Thursday, March 8, 2018

Housing View – March 9, 2018

On cross-country:

- Global House Price Index – Q4 2017 – Knight Frank

- 2018 Emerging Models in Real Estate Report – Mike DelPrete

On the US:

- The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco – NBER

- Shocker! Rent Control Makes Housing Scarcer and More Expensive – Reason

- Eliminating Fannie Mae and Freddie Mac without legislation – American Enterprise Institute

- Income Doesn’t Determine Whether People Buy Homes, for Now – Zillow

- De Blasio Bolsters Affordable Housing, but at What Price? – New York Times

- NYC perseveres with affordable housing agenda despite costly obstacles – Curbed

- Home sales falling in the U.S. – but not for the reason you think – Global Property Guide

- The Rise and Fall of American Public Housing – Citylab

- In California, Momentum Builds for Radical Action on Housing – Citylab

- State and Local Health and Housing Integration Projects – Center on Budget and Policy Priorities

- The mortgage market risk no one’s talking about, plus a proposal to redesign the system – Brookings

On other countries:

- [Germany] Landlords Shed No Tears Over Broken German Housing Market – Wall Street Journal

- [Nambia] House Prices in Namibia – IMF

- [New Zealand] Funding cost pass-through to mortgage rates – Reserve Bank of New Zealand

- [New Zealand] New Zealand to hit property speculators with taxes on capital gains – Global Property Guide

- [Switzerland] That Zurich Lakeside Property May Finally Become More Affordable – Bloomberg

- [United Kingdom] The housing market in the macroeconomy – National Institute of Economic and Social Research

- [United Kingdom] Detailed household expenditure for mortgage-paying households, by gross income quintile group, UK, financial year ending 2015 to financial year ending 2017 – Office for National Statistics

Photo by Aliis Sinisalu

On cross-country:

- Global House Price Index – Q4 2017 – Knight Frank

- 2018 Emerging Models in Real Estate Report – Mike DelPrete

On the US:

- The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco – NBER

- Shocker! Rent Control Makes Housing Scarcer and More Expensive – Reason

- Eliminating Fannie Mae and Freddie Mac without legislation – American Enterprise Institute

- Income Doesn’t Determine Whether People Buy Homes,

Posted by at 2:15 PM

Labels: Global Housing Watch

Wednesday, March 7, 2018

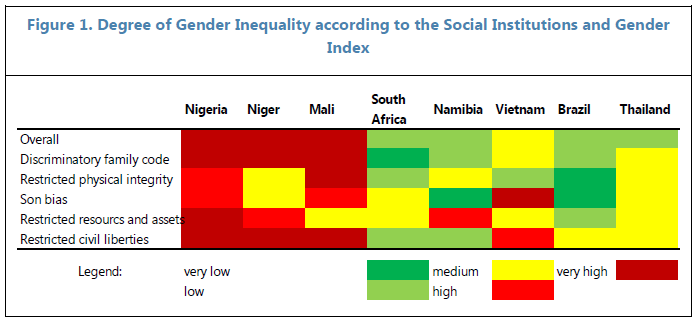

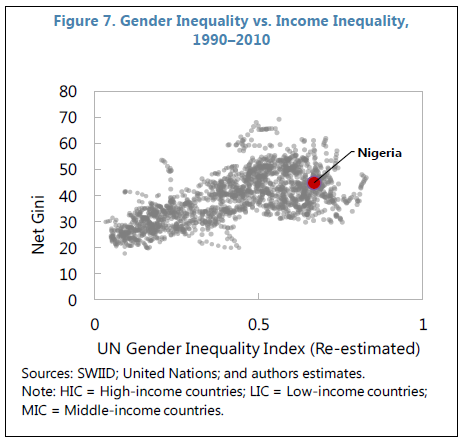

Gender Inequality in Nigeria: Macroeconomic Costs and Future Opportunities

The latest IMF country report finds that “Gender inequality in Nigeria is high and widespread across areas of economic opportunities (enforcement of legal rights; access to education, health, financial services) and outcomes (labor force participation, entrepreneurship, political representation, income). These inequalities have led to substantial macroeconomic losses in terms of growth, income equality, and economic diversification. Nigeria’s real GDP per capita growth could, on average, be higher by 1¼ percentage points annually if gender inequality was reduced to that of peers in the region. Addressing challenges in health and education, such as by providing necessary infrastructure (sanitation facilities and electricity), equalizing legal rights, and combatting violence against women and girls, will be essential for Nigeria to reap the demographic dividend from its young and rapidly growing population.”

