disposable income has had an average annual real growth of 9 percent at the national level. Also, down payments have been over 30 percent on all mortgage loans.

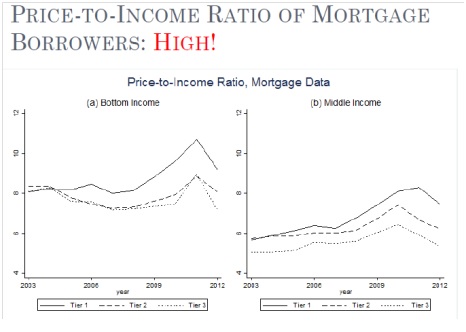

However, Fang noted that the participation of low-income home buyers in the housing boom has been characterized by high price-to-income ratios. The ratios are around eight in second and third tier cities, and even ten in first tier cities.

Haizhou Huang (CICC) provided very interesting facts on China’s housing market from the perspective of population in big cities. Huang pointed out that population concentrates into big cities. For example, in Japan and the United States, an increase in urbanization was accompanied by an increase in population concentration in big cities. So Huang expects that population concentration in China’s big cities will continue to rise. This could lead to more pressure on the housing market in Tier 1 cities. Huang asks: “Should China follow the European or Japanese model of few cities that have a large amount of the population?” China needs to develop more megacities, in his view. This could imply that the housing market could continue to grow and pressure in the housing market in tier I cities could decrease in the future.

Xiaobo Zhang (Peking University) talked the impact on China’s housing market from cultural traditions. “In rural areas of China, a new home is a necessary condition for marriage”, says Zhang. This is due in part by the sex ratio imbalance in China. Zhang showed that in 2000, 1 in 14 males could not marry. And in 2005, it was 1 in 10.

Assessing the risks: the role of expectations and local government debt

One area of risk is the role of expectations. Fang and Gyourko said that risks in Chinese housing market could arise with a shift in expectations. Specifically, Fang said that the willingness of low-income homebuyers to endure high price-to-income rations is explained by expectation of continued growth in income. However, the high expectation of future income growth may not be sustainable. Likewise, Gyourko said that a modest downward shift in expectations could generate sharp decline in house prices.

Moreover, Richard Koss (Global Housing Watch Initiative) compared how expectations have played an important role in the housing market in China and the United States. In both countries, expectations have played a role, but in different ways. Koss said that in the United States, expectations played a role in terms of house prices (e.g. expectations that house prices would continue rising), while in China, expectations play a role in terms of income growth (e.g. expectations that income will continue rising).

In the United States, said Koss, “No one thought house prices could fall as they never had on a nationwide basis, although specific regions suffered declines in the past. Americans thought they were special and that financial innovation would minimize risks but that turned out to be completely wrong.” So, in China, there could be risks in terms of irrational expectations of income growth.

Another area of risk is the local government debt and its linkage with the housing market. A new paper by Yongheng Deng (National University of Singapore) and his co-authors explores this link. At the conference, Deng noted that unlike local governments in western countries, local Chinese governments are prevented from directly issuing debt to fund mandated capital projects. Therefore, local governments tap into the growing housing market by selling public land to rise funding.

More specifically, future land sales revenue are used to repay the local government’s debt and land parcels are the most widely-used collateral for local government debt. This implies that “a substantial drop in housing or land prices may increase the risk level of local government debt, or even trigger a systematic default”, said Deng.

From the Global Housing Watch Newsletter: December 2015

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”,

Posted by at 4:46 PM

Labels: Global Housing Watch

Wednesday, December 9, 2015

Housing Market in Kuwait

On the policy front, the report says that “Macroprudential tools can help mitigate potential risks posed by banks’ high exposures to the real estate sector. It is important to ensure that macroprudential policies are reviewed constantly to ensure that they do not exacerbate any property price correction, while preempting the buildup of excessive risks related to real estate exposures. (…) House price growth is a core indicator to monitor and the authorities should construct indices for residential properties as well as commercial properties. Also, other indicators, such as both the average and distribution of the LTV and DSTI (DSC) ratio, should be collected and analyzed to adjust macroprudential policy measures properly and swiftly.”

“Prices have shown some signs of softening (…) As of July 2015, prices across the residential and investment property segments have seen average prices fall in year-on-year terms by 6 and 7 percent, respectively (…). As residential prices began to fall in the first half of 2014, average investment property prices began increasing, rising by some 71 percent between March and September. After peaking in September 2014, average investment property prices have fallen by approximately 32 percent as of July 2015. Read the full article…

Posted by at 10:00 AM

Labels: Global Housing Watch

Monday, December 7, 2015

Sweden’s Housing Market

In terms of policies, the report recommends that:

- “Housing supply should be enhanced through land sale and planning reforms, which will also facilitate more competition in residential construction. Rent controls should be eliminated on new rental apartments and phased out more broadly.”

- “Mortgage interest deductibility should be phased out to moderate housing demand over time and limits on capital gains tax deferrals raised to release pent up supply.”

- “A debt-to-income limit should be adopted to contain rises in the already sizable share of highly indebted households, which adds to macroeconomic vulnerabilities.”

