Saturday, June 30, 2018

The Irish Commercial Real Estate Market: Synchronization and the Role of External Factors

The IMF’s latest report on Ireland says that:

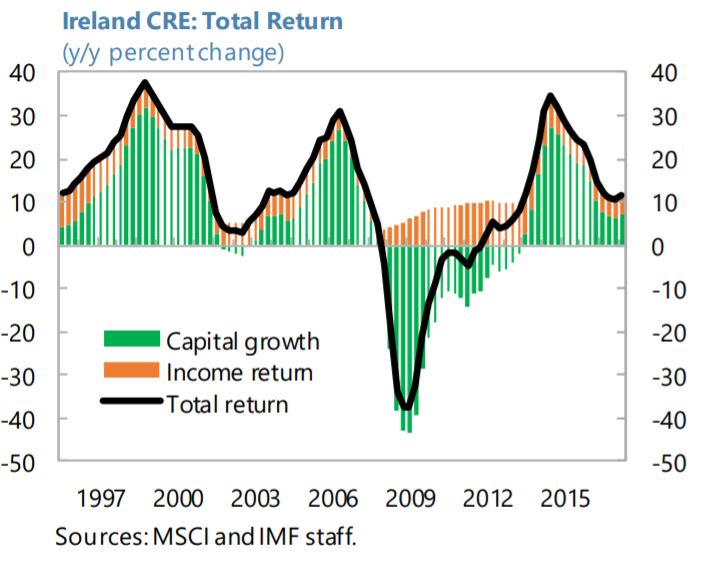

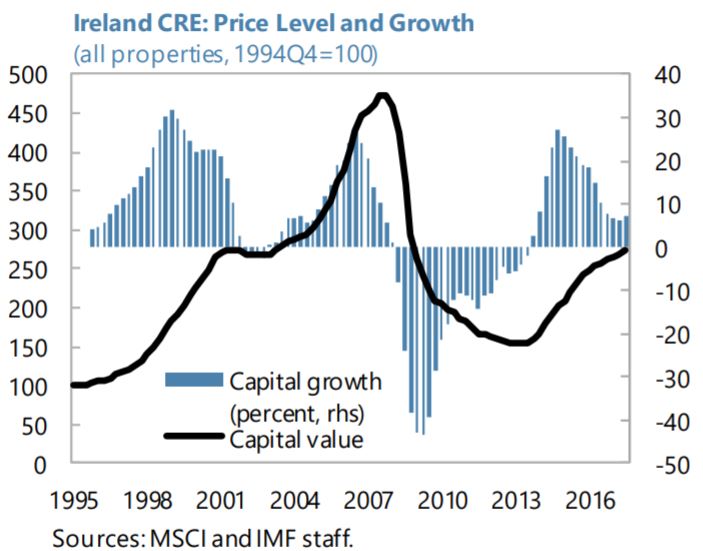

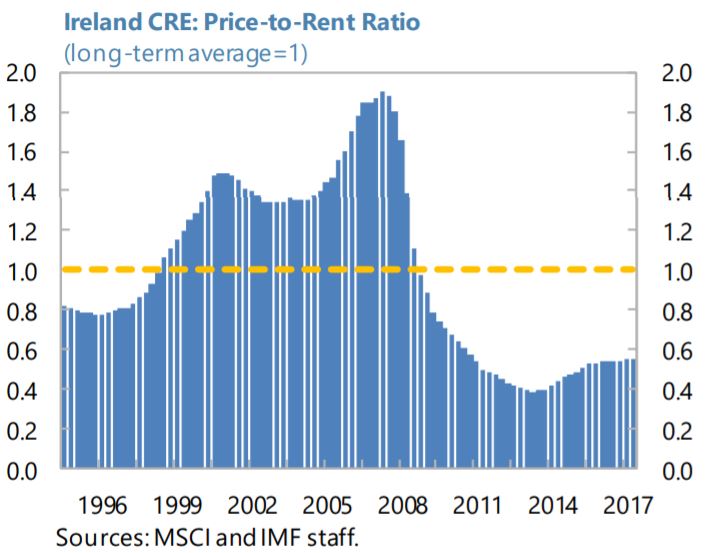

“This chapter examines the synchronization of the Irish returns on commercial real estate (CRE) properties with those in peers to better understand the importance of external factors in explaining the high volatility of CRE returns in recent years. The analysis finds that the cyclical pattern of Irish CRE returns is highly corelated with that in other advanced economies, yet with much higher volatility. Moreover, a vector auto-regression (VAR) analysis points to a high impact of international CRE prices on Irish CRE prices, and to strong feedback effects between the latter and domestic economic activity. These findings underline the importance of continued close monitoring of this market to ensure that the financial system is resilient to possible drops in collateral values and investment flows.”