The latest IMF country report finds that “Gender inequality in Nigeria is high and widespread across areas of economic opportunities (enforcement of legal rights; access to education, health, financial services) and outcomes (labor force participation, entrepreneurship, political representation, income). These inequalities have led to substantial macroeconomic losses in terms of growth, income equality, and economic diversification. Nigeria’s real GDP per capita growth could, on average, be higher by 1¼ percentage points annually if gender inequality was reduced to that of peers in the region.

Posted by at 11:25 AM

Labels: Inclusive Growth

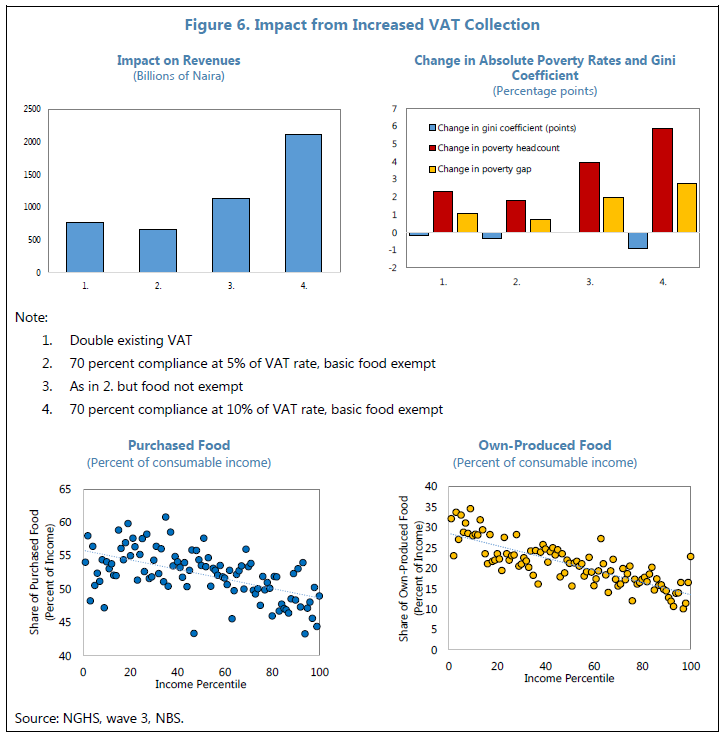

Distributional Impact of Fiscal Reforms in Nigeria

The latest IMF country report on Nigeria finds that “Income inequality and poverty rates are high in Nigeria, with the latter having declined more slowly compared to other countries. At the same time, moving closer to achieving the sustainable development goals and addressing Nigeria’s large development needs will require additional financing. This chapter finds that reforms to generate fiscal space—increases in value-added tax collection, excises, and electricity tariffs—are progressive, i.e. they reduce income inequality. However, they increase poverty gaps and rates to varying extents. Scaling up social safety net transfers and expanding their scope to cover a wider share of the poor can, to some extent, compensate for these adverse impacts at relatively low cost, and bring down poverty rates more generally. In the short term, other measures to shield vulnerable households’ income, including through lifeline electricity tariffs, and higher spending on health and education are needed.”

The latest IMF country report on Nigeria finds that “Income inequality and poverty rates are high in Nigeria, with the latter having declined more slowly compared to other countries. At the same time, moving closer to achieving the sustainable development goals and addressing Nigeria’s large development needs will require additional financing. This chapter finds that reforms to generate fiscal space—increases in value-added tax collection, excises, and electricity tariffs—are progressive, i.e. they reduce income inequality.

Posted by at 11:20 AM

Labels: Inclusive Growth

Tuesday, March 6, 2018

IMF Paper Looks at How Inflation Anchoring Affects Growth

My new paper with Sangyup Choi and Davide Furceri has been featured the Central Banking:

“A working paper published by the International Monetary Fund has concluded anchoring inflation expectations – rather than the level of inflation – is what has a statistical effect on growth.

In their paper, Sangyup Choi, Davide Furceri, and Prakash Loungani explore whether low inflation and the anchoring of inflation expectations are positive for economic growth, as central bankers often assert.

While they find inflation anchoring fosters growth in industries that are more credit-constrained, the authors also attempt to “disentangle” the effect of inflation anchoring from the effect of the level of inflation.

