Friday, October 19, 2018

Do Remittances Help Growth? A Lebanon Story

From a new post by Timothy Taylor:

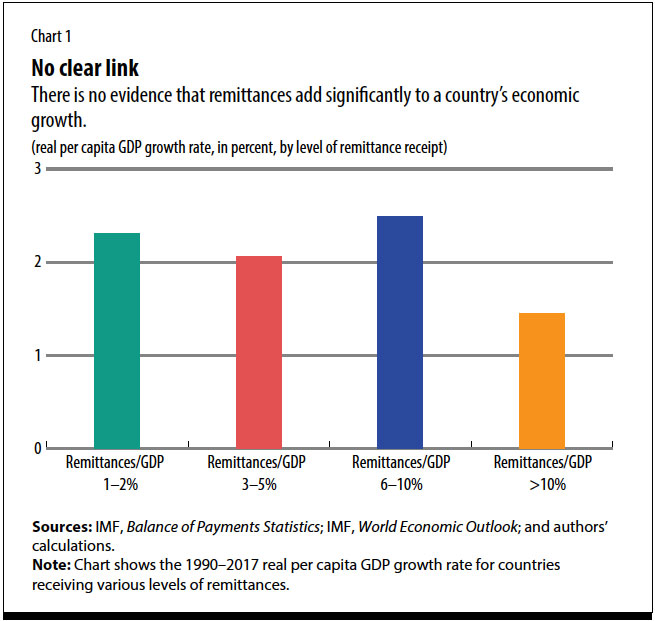

“Remittances are money sent back to a home country by emigrants. On a global basis, remittances to developing countries topped $400 billion in 2017, far exceeding foreign aid to those countries, similar in size to flows of loans and equity investment in those countries, and beginning to approach the level of foreign direct investment in those countries.”

These inflows of funds are clearly helpful to the recipient families, helping to boost and to smooth their consumption. But do they help to boost overall economic growth for the recipient country? Ralph Chami, Ekkehard Ernst, Connel Fullenkamp, and Anne Oeking raise doubts in “Is There a Remittance Trap? High levels of remittances can spark a vicious cycle of economic stagnation and dependence,” published in Finance & Development (September 2018, pp. 44-47). This short and readable article draws on insights from their IMF working paper, “Are Remittances Good for Labor Markets in LICs, MICs and Fragile States? Evidence from Cross-Country Data” (May 9, 2018).

The authors point out that at a big picture level, countries that receive more remittances (as a share of GDP) don’t seem to grow faster. They offer the intriguing example of Lebanon”

Continue reading paper here.

From a new post by Timothy Taylor:

“Remittances are money sent back to a home country by emigrants. On a global basis, remittances to developing countries topped $400 billion in 2017, far exceeding foreign aid to those countries, similar in size to flows of loans and equity investment in those countries, and beginning to approach the level of foreign direct investment in those countries.”

These inflows of funds are clearly helpful to the recipient families,

Posted by at 10:55 AM

Labels: Inclusive Growth

When the Market Drives you Crazy: Stock Market Returns and Fatal Car Accidents

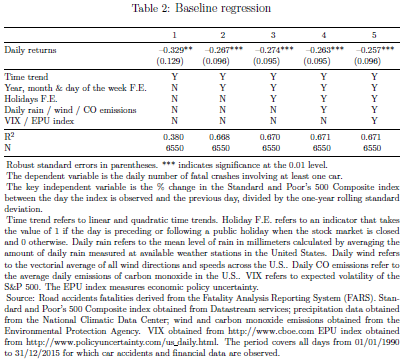

From a new CESifo working paper:

“The stock market influences some of the most fundamental economic decisions of investors, such as consumption, saving, and labor supply, through the financial wealth channel. This paper provides evidence that daily fluctuations in the stock market have important – and hitherto neglected – spillover effects in another, unrelated domain, namely driving. Using the universe of fatal road car accidents in the United States from 1990 to 2015, we find that a one standard deviation reduction in daily stock market returns is associated with a 0.5% increase in the number of fatal accidents. A battery of falsification tests support a causal interpretation of this finding. Our results are consistent with immediate emotions stirred by a negative stock market performance influencing the number of fatal accidents, in particular among inexperienced investors, thus highlighting the broader economic and social consequences of stock market fluctuations.”

From a new CESifo working paper:

“The stock market influences some of the most fundamental economic decisions of investors, such as consumption, saving, and labor supply, through the financial wealth channel. This paper provides evidence that daily fluctuations in the stock market have important – and hitherto neglected – spillover effects in another, unrelated domain, namely driving. Using the universe of fatal road car accidents in the United States from 1990 to 2015,

Posted by at 10:41 AM

Labels: Macro Demystified

More evidence that it’s really hard to ‘beat the market’

According to Mark Perry of Carpe Diem: “over the last 15 years from June 30, 2003 to June 30, 2018, only one in 13 large-cap managers, only one in 21 mid-cap managers, and one in 43 small-cap managers were able to outperform their benchmark index. So it is possible for some active fund managers to “beat the market” over various time horizons, although there’s no guarantee that they will continue to do so in the future. And the percentage of active managers who do beat the market is usually pretty small – fewer than 8% in most of the cases above over the last 15 years; and they may not sustain that performance in the future.”

