Tuesday, February 7, 2017

Okun’s Law: Fit at 50?–Revised Paper and Dataset

Here is a revised version of my paper with Larry Ball and Daniel Leigh and the dataset and programs needed to reproduce the results.

Here is a revised version of my paper with Larry Ball and Daniel Leigh and the dataset and programs needed to reproduce the results.

Posted by at 10:03 AM

Labels: Inclusive Growth

Monday, February 6, 2017

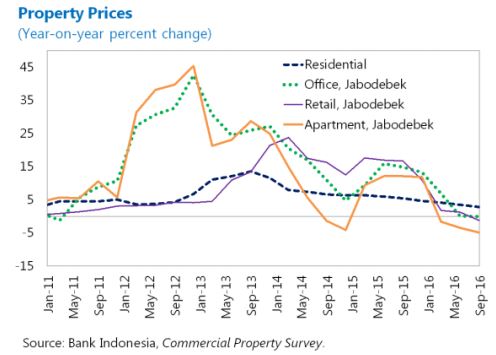

House Prices in Indonesia

“Property prices have been subdued, in tandem with slowing economic growth”, notes IMF’s report on Indonesia.

“Property prices have been subdued, in tandem with slowing economic growth”, notes IMF’s report on Indonesia.

Posted by at 4:10 PM

Labels: Global Housing Watch

Saturday, February 4, 2017

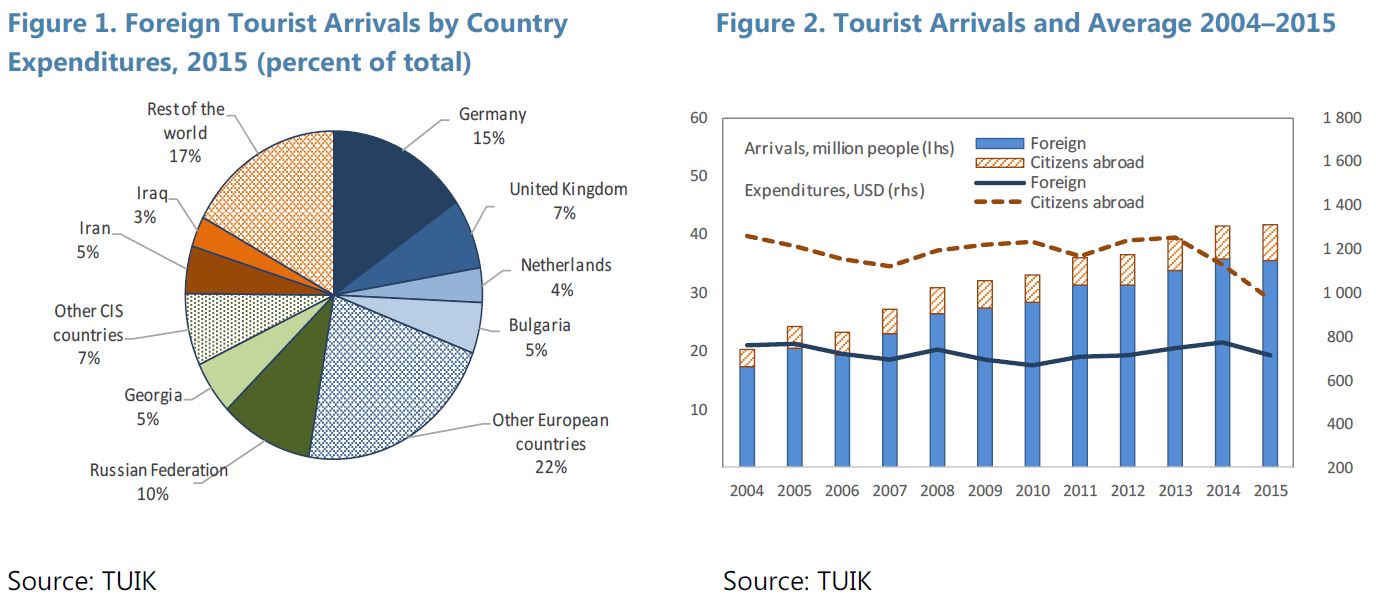

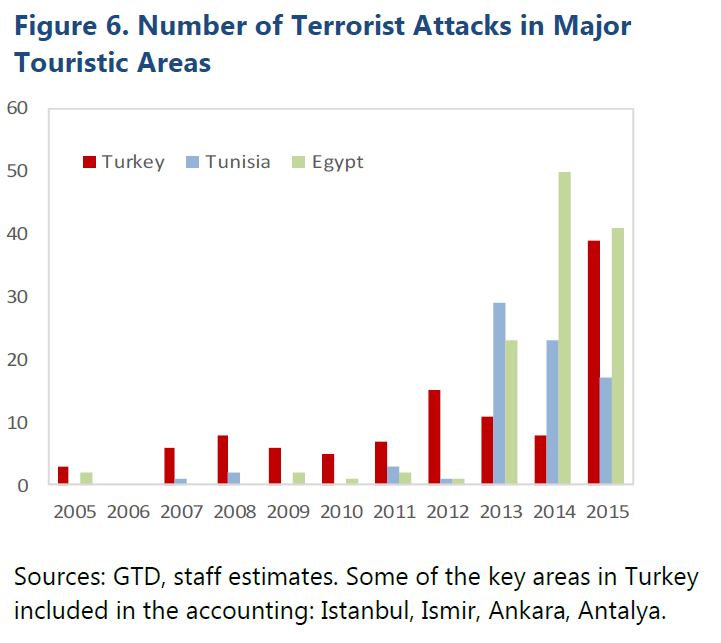

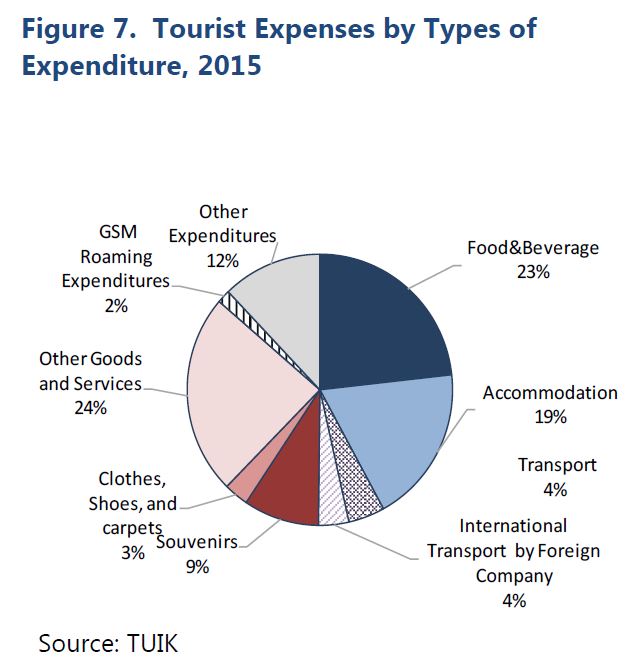

Turkey’s Tourism Sector: Recent Developments and the Impact on the Broader Economy