A separate IMF report looks at the role of supply constraints in driving prices of owner-occupied housing using municipal-level data.

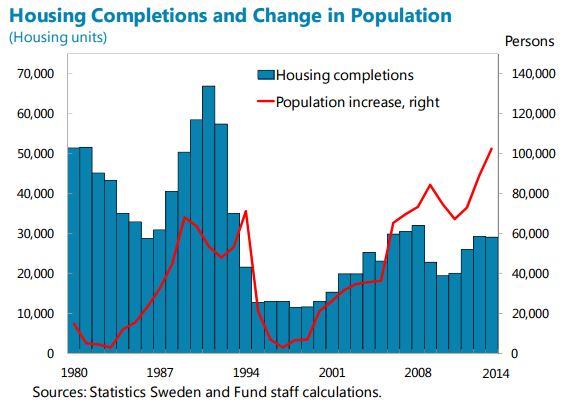

“The housing market shows imbalances, with double-digit price gains as the urban population outpaces construction, pushing up household debt from already high levels. Dwelling price rises accelerated to 16 percent y/y in September, led by apartment price increases exceeding 20 percent in Stockholm and Gothenburg. Housing supply is constrained by construction impediments and rent controls while demand is bolstered by population growth and urbanization, rising income and financial savings, and historically low interest rates. Households need to borrow more at higher house prices, Read the full article…

Posted by at 10:00 AM

Labels: Global Housing Watch

Monday, November 30, 2015

Labor Migration across U.S. States: An Update

A commonly-held view is that when a U.S. state is experiencing tough times (relative to other U.S. states), workers quickly leave the state for greener pastures; this keeps the state’s unemployment rate from going up too much and its labor force participation rate from declining too much.

My new work (with Mai Dao and Davide Furceri) offers a less sanguine view of the ability of U.S. workers to shield themselves from the consequences of adverse shocks. We show that, particularly in the short run, the adjustment to tough times occurs more through unemployment rates going up than through people leaving the state. And while migration picks up during recessions, people in the states that are doing very poorly have a difficult time exiting.

Here is a link to the paper and a technical summary of the paper:

Our first key finding is that labor mobility is less important as a cyclical adjustment mechanism, relative to changes in unemployment and participation, than suggested in earlier work. Some of this shift in view comes from the addition of over 20 years of data to the previous work. But the main reason is that, given the availability of official interstate net-migration data starting in 1991 we can also directly look at the behavior of migration, as opposed to backing it out as a residual. We find that it is primarily the relative unemployment rate, not net migration, that is the main adjustment mechanism in the first two years following a relative shock to state labor demand.

Our second set of findings pertains to a newer literature that documents longer-run movements in U.S. mobility, particularly the steady and widespread reduction in gross internal migration rates since the 1980’s. Here we establish several results that reveal important patterns in regional adjustment mechanisms.

- First, in the last two decades or so starting 1990, the response of net migration to given regional shocks in the short run has decreased, as has the response of relative unemployment and participation rates, resulting in less dispersion of employment growth in response to given dispersion in relative labor demand shocks.

- Second, the smaller migration response to shocks is driven entirely by less net out-migration from states that experience adverse labor demand shifts, whereas the net in-migration response to states with favorable labor demand shifts has increased or remained constant (depending on time horizon). This also suggests that in-migrants to the best states do not disproportionately come from the poorest states, a sign of lack of migration directedness and of scope for efficiency gains from an aggregate perspective.

- Third, despite the trend decline in gross migration rates since the early 1990’s, the migration response to a state-relative demand shock increases strongly in recessions, hence potentially playing a larger role as shock absorber during aggregate downturns than in normal times. Importantly, we observe that this counter-cyclical response of migration is driven primarily by a stronger response of positive net migration into states that do relatively better during recessions, while negative net migration from states that do relatively worse only increases by less and the response is delayed, occurring toward the end of the recession. When a state like North Dakota does relatively better than average during a recession thanks to the shale gas boom, it attracts disproportionately more in-migration than for instance Texas during an expansion, when strong demand for oil creates more jobs in Texas than elsewhere. However, the migrants into North Dakota during the recession do not come disproportionately more from states that are doing worse than average, say Michigan, as one would expect.

A high degree of mobility has long been considered a distinguishing feature of the U.S. labor market.

A commonly-held view is that when a U.S. state is experiencing tough times (relative to other U.S. states), workers quickly leave the state for greener pastures; this keeps the state’s unemployment rate from going up too much and its labor force participation rate from declining too much.

My new work (with Mai Dao and Davide Furceri) offers a less sanguine view of the ability of U.S.

Posted by at 5:12 PM

Labels: Inclusive Growth

Fund Fires Employment Guru?

RG: What was the group set up to do?

Loungani: On jobs, the immediate task was to remind people that sometimes unemployment is high because demand is low. The Fund, like many others, often veers towards thinking of unemployment as largely a supply-side problem—people are lazy or we give them very generous unemployment benefits so they don’t search for jobs or there are structural problems that keep unemployment high. At the onset of the Great Recession, Olivier (Blanchard) and Min (Zhu)—who had oversight over the group—were worried that we would underplay the most obvious explanation for why unemployment had spiked up, namely that aggregate demand had fallen. Our mission was to keep the words “aggregate demand” alive within the building and outside.

