Monday, August 27, 2018

Counting the Oil Money and the Elderly: Norway’s Public Sector Balance Sheet

A new IMF working paper by Ezequiel Cabezon and Christian Henn says:

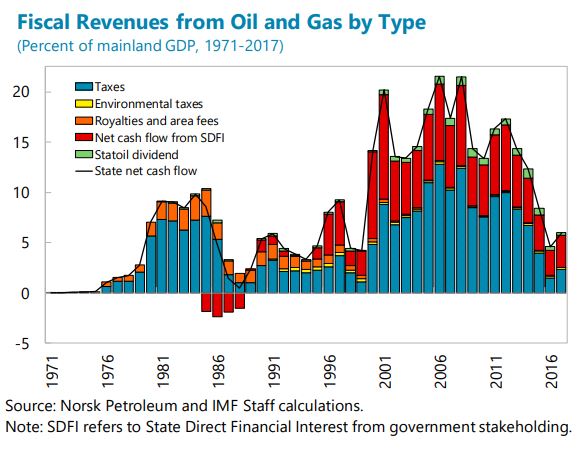

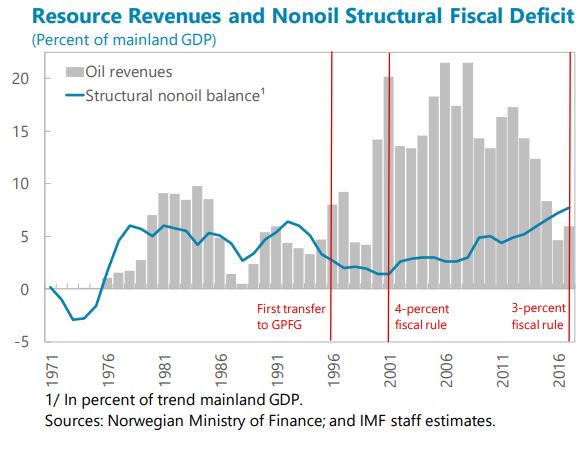

“Based on a permanent income analysis, Gagnon (2018) has prominently suggested that Norway has saved too much, thereby free-riding on the rest of the world for demand. Our public sector balance sheet analysis comes to the opposite conclusion, chiefly because it also accounts for future aging costs. Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP. But its nonoil fiscal deficits have grown very large (to almost 8 percent of mainland GDP) and aging pressures are only commencing. Therefore, Norway’s intertemporal financial net worth (IFNW) is negative, at about -240 percent of mainland GDP. As IFNW represents an intertemporal budget constraint, this implies that Norway’s savings are likely insufficient to address aging costs without additional fiscal action.”

A new IMF working paper by Ezequiel Cabezon and Christian Henn says:

“Based on a permanent income analysis, Gagnon (2018) has prominently suggested that Norway has saved too much, thereby free-riding on the rest of the world for demand. Our public sector balance sheet analysis comes to the opposite conclusion, chiefly because it also accounts for future aging costs. Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP.

Posted by at 1:50 PM

Labels: Global Housing Watch, Inclusive Growth

The Economic Impact of Policies to Boost the Employment of Saudi Nationals

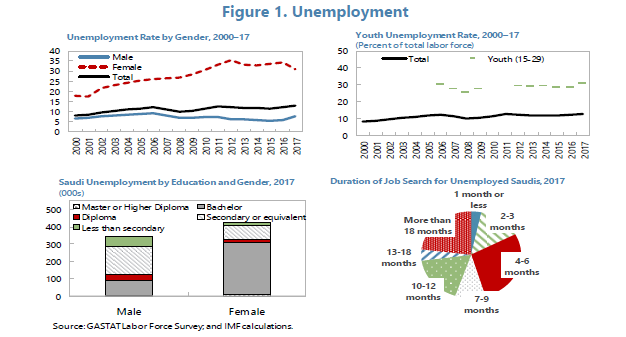

A new IMF country report says that “Saudi Arabia’s labor market is characterized by a persistently high unemployment rate, low private employment ratio, and a low labor participation rate for nationals. The authorities are undertaking a wide range of labor market interventions to address these issues. The analysis in this paper shows that these interventions are helping to reduce distortions in the labor market, including by boosting female labor force participation and reducing the wage gap between expatriates and nationals in the private sector, but the impact on the rest of the economy is not always positive as firms adjust to the higher cost of labor. Reforms should therefore be gradual to minimize their impact on growth. A comprehensive set of policies is also needed to foster job creation for nationals. Measures should include policies toward levelling the playing field between national and expatriate workers so that employers have less of a preference for employing expatriates, setting clear expectations about the limited prospects for public sector employment, boosting female labor force participation, and strengthening education and training to support increased productivity of nationals.”