The IMF’s latest report on Ireland says that:

“This chapter examines the synchronization of the Irish returns on commercial real estate (CRE) properties with those in peers to better understand the importance of external factors in explaining the high volatility of CRE returns in recent years. The analysis finds that the cyclical pattern of Irish CRE returns is highly corelated with that in other advanced economies, yet with much higher volatility.

Posted by at 6:23 AM

Labels: Global Housing Watch

Housing Market in Czech Republic

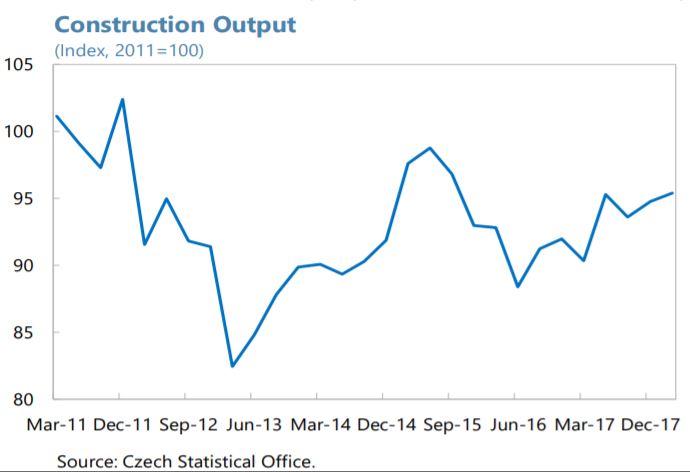

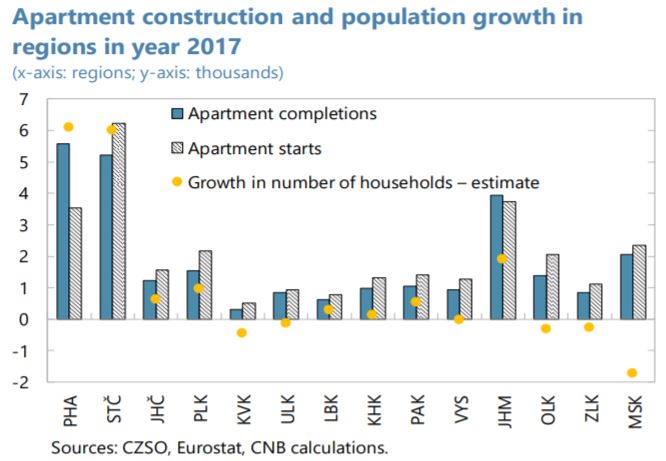

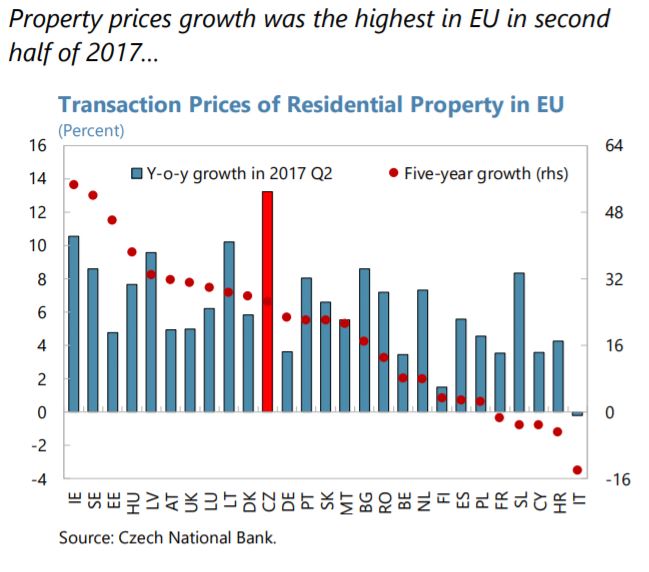