RG: Did you succeed?

Loungani: Perhaps more outside the building than within it, at least initially. Under Olivier’s supervision—he gave me a two-page outline and said “follow this”—Mai Dao and I wrote a 2010 paper which Paul Krugman praised: “A recovery in aggregate demand is the single best cure for unemployment. What a relief to hear the IMF say that!” This sentiment was echoed by many others over the ensuing years, including many in the trade union movement. We had a tougher time at other institutions: after one of my presentations in Europe a person came up to me and said: “I heard the same thing from Olivier 30 years ago and I didn’t believe it then.”

RG: And within the Fund building?

Loungani: It has been a tough sell. Larry Ball (of Johns Hopkins), Davide Furceri, Daniel Leigh and I kept up a drumbeat that the short-run relationship between output and unemployment—known as Okun’s Law—had remained stable through the Great Recession. Antonio Spilimbergo started calling us the “Okun police”. I think it eventually started to rub off; one piece of evidence is EUR’s paper on the rise in youth unemployment, which provides an even-handed treatment of the respective roles of aggregate demand and supply factors.

RG: What was the task on growth?

Loungani: Olivier put it as “moving beyond mantras”. Both he and I had the view that the Fund goes to countries and says: “Here are 25 (structural) areas on which you are behind international standards. Improve on all them by next year and you will surely grow”. So I started to look through the Fund’s advice on growth.

RG: What did you find?

Loungani: That the characterization is unfair. Though you can still find examples of the kind I mentioned, the bulk of the Fund’s advice on growth is actually quite ‘granular’; that is, it digs down to see the specific problems the country is facing. Think, for example, of the great work that Patrizia Tumbarello and many other Fund staff have done in providing advice to small states on sustainable growth.

RG: So what did the group do?

Loungani: In the “Jobs & Growth” Board paper, we summarized the current ‘do’s and don’ts’ on growth and then showed that staff had been broadly following that advice. We also issued a very nice guidance note for Fund staff on how to tackle growth issues—I am not praising myself here as this was largely the work of several SPR colleagues. In this case too, as with jobs, we got some external recognition—in this case some back-handed praise from Dani Rodrik, who in the past has been critical of our advice on growth.

RG: And, finally, on inequality?

Loungani: Here the guidance came largely from Min (Zhu), at least initially. Around 2010-11, when the group’s work started, Min was more concerned about inequality than was Olivier. Min said we should see how policies, including Fund policies, affect inequality, so we could take these effects into account in our surveillance and program work.

RG: So does Fund policy advice affect inequality?

Loungani: One of the first things we did was to see how fiscal consolidations—referred to as ‘austerity’ outside our building—affected inequality. In a 2011 piece we found that austerity raises inequality. This initially proved controversial within the building—and, not surprisingly, popular in some circles outside—but management supported us and the paper was published. In 2014, FAD did a very nice Board paper on fiscal policy and inequality and has just issued a new book on the topic. Recently we have shown that openness—capital account liberalization—raises inequality; I hope MCM picks up on this, the way FAD did with fiscal policy. Min also wanted us to see how monetary and exchange rate policies affect inequality; I never got around to it but hope springs eternal—here again MCM could help.

RG: What’s next for you?

Loungani: I have a few residual tasks to complete in the Jobs & Growth agenda. One is to finish extensions of the work on Okun’s Law to emerging markets and low-income countries. The other is to think about the advice the Fund gives to these countries on the design of labor market institutions. This was a topic close to Olivier’s and my hearts; but while Olivier and I did a paper on it for advanced economies (with Florence Jaumotte), I never got around to doing the follow-up paper for other countries. But my main job is to head the division within RES that deals with low-income countries.

RG: And what’s next for the group? Is it disbanded and how would you summarize its impact?

Loungani: Well, my co-chair Ranil Salgado and I have both moved on. But the agenda continues under new management—and the seminar series we launched continues as well. In RES, Romain Duval has taken over and had added structural reforms to the agenda—this is good as the focus we had placed on aggregate demand was appropriate for the time but we should be even-handed. And of course, inequality has become a big deal at the Fund now—with the astounding success of the work by Jonathan Ostry and Andy Berg, the blossoming work on gender inequality, the pilot cases on operationalizating inequality.

On the impact: I suspect Gerry Rice would not call it “huge”. But, in the words of the poet, we managed “to swell a progress, start a scene or two.”

So, did the Fund fire its employment guru? Well, not quite, but after five years at the helm of the Fund’s Jobs & Growth working group, Prakash Loungani is moving on to other assignments. RES GESTAE spoke to him about the group’s travails in promoting the Fund’s work on jobs, growth and equity.

RG: What was the group set up to do?

Loungani: On jobs, the immediate task was to remind people that sometimes unemployment is high because demand is low.

Posted by at 3:33 PM

Labels: Inclusive Growth

Subscribe to: Posts