Thursday, December 22, 2016

Monetary Policy and Inequality

Do the actions of central banks affect inequality? Leading central bankers have been discussing the issue (e.g., Yellen 2014; Bernanke 2015, Draghi 2016) but there is little consensus about the sign and magnitude of the effect. Our new paper documents how monetary policy affects income inequality in 32 advanced economies and emerging market countries over the period of 1990-2013. We find that decline of 100 basis points in the policy interest rate lowers inequality by about 1¼ percent in the short term and by about 2¼ percent in the medium term. The effect is significant and holds for different measures of inequality (Gini coefficient, top income shares and labor share of income). To identify the causal effect of monetary policy shocks on inequality, we borrow from the recent literature on fiscal policy (Auerbach and Gorodnichenko 2013) and construct unexpected changes in policy rates that are orthogonal to innovations in economic activity.

Do the actions of central banks affect inequality? Leading central bankers have been discussing the issue (e.g., Yellen 2014; Bernanke 2015, Draghi 2016) but there is little consensus about the sign and magnitude of the effect. Our new paper documents how monetary policy affects income inequality in 32 advanced economies and emerging market countries over the period of 1990-2013. We find that decline of 100 basis points in the policy interest rate lowers inequality by about 1¼ percent in the short term and by about 2¼ percent in the medium term.

Posted by at 4:55 PM

Labels: Inclusive Growth

Wednesday, December 21, 2016

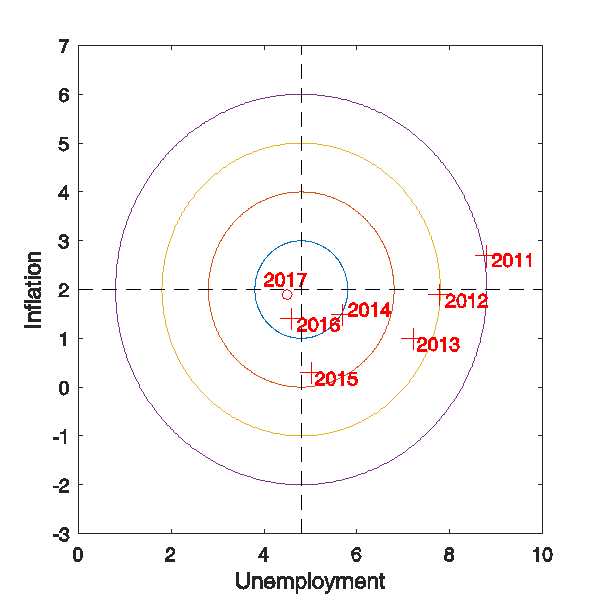

The Fed and the U.S. Economy: Hitting the Bull’s Eye?

Like Jim Hamilton, I like the visual device suggested by my friend and former colleague Charlie Evans (a.k.a. President Evans of the Chicago Fed) of using a bull’s eye to show where the economy is relative to the Fed’s likely targets. Jim’s latest update shows the U.S. economy moving back towards the bull’s eye.

Like Jim Hamilton, I like the visual device suggested by my friend and former colleague Charlie Evans (a.k.a. President Evans of the Chicago Fed) of using a bull’s eye to show where the economy is relative to the Fed’s likely targets. Jim’s latest update shows the U.S. economy moving back towards the bull’s eye.

