Friday, March 10, 2017

Trade Integration in Latin America and the Caribbean

Below is the executive summary of a new IMF report:

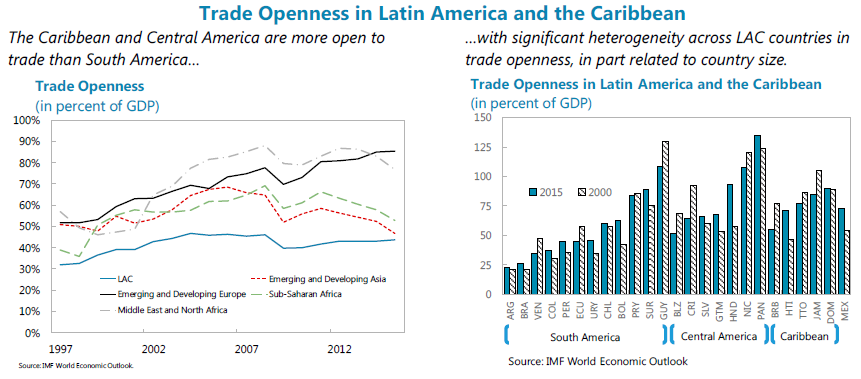

“This cluster report takes stock of and explores opportunities for trade integration in Latin America and the Caribbean (LAC). Drawing on a set of 12 analytical studies that will be issued as working papers, the report examines the determinants of trade, explores the potential to enhance LAC’s trade integration, and assesses the associated economic and social effects. To deepen understanding of the region’s policy options and trade strategies, the report also incorporates the views of LAC country authorities based on responses to a survey. This provides an opportunity to examine the alignment of recommendations based on the analytical findings with the region’s current trade policy priorities, with the caveat that the survey was conducted between late 2015 and mid-2016, prior to the most recent developments in the global trade landscape.

The report finds that LAC can reap important growth benefits from further trade integration. With trade integration below that of other regions, there is scope for LAC to increase trade as an engine of growth and help offset the weaker economic outlook without adversely affecting overall income inequality. While there is potential to enhance both inter- and intra-regional trade integration, renewed political momentum within LAC in support of greater trade openness could provide an important impetus to further intra-regional trade integration in particular. In this context, regional trade integration could be promoted through a regional trade agreement, convergence of trade rules and regulatory standards, and measures to support trade facilitation. Strategies to bolster the region’s inter-regional integration could be centered on unilateral liberalization as a complement to existing efforts to expand LAC’s network of trade agreements.

This report also emphasizes the importance of complementary policies. Continued regional efforts to strengthen infrastructure and human capital would be useful as part of a broad growth strategy. But they can also enhance trade integration, including by facilitating participation in global value chains which may offer new opportunities for technology transfer, and are critical to diversifying and upgrading the complexity of LAC’s exports. Finally, strengthened social safety nets can help lessen adjustment costs linked to further integration and promote an equitable distribution of gains from trade.”

Below is the executive summary of a new IMF report:

“This cluster report takes stock of and explores opportunities for trade integration in Latin America and the Caribbean (LAC). Drawing on a set of 12 analytical studies that will be issued as working papers, the report examines the determinants of trade, explores the potential to enhance LAC’s trade integration, and assesses the associated economic and social effects. To deepen understanding of the region’s policy options and trade strategies,