Using data on sectoral growth for 36 advanced and emerging market economies from 1990–2014, the authors “explicitly” control for interactions between “the level of inflation and industry-specific measures of credit constraints”.

“While these two channels tend to be correlated, since low inflation is often achieved by better inflation anchoring … the results of the analysis suggest that it is inflation anchoring and not the level of inflation per se that has a statistical effect on growth,” they say.”

My new paper with Sangyup Choi and Davide Furceri has been featured the Central Banking:

“A working paper published by the International Monetary Fund has concluded anchoring inflation expectations – rather than the level of inflation – is what has a statistical effect on growth.

In their paper, Sangyup Choi, Davide Furceri, and Prakash Loungani explore whether low inflation and the anchoring of inflation expectations are positive for economic growth,

Posted by at 8:57 AM

Labels: Inclusive Growth

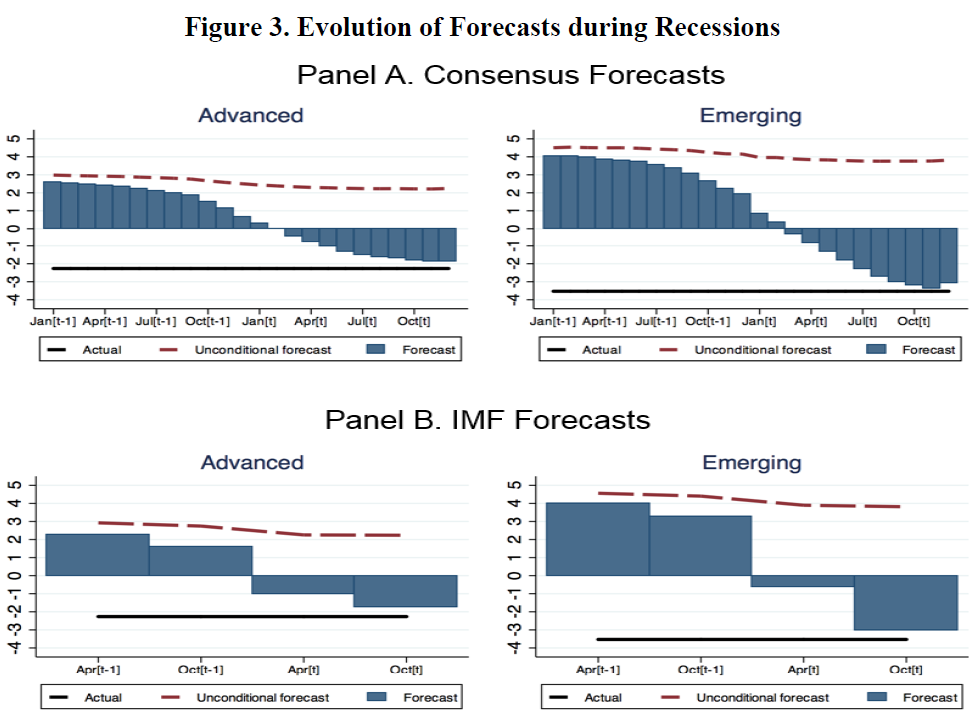

How Well Do Economists Forecast Recessions?

In my latest IMF working paper with Zidong An and Joao Jalles, “We describe the evolution of forecasts in the run-up to recessions. The GDP forecasts cover 63 countries for the years 1992 to 2014. The main finding is that, while forecasters are generally aware that recession years will be different from other years, they miss the magnitude of the recession by a wide margin until the year is almost over. Forecasts during non-recession years are revised slowly; in recession years, the pace of revision picks up but not sufficiently to avoid large forecast errors. Our second finding is that forecasts of the private sector and the official sector are virtually identical; thus, both are equally good at missing recessions. Strong booms are also missed, providing suggestive evidence for Nordhaus’ (1987) view that behavioral factors—the reluctance to absorb either good or bad news—play a role in the evolution of forecasts.”

In my latest IMF working paper with Zidong An and Joao Jalles, “We describe the evolution of forecasts in the run-up to recessions. The GDP forecasts cover 63 countries for the years 1992 to 2014. The main finding is that, while forecasters are generally aware that recession years will be different from other years, they miss the magnitude of the recession by a wide margin until the year is almost over.

Posted by at 8:38 AM

Labels: Forecasting Forum

Subscribe to: Posts