“After a decade of a vibrant development Turkish tourism sector was hit by a major fall in foreign tourists’ arrivals. This [IMF] study takes stock of recent developments and considers potential spillovers from tourism sector to other parts of the economy. It finds that a negative shock to foreign arrivals had a significant impact on the economic activity in 2016, while the recovery prospects remain subdued”, says IMF report on Turkey.

“After a decade of a vibrant development Turkish tourism sector was hit by a major fall in foreign tourists’ arrivals. This [IMF] study takes stock of recent developments and considers potential spillovers from tourism sector to other parts of the economy. It finds that a negative shock to foreign arrivals had a significant impact on the economic activity in 2016, while the recovery prospects remain subdued”, says IMF report on Turkey.

Posted by at 2:49 PM

Labels: Inclusive Growth

Friday, February 3, 2017

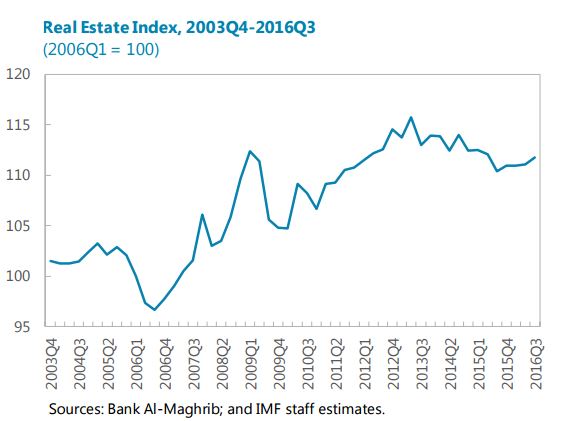

House Prices in Morocco

“Mortgage lending remains moderate (about 5 percent y-o-y) and there is no indication of a housing price bubble”, says IMF’s new report on Morocco.

“Mortgage lending remains moderate (about 5 percent y-o-y) and there is no indication of a housing price bubble”, says IMF’s new report on Morocco.