Posted by at 11:45 AM

Labels: Inclusive Growth

Trade, Growth and Inequality in Latin America and the Caribbean

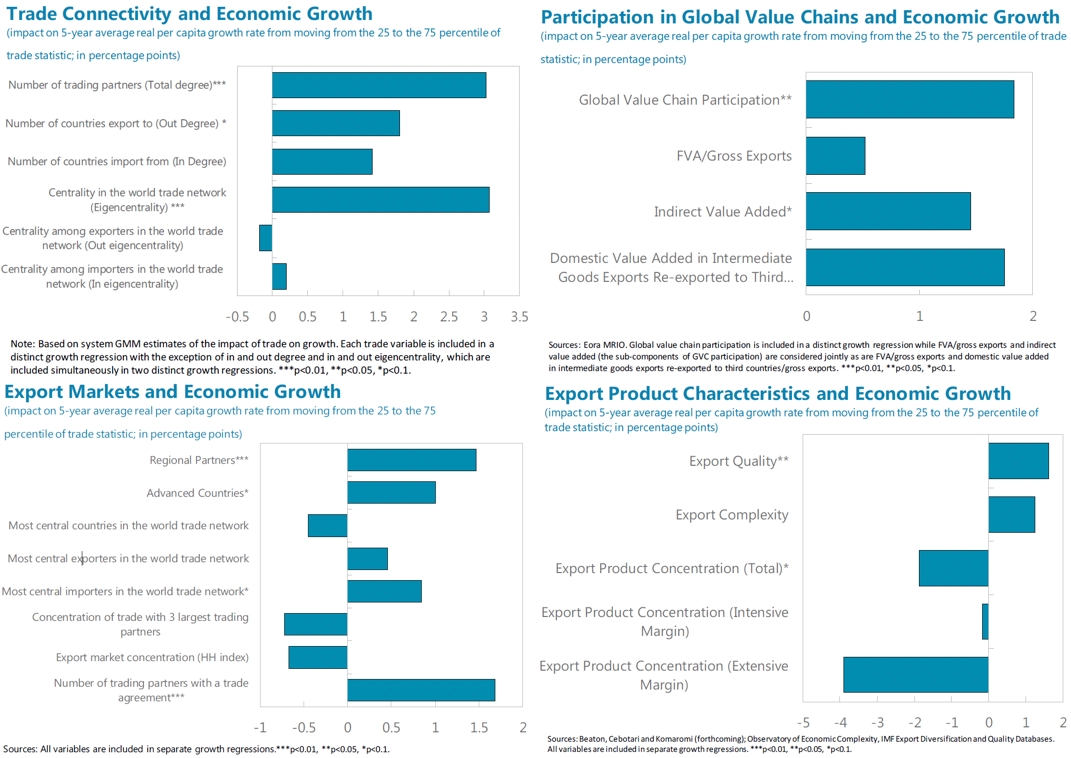

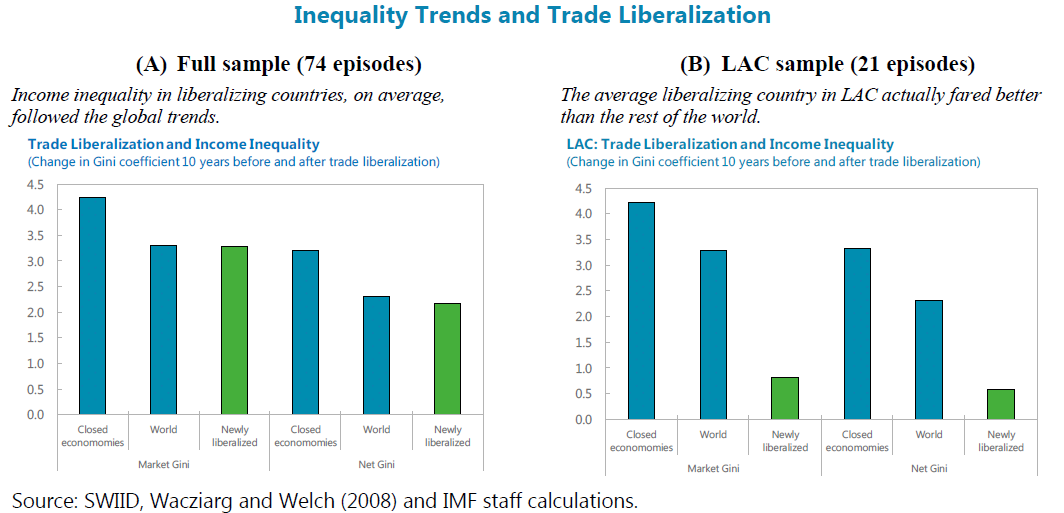

A new IMF working paper studies “the relationship between international trade, economic growth and inequality with a focus on Latin America and the Caribbean. The paper combines two approaches: First, [this paper employs] a cross-country panel framework to analyze the macroeconomic effects of international trade on economic growth and inequality considering the strength of trade connections as well as characteristics of countries’ export markets and products. Second, [this paper considers] event studies of past episodes of trade liberalization to extract general lessons on the impact of trade liberalization on economic growth and its structure and inequality. Both approaches consistently point to two broad messages: First, trade openness and connectivity to the center of the trade network has substantial macroeconomic benefits. Second, [no] statistically significant or economically sizable direct impact of trade on overall income inequality.”