Posted by at 7:26 AM

Labels: Macro Demystified

Tuesday, December 20, 2016

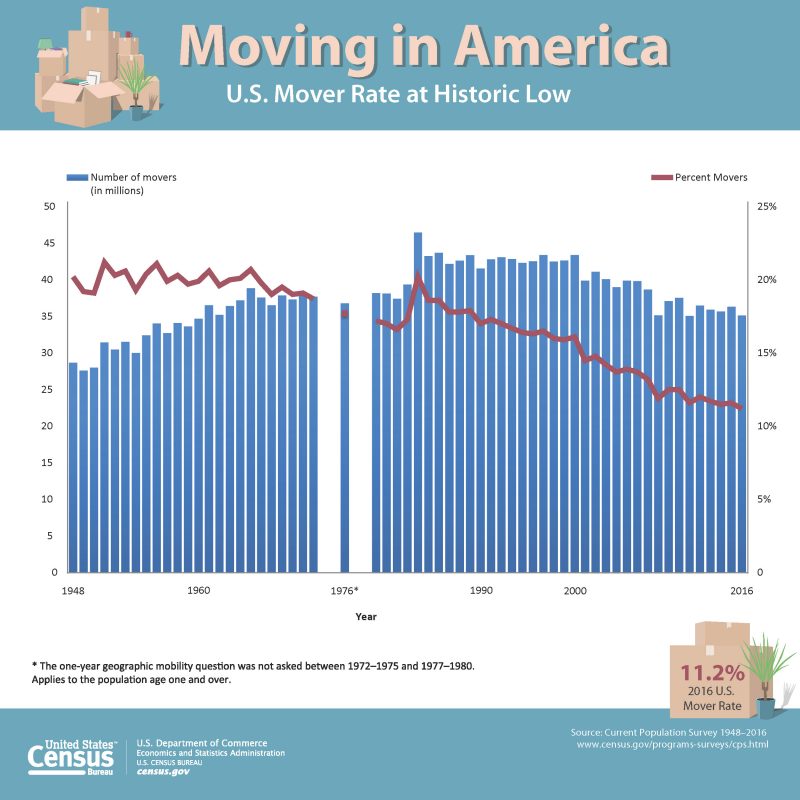

(Not) On The Road Again: Americans Are Moving Less

A nice update by Timothy Taylor on declining labor mobility in the United States and the possible reasons, a topic I have written on as well.

Posted by at 8:44 AM

Labels: Inclusive Growth

Monday, December 19, 2016

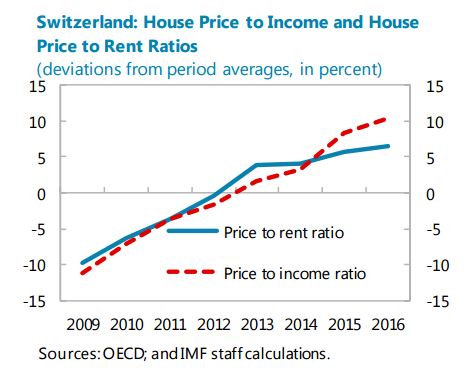

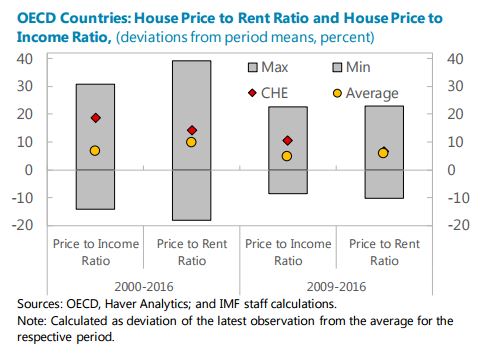

Housing Market in Switzerland

“Elevated exposure to mortgage debt continues, and low interest rates could rekindle a credit-driven upswing in house prices (…) [the authorities should] stand ready to adopt new macroprudential measures if credit and house prices again turn up, with a focus on the build-to-let segment”, says IMF’s latest report on Switzerland.

The report also says that “House prices relative to income have grown significantly since the great recession, and while prices have recently stabilized, price to income ratios remain stretched. Average debt per borrower is very high given the relatively low rate of home ownership. A prompt response will be needed if greater competition in credit markets further bids down interest rates and spurs a resurgence of mortgage lending or an acceleration of house prices. The response should target the build-to-rent segment where activity is currently brisk and where larger risk weights and/or faster amortization relative to owner-occupied properties is appropriate to reflect the international tendency for higher default and loss rates on these loans. Greater recourse to legally-binding regulation in preference to banks’ self-regulation could ensure any needed changes are implemented in timely manner and that uniform standards apply to all mortgage providers”

“Elevated exposure to mortgage debt continues, and low interest rates could rekindle a credit-driven upswing in house prices (…) [the authorities should] stand ready to adopt new macroprudential measures if credit and house prices again turn up, with a focus on the build-to-let segment”, says IMF’s latest report on Switzerland.

The report also says that “House prices relative to income have grown significantly since the great recession,

Posted by at 11:37 AM

Labels: Global Housing Watch

GDP Demystified

Posted by at 8:59 AM

Labels: Macro Demystified

Subscribe to: Posts