Posted by at 6:00 PM

Labels: Global Housing Watch

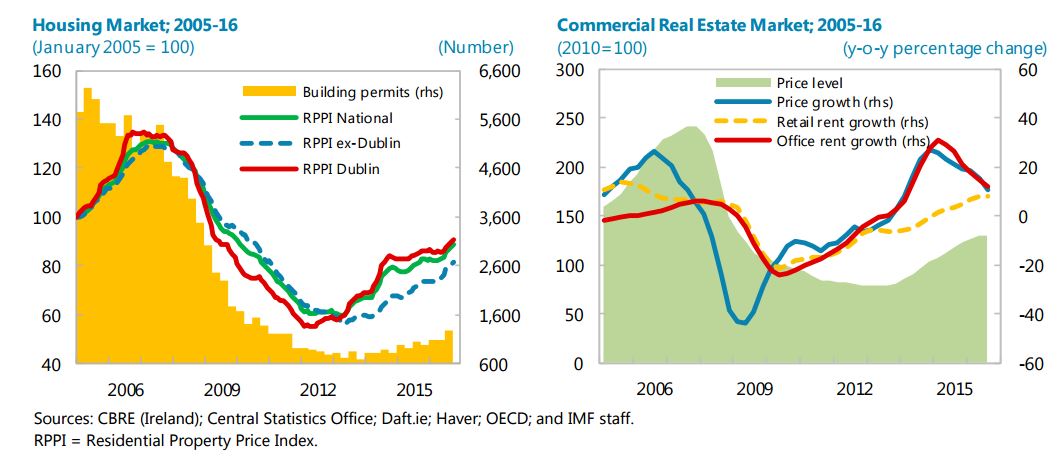

Housing Market in Ireland

The IMF’s report on Ireland says that:

“Property market conditions tightened further, mainly due to a limited supply response. Current conditions have supported robust demand recovery, but housing completions have picked up only moderately, continuing to fall well short of the underlying requirement in the economy. With the stock of properties listed for sale at a nine-year low, house price increases accelerated to 7.1 percent y/y in October 2016. The value of mortgage approvals surged by 43 percent as of November compared to a year earlier, albeit from a relatively low base and in the context of a continued contraction in the stock of outstanding mortgages. Tight housing market conditions have also led to a sharp rise in residential rents, which have now exceeded their pre-crisis peak. In response, the government introduced rental growth caps of 4 percent in Rent Pressure Zones (RPZ) starting in 2017. To ease supply constraints, the government introduced a multipronged Housing Action Plan in July to be implemented over 2017-21 (Annex II). Pressures in the commercial real estate (CRE) market remained strong, and prices increased further, particularly in the office segment. As demand is mostly funded by foreign investors and domestic equity, the exposure of the domestic banking system to the CRE market continued to decline. Despite these pressures, analysis at the time of the 2016 Article IV discussion suggested that current prices are broadly in line with fundamentals in both residential and commercial segments (…).”

On mitigating housing market imbalances, the report says that:

“Efforts to expand and expedite the delivery of housing and rental properties under the Housing Action Plan—a central focus of the current budget—are welcome, particularly those measures directed at mitigating supply constraints. On the contrary, the “Help-to-Buy” (HTB) scheme, set to run through 2019, raises some concerns. While temporary and relatively limited, the program provides only indirect support for supply and carries a relatively high threshold for mortgage value, suggesting scope for better targeting. At the same time, it risks exacerbating demand and pricing pressures. Plans for a phased increase in interest relief for buy-to-let landlords from the current 75 percent to 100 percent by 2021 raise similar concerns. An early review of these fiscal incentives would be warranted to ensure they are well-targeted to assist those most in need and to reduce risks of fueling demand and price pressures. To help address supply bottlenecks, consideration should be given to fasttracking the implementation of a locally levied vacant lot tax, currently expected in 2018, which aims to create incentives to increase land utilization. Administrative measures on rents, however, could dissuade construction and may prove ineffective as landlords could pass on additional costs to tenants through other fees.”

The IMF’s report on Ireland says that:

“Property market conditions tightened further, mainly due to a limited supply response. Current conditions have supported robust demand recovery, but housing completions have picked up only moderately, continuing to fall well short of the underlying requirement in the economy. With the stock of properties listed for sale at a nine-year low, house price increases accelerated to 7.1 percent y/y in October 2016. The value of mortgage approvals surged by 43 percent as of November compared to a year earlier,

Posted by at 6:00 PM

Labels: Global Housing Watch

Subscribe to: Posts