A new IMF working paper studies “the relationship between international trade, economic growth and inequality with a focus on Latin America and the Caribbean. The paper combines two approaches: First, [this paper employs] a cross-country panel framework to analyze the macroeconomic effects of international trade on economic growth and inequality considering the strength of trade connections as well as characteristics of countries’ export markets and products. Second, [this paper considers] event studies of past episodes of trade liberalization to extract general lessons on the impact of trade liberalization on economic growth and its structure and inequality.

Posted by at 11:24 AM

Labels: Inclusive Growth

Monday, March 6, 2017

Global House Prices: An Update

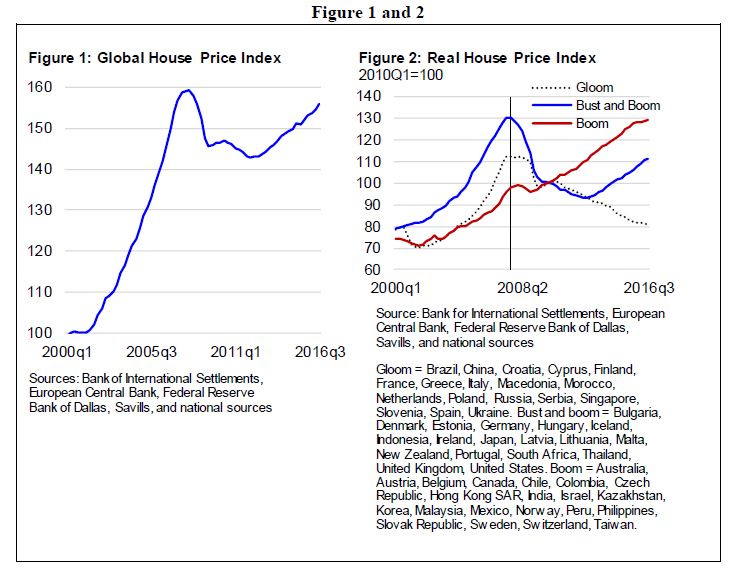

The IMF’s Global House Price Index—an average of real house prices across countries—continued to climb up in the third quarter of 2016 (Figure 1). This is the sixteenth consecutive quarter of positive year-on-year growth in the index. However, house prices are not rising everywhere around the world. As noted in our Q4 2016 Quarterly Update (and as covered in the Wall Street Journal), house price developments in the countries that make up the index fall into three clusters: gloom, bust and boom, and boom (Figure 2).