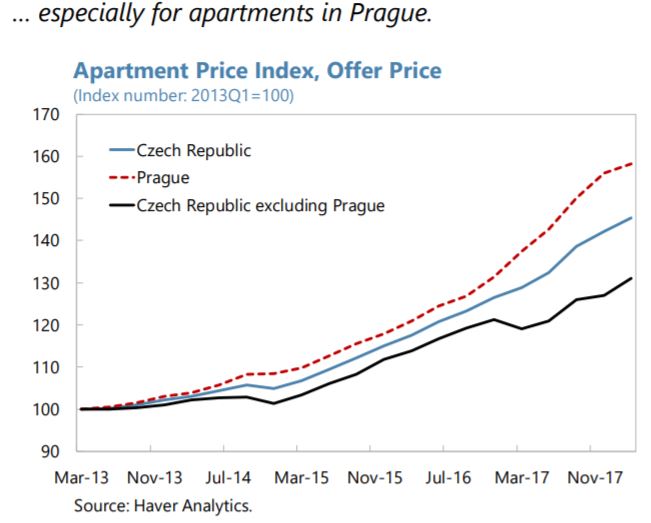

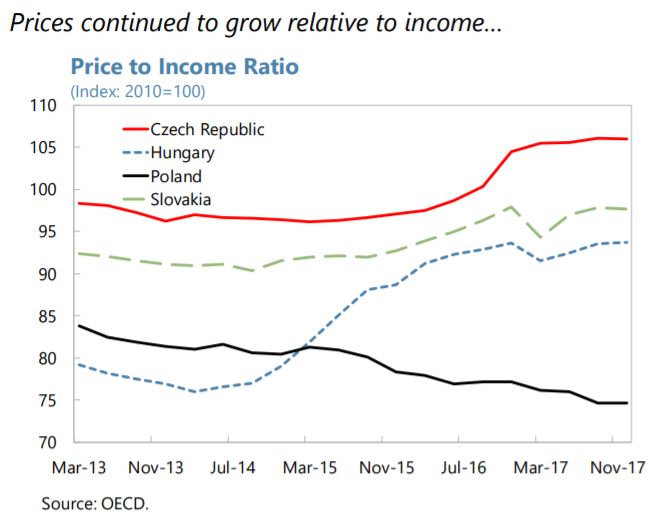

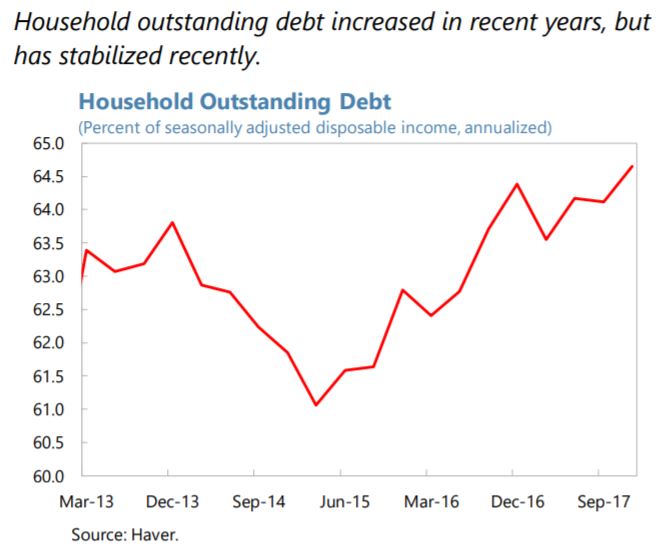

The IMF’s latest report on Czech Republic says that:

“Construction activity declined after the financial crisis and has yet to recover to levels seen in 2009. The effect is particularly noticeable in Prague, for which housing completions have not kept pace with housing demand. Low numbers of housing starts imply that the problem will continue for some time. Demand has been driven mainly by migration within the country and strong demand for prime properties by foreigners; demand for investment properties is also believed to play a significant role.”