Read the full story here, which gives a link to the underlying study.

According to Mark Perry of Carpe Diem: “over the last 15 years from June 30, 2003 to June 30, 2018, only one in 13 large-cap managers, only one in 21 mid-cap managers, and one in 43 small-cap managers were able to outperform their benchmark index. So it is possible for some active fund managers to “beat the market” over various time horizons, although there’s no guarantee that they will continue to do so in the future.

Posted by at 10:36 AM

Labels: Macro Demystified

Housing View – October 19, 2018

On cross-country:

- Homeownership motivation, rationality, and housing prices: Evidence from gloom, boom, and bust‐and‐boom economies – International Journal of Finance & Economics

On the US:

- Assessing Housing Risk – Money and Banking

- Local regulatory responses during a regional housing shortage: An analysis of rezonings in Silicon Valley – Land Use Policy

- HUD can’t fix exclusionary zoning by withholding CDBG funds – Brookings

- Housing Market Is Raising Serious Red Flags – Bloomberg

- Promoting Luxury Housing with an Ironic Twist – Institute for Policy Studies

- Homebuilding Isn’t What It Used to Be – Bloomberg

- Reconciling the back to the city thesis with sustained suburban growth – Harvard Joint Center for Housing Studies

- Airbnb and Neighborhood Conflict – Cato Institute

- Slower Growth Anticipated in Home Remodeling – Harvard Joint Center for Housing Studies

On other countries:

- [Austria] Austrian Housing Policy – Dublin Economics

- [Canada] Condo Flippers Aren’t the Vancouver and Toronto Housing Culprits – Bloomberg

- [China] China homeowners stage protests over falling prices – Financial Times

- [United Kingdom] No, the housing crisis will not be solved by building more homes – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Homeownership motivation, rationality, and housing prices: Evidence from gloom, boom, and bust‐and‐boom economies – International Journal of Finance & Economics

On the US:

- Assessing Housing Risk – Money and Banking

- Local regulatory responses during a regional housing shortage: An analysis of rezonings in Silicon Valley – Land Use Policy

- HUD can’t fix exclusionary zoning by withholding CDBG funds – Brookings

- Housing Market Is Raising Serious Red Flags – Bloomberg

- Promoting Luxury Housing with an Ironic Twist – Institute for Policy Studies

- Homebuilding Isn’t What It Used to Be – Bloomberg

- Reconciling the back to the city thesis with sustained suburban growth – Harvard Joint Center for Housing Studies

- Airbnb and Neighborhood Conflict – Cato Institute

- Slower Growth Anticipated in Home Remodeling – Harvard Joint Center for Housing Studies

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, October 18, 2018

Highlights of the Economic Outlook for the Euro Area

From the Economic Outlook for the Euro Area in 2018 and 2019:

“Signs of a slowing world economy are piling up: Since the beginning of the year purchasing manager indices have been declining globally, in summer higher US interest rates led investors to withdraw capital from emerging markets, and as a consequence, capital costs rose and currencies depreciated in many emerging markets economies. In October stock prices decreased markedly worldwide including the US, despite the strong upswing in this country.

As a consequence of the turmoil on financial markets, monetary conditions in many emerging economies are no longer favorable. What ultimately counts for the prospects of the global economy, is, however, the performance of the US, the Euro area, China and Japan. The upswing in the US appears stable enough to continue well into 2019. While at present the rest of the group appears to lose momentum, there is a good chance that production in each of these economies will still expand at rates that are close to their potential growth. Further protectionist rounds are the most important risk to this scenario.”

“In the first half of the current year the euro area economy expanded at a markedly slower rate than in 2017, about 0.4% per quarter, but still substantial. Rising risk premia on Italian assets will probably force banks in this large country to tighten credit conditions, and a slowing world trade will dent export growth. All in all, we expect GDP growth in the euro area to go down from 2.4% in 2017 to 2.0% in 2018 and to 1.7% in 2019.”

“Employment continues to expand and vacancy rates are at present higher than in 2017. As a consequence, wages rise more quickly: nominal compensations per employee started accelerating early in 2017, and negotiated wages followed at the beginning of 2018. Wage inflation of slightly below 2.5% and healthy growth in employment raise real labor incomes markedly.

Our forecasts are based on the assumption that rating agencies will continue as-signing investment grade to the Italian government debt, and that the Italian government and the European Commission will find a compromise about the draft budget of the country in the coming weeks. Another assumption is that the UK will not exit the EU in an unorderly way in March 2019”

From the Economic Outlook for the Euro Area in 2018 and 2019:

“Signs of a slowing world economy are piling up: Since the beginning of the year purchasing manager indices have been declining globally, in summer higher US interest rates led investors to withdraw capital from emerging markets, and as a consequence, capital costs rose and currencies depreciated in many emerging markets economies. In October stock prices decreased markedly worldwide including the US,

Posted by at 5:32 PM

Labels: Forecasting Forum

Subscribe to: Posts