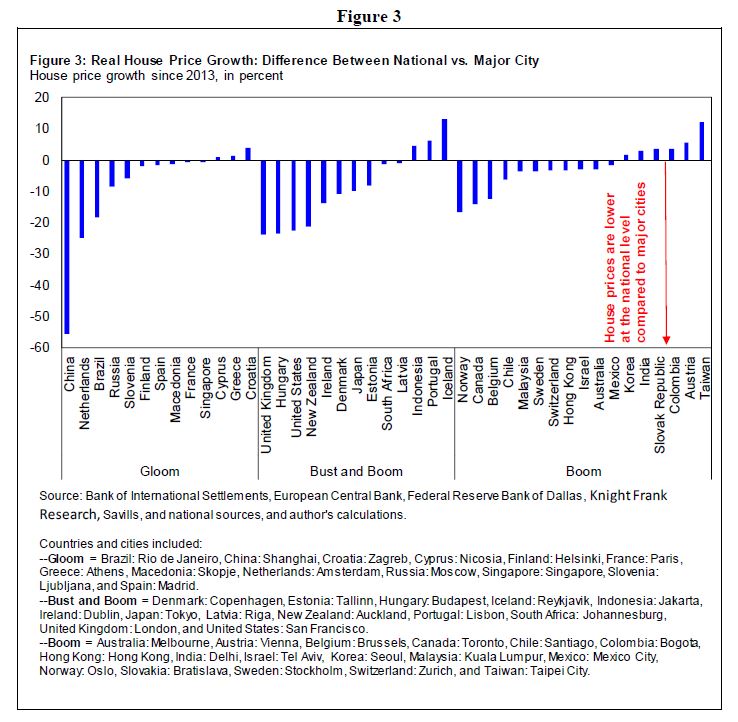

The Q1 2017 Quarterly Update digs a little deeper and shows that house prices are also not climbing up everywhere within countries. Figure 3 shows that in many countries, house prices are subdued at the national level compared to the city level.

Recent IMF assessments provide a more nuanced view of the within country house price developments.

- On Australia, IMF assessment points out that house price gains have moderated. However, the extent of cooling has varied considerably across cities. The strongest price increases continue to be recorded in Sydney and Melbourne, where underlying demand for housing remains strong. With house prices still rising ahead of income, standard valuation metrics suggest somewhat higher house price overvaluation relative to the previous IMF assessment.

- On Austria, IMF assessment notes that the cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna, while prices in the rest of the country appear broadly in line with fundamentals.

- On Turkey, IMF assessment points out that the housing market exhibits significant variations across cities. Regional variations have been further accentuated by the presence of more than 2.7 million Syrian refugees since March 2011. Cities near the Syrian border, which have absorbed larger masses of Syrian refugees have seen significant rises in local housing prices since 2011, though they have moderated in recent years.

The IMF’s Global House Price Index—an average of real house prices across countries—continued to climb up in the third quarter of 2016 (Figure 1). This is the sixteenth consecutive quarter of positive year-on-year growth in the index. However, house prices are not rising everywhere around the world. As noted in our Q4 2016 Quarterly Update (and as covered in the Wall Street Journal), house price developments in the countries that make up the index fall into three clusters: gloom,

Posted by at 9:20 PM

Labels: Global Housing Watch

Thursday, March 2, 2017

Creative Financing for Affordable Housing

From Shaping the Future of Construction: Insights to redesign the industry

by Richard Koss

“Overview

Attracting private capital into programmes for affordable housing has been a long-run challenge in both developed and developing countries. In general, the problem is that purely private capital is incentivized to devote its resources towards the development of high-end properties for upper-income households.

Purely public forms of capital can be brought to bear to support affordable housing construction, but cost control can be a problem without the profit incentive. In addition, public resources are limited, in particular in emerging markets, and can fall far short of the public need. What we see then is the development of many forms of public regulation and partnerships with the private sector in order to meet the affordable housing challenge. While still in early changes, a great deal of institutional and technological innovation is just now being brought to bear on this issue that offers considerable promise in this area, particularly in emerging markets.

Regulation and government-sponsored enterprises

Traditionally, higher-income countries have dealt with the issue of affordable housing via a variety of regulations on financial institutions and public support of income targeted at housing. In terms of regulation, the idea is that financial institutions, notably banks, receive public support through features such as cheap funding through taxpayer-insured deposits. In exchange they should be directed to allocate capital towards affordable housing projects that are expected to be profitable, but not so much as the development of costlier units. In the United States, one such mechanism is the Community Reinvestment Act.

Another approach is the formation of government agencies or government-sponsored enterprises (GSE’s) which support liquidity and affordability to loans directed at lower income homeowners and to developers who build high-quality rental units aimed at lower-income communities. They do so in part by designating balance sheet directly towards these mortgages. In addition, they also set standards and share risk with the private sector through the issuance of mortgage-related securities (MRS). In the US these entities include agencies such as the Federal Housing Agency and the Veterans Administration as well as the housing GSEs Fannie Mae and Freddie Mac. GSEs are tasked to support lower-income housing through sweeping regulation known as the Affordable Housing Goals and the Duties to Serve. Other nations have housing agencies, notably Japan and Canada.