The report also says that:

“Private credit growth is in line with nominal GDP growth, but household lending is growing more quickly. Bank lending to residents eased to 4 percent (y/y) in April, of which loans to

resident non-financial corporations grew by only 1½ percent. However, loans to households

increased by 7½ percent; mortgage loans to households increased by 9½ percent, off the recent peak in mid-2017 of 10½ percent, but nonetheless outpacing nominal income growth. Consumer credit also grew relatively strongly.Some households are highly leveraged. The aggregate household debt-to-income (DTI)

ratio has not increased further over the year, given the strong growth of disposable income. But many households continue to borrow at high loan-to-income multiples (…), associated with escalating price-to-income and price-to-rent ratios (…).The CNB has tightened macroprudential recommendations (…). New, non-binding

recommendations implemented in 2017: Q2 included a 90 percent LTV cap on individual loans and a 15 percent cap on the share of new loans originated with LTV ratios between 80 and 90 percent. In June 2017, the CNB recommended that banks pay extra attention to debt-to-income and debt service-to-income ratios. Reported lending standards have subsequently tightened, and the share of new household mortgage loans with LTVs above 90 percent has declined, with many loans at around 80 percent LTV. However, concerns were expressed that this improvement may have been flattered by inflated valuations.Additional measures are needed to insure against household financial vulnerabilities. DTI ratios on new mortgages are only indirectly addressed by LTV restrictions—to safeguard

household finances, the financial authority needs more comprehensive tools and access to data sufficient for a comprehensive picture of households’ finances.

- The CNB should be given binding powers over maximum LTV, DTI, and Debt-Service-To-Income (DSTI) ratios as soon as possible. Debt-based measures would provide a more comprehensive assessment of financial risks than loan-based measures, and are increasingly standard in advanced economies. In the absence of legislation granting binding powers, the CNB should immediately issue recommendations over DTI and DSTI ratios, to reinforce those over LTVs and better target high leverage.

- If such “demand side” (i.e. borrower-based) tools are not implemented, additional “supply side” measures could be considered, but these would only indirectly address the underlying problem of high household leverage. Risk weight add-ons or minimum risk weights for property exposures could provide insurance against growing real estate exposures, but a substantial increase would likely be required to make a meaningful difference to lending conditions, given that capital ratios are above regulatory requirements. The CNB has discretion over capital requirements under Pillar II, but it is not guaranteed that the effects would “pass through” to mortgage borrowers.

Better data are needed for monitoring risks. The use of DTI and DSTI measures puts great

demands on data—to accurately assess risks and to be fully sure of compliance, the CNB needs access to comprehensive household loan data. Better data on commercial real estate transactions would also be helpful.Macroprudential measures should be supported by addressing fiscal and structural

policies. Increasing house prices in major metropolitan areas reflects equilibrium adjustment, and demand has consistently outstripped supply, especially in Prague. Planning and zoning laws contribute to housing supply constraints that add to pressures on prices. Some progress has been made in streamlining procedures for building permits, but construction levels remain below pre-crisis highs (…). In addition, the tax environment adds to housing demand (…). Without attention to such problems, the housing market is likely to remain tight.”

The IMF’s latest report on Czech Republic says that:

“Construction activity declined after the financial crisis and has yet to recover to levels seen in 2009. The effect is particularly noticeable in Prague, for which housing completions have not kept pace with housing demand. Low numbers of housing starts imply that the problem will continue for some time. Demand has been driven mainly by migration within the country and strong demand for prime properties by foreigners;

Posted by at 6:15 AM

Labels: Global Housing Watch

Friday, June 29, 2018

Housing View – June 29, 2018

On cross-country:

- Vivienda en Centroamérica – Instituto Centroamericano de Administración de Empresas (INCAE), CNN

- ‘Livability & Affordability in the Digitized City’ – Housing Europe

- Using evidence to make affordable housing a more attractive investment – Housing Europe

- The digitalisation of cities and housing: what will the future bring? – Sociology Lens

On the US:

- The State of the Nation’s Housing 2018 – Joint Center for Housing Studies

- Housing in the U.S. is too expensive, too cheap, and just right. It depends on where you live. – Brookings

- The big business of housing immigrant children – CNN

- Housing Inventory Tracking – Calculating Risk

- How Is Technology Changing the Mortgage Market? – Federal Reserve Bank of New York

- S. Housing Will Get Even Less Affordable – Bloomberg

- Fed’s Bostic to Hear Case for Excluding Housing From Inflation – Bloomberg

- BankThink FHFA needs to curb Fannie and Freddie’s insatiable appetites – American Banker

On other countries:

- [Canada] Nothing ‘nefarious’ about foreign-buyer tax: B.C. gov’t lawyer – Vancouver Sun

- [China] Why China Can’t Fix Its Housing Bubble – Bloomberg

- [France] Macron pone en jaque el modelo de vivienda social en Francia – El Salto

- [New Zealand] As Housing Prices Soar, New Zealand Tackles a Surge in Homelessness – New York Times

- [Nigeria] Nigerian Low-Cost Mortgage Lender Set for $1.4 Billion Boost – Bloomberg

- [Portugal] Portugal property boom accelerates in first quarter – Reuters

- [Singapore] Singapore Millennials Prefer Property – Bloomberg

- [Sweden] Giddy property prices are a test for Swedish policymakers – The Economist

- [United Arab Emirates] Dubai: To Build or not to Build? – REIDIN

- [United Kingdom] House prices tumble in seaside hot spots – BBC

- [United Kingdom] Buy-to-let landlords cool on property purchases – Financial Times

- [United Kingdom] Not in my back yard — conflicting views on the housing shortage – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Vivienda en Centroamérica – Instituto Centroamericano de Administración de Empresas (INCAE), CNN

- ‘Livability & Affordability in the Digitized City’ – Housing Europe

- Using evidence to make affordable housing a more attractive investment – Housing Europe

- The digitalisation of cities and housing: what will the future bring? – Sociology Lens

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 28, 2018

Fiscal Policy and the Shifting Goalposts

From a new paper by Antonio Fatas:

“This paper studies the negative loop created by the interaction between pessimistic estimates of potential output and the effects of fiscal policy during the 2008-2014 period in Europe. The crisis of 2008 created an overly pessimistic view on potential output among policy makers that led to a large adjustment in fiscal policy during the years that followed. Contractionary fiscal policy, via hysteresis effects, caused a reduction in potential output that not only validated the original pessimistic forecasts, but also led to a second round of fiscal consolidation. This succession of contractionary fiscal policies was likely self-defeating for many European countries. The negative effects on GDP caused more damage to the sustainability of debt than the benefits of the budgetary adjustments. The paper concludes by discussing alternative frameworks for fiscal policy that could potentially avoid this negative loop in future crises.”

From a new paper by Antonio Fatas:

“This paper studies the negative loop created by the interaction between pessimistic estimates of potential output and the effects of fiscal policy during the 2008-2014 period in Europe. The crisis of 2008 created an overly pessimistic view on potential output among policy makers that led to a large adjustment in fiscal policy during the years that followed. Contractionary fiscal policy, via hysteresis effects, caused a reduction in potential output that not only validated the original pessimistic forecasts,

Posted by at 9:42 AM

Labels: Inclusive Growth

Fiscal Stimulus in a Monetary Union: Evidence from Eurozone Regions

From a new IMF working paper:

“This paper contributes to the open economy local fiscal multiplier literature by estimating regional output and employment responses to federal expenditure shocks in the European Union. In particular, similarly to the literature on foreign aid and growth, I use shocks to the supply of federal transfers (European Commission commitments) of structural fund spending by subnational region as instruments for annual realized expenditure in a panel from 2000-2013. I find a large, contemporaneous multiplier of 1.7 which translates into a cumulative multiplier of 4 three years after the shock. Furthermore, using a novel dataset on bilateral trade between EU regions, I find evidence of demand-driven spillovers up to three years after a shock.”

From a new IMF working paper:

“This paper contributes to the open economy local fiscal multiplier literature by estimating regional output and employment responses to federal expenditure shocks in the European Union. In particular, similarly to the literature on foreign aid and growth, I use shocks to the supply of federal transfers (European Commission commitments) of structural fund spending by subnational region as instruments for annual realized expenditure in a panel from 2000-2013.

Posted by at 9:39 AM

Labels: Inclusive Growth

Subscribe to: Posts