The UK has an innovative programme called Help-to-Buy that allows lower income households to purchase a share of a home (usually 25% – 75%) and pay rent on the rest.

Another affordability policy is income support for lowerincome housing. In the US there is the Low Income Housing Tax Credit Programme (LIHTC).

Another approach which is more local in nature is the requirement that developers who are given rights to build on a piece of land set aside a certain number of units designated as affordable housing. Such programmes are very popular in California where affordability is particularly problematic.

Financing vehicles

Another set of responses to the affordable housing financing challenge can be characterized as “financing vehicles”. These are generally partnerships between private, philanthropic and public entities that bring the efficiency of private capital to bear with credit enhancements provided by government and charities. In general, the returns to private capital are somewhat less than for purely private projects, but the experience is that many private developers are willing to participate in these programmes out of a sense of civic duty and reputation enhancement. There are many classes of such investments that are targeted at different segments of the market. These include below-market debt funds, private equity vehicles and real estate investment trusts (REITs). The Urban Land Institute provides a useful summary of these efforts.

In many cases, the public funds come from regional entities (generally states in the US). These are known as Housing Finance Agencies (HFA’s). The US Treasury lends support to more distressed local communities through entities known as Community Development Financial Institutions (CDFI’s). All-in-all there are many hundreds of such vehicles and structures, revealing great innovative thinking that can be targeted at particular needs in distinct communities. There are far too many to list here, but an example that has received attention is the JP Morgan Partners in Raising Opportunity (PRO) programme that provides funding to CDFI’s across the country.”

Continue reading here.

From Shaping the Future of Construction: Insights to redesign the industry

by Richard Koss

“Overview

Attracting private capital into programmes for affordable housing has been a long-run challenge in both developed and developing countries. In general, the problem is that purely private capital is incentivized to devote its resources towards the development of high-end properties for upper-income households.

Purely public forms of capital can be brought to bear to support affordable housing construction,

Posted by at 2:58 PM

Labels: Global Housing Watch

Shaping the Future of Construction: Insights to redesign the industry

A new White Paper from the World Economic Forum says that:

“While most other industries have undergone tremendous changes over the past few decades and have reaped the benefits of process, product and service innovations, the construction sector has been hesitant to fully embrace the latest innovation opportunities and its labour productivity has stagnated or even decreased over the last 50 years.

This mediocre track record can be attributed to various internal and external challenges: the persistent fragmentation of the industry, inadequate collaboration between the players, the sector’s difficulty in adopting and adapting to new technologies, the difficulties in recruiting a talented and futureready workforce, and insufficient knowledge transfer from project to project, among others.

In the context of the Forum’s Future of Construction initiative, over the past year six Working Groups comprised of industry leaders, academics and experts met regularly to develop and analyse innovative ideas, their impact, the barriers to implementing solutions and the way forward to overcoming obstacles and implementing modern approaches in the construction and engineering industry.

This white paper presents the outcome of this work in the form of insight articles proposing innovative solutions on how to address the construction sector’s key challenges in the following fundamental challenge areas:

- Project Delivery – Creating certainty of timely delivery and to budget, and generally improving the productivity of the construction sector

- Life cycle Performance – Reducing the life cycle costs of assets and designing for re-use

- Sustainability – Achieving carbon-neutral assets and reducing waste in the course of construction

- Affordability – Creating high-quality, affordable infrastructure and housing

- Disaster Resilience – Making infrastructure and buildings resilient to climate change and natural disasters

- Flexibility, Liveability and Well-being – Creating infrastructure and buildings that improve the well-being of end-users”

A new White Paper from the World Economic Forum says that:

“While most other industries have undergone tremendous changes over the past few decades and have reaped the benefits of process, product and service innovations, the construction sector has been hesitant to fully embrace the latest innovation opportunities and its labour productivity has stagnated or even decreased over the last 50 years.

This mediocre track record can be attributed to various internal and external challenges: the persistent fragmentation of the industry,

Posted by at 2:49 PM

Labels: Global Housing Watch

Subscribe to: Posts