A new IMF country report says that “Saudi Arabia’s labor market is characterized by a persistently high unemployment rate, low private employment ratio, and a low labor participation rate for nationals. The authorities are undertaking a wide range of labor market interventions to address these issues. The analysis in this paper shows that these interventions are helping to reduce distortions in the labor market, including by boosting female labor force participation and reducing the wage gap between expatriates and nationals in the private sector,

Posted by at 9:51 AM

Labels: Inclusive Growth

Friday, August 24, 2018

Housing View – August 24, 2018

On cross-country:

- Manufacturing decline reduces house price volatility – VOX

- How does the US-China trade war impact China’s real state market and beyond? – Knight Frank

- Tres estudios universitarios muestran que las plataformas de alquiler turístico han encarecido el mercado del alquiler en ciudades como Los Ángeles y Boston – El Pais

On the US:

- What’s up with housing investment? – Rutgers Center for Real Estate

- The Bipartisan Cry of ‘Not in My Backyard’ – New York Times

- Housing Is Back, But the American Dream Isn’t – Bloomberg

- Are More Adults Sharing Housing? – Harvard Joint Center for Housing Studies

- When the Federal Government Takes on Local Zoning – CityLab

- Where Black Homeownership Is the Norm – The Pew Charitable Trusts

- How HUD Can Help the Housing Market – Wall Street Journal

- Foreclosure Starts Increase in 44 Percent of U.S. Markets in July 2018 – ATTOM

- Investigating Metro-Area Home Improvement Spending Cycles – Harvard Joint Center for Housing Studies

- The rebounding mortgage market, in three charts – Urban Institute

On other countries:

- [Australia] That unfolding Australian house price crash – Financial Times

- [China] China Property: Monthly Report – Foresight

- [New Zealand] Will banning foreign buyers solve homelessness in New Zealand? – Reuters

Photo by Aliis Sinisalu

On cross-country:

- Manufacturing decline reduces house price volatility – VOX

- How does the US-China trade war impact China’s real state market and beyond? – Knight Frank

- Tres estudios universitarios muestran que las plataformas de alquiler turístico han encarecido el mercado del alquiler en ciudades como Los Ángeles y Boston – El Pais

On the US:

- What’s up with housing investment?

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, August 22, 2018

Credit Supply and Housing Speculation

From Atif Mian and Amir Sufi at VoxEU:

“Charles P. Kindleberger wrote that “asset price bubbles depend on the growth in credit”. This column looks at the acceleration of the US private label mortgage securitisation market in the US in the late summer of 2003, which disproportionately reduced the cost of financing by lenders that did not traditionally rely on deposit financing for mortgage lending. The sharp rise in lending in zip codes with greater exposure to such lenders generated a boom and bust in house prices. Easier credit also appears to have been a crucial ingredient in explaining bubble cities that experienced both house price and construction booms.

Charles P. Kindleberger, who was the world’s leading expert on financial crises, wrote that “asset price bubbles depend on the growth in credit” (Kindleberger and Aliber 2005). Nobel prize winner Vernon Smith described evidence from experimental settings showing that that the size of a bubble increased when individuals were allowed to borrow (Porter and Smith 1994). Economic theorists have taken this lesson to heart, writing down models in which easier credit helps fuel asset prices through an increase in speculative buying (Allen and Gorton 1993, Allen and Gale 2000).

A core idea in the theory of credit and bubbles is that easier credit allows optimists with high asset valuations to aggressively buy assets, and therefore boost the price (Geanakoplos 2010, Simsek 2013). Even if optimists form a small part of the overall population, easier credit can allow this small group to have a large effect on the market. Further, if the optimists suddenly lose access to credit, the price of the asset will collapse before more pessimistic individuals can be induced to buy the asset. As a result, fluctuations in credit availability increase the amplitude of fluctuations in asset prices.

Our recent study tests this idea, focusing on the boom and bust in house prices from 2000 to 2010 in the US (Mian and Sufi 2018). The study focuses on a natural experiment: the sudden acceleration of the private label mortgage securitisation (PLS) market in the late summer of 2003. The sudden rise in the PLS market, which was part of the broader global rise in shadow banking during this period, disproportionately reduced the cost of financing by lenders that did not traditionally rely on deposit financing for mortgage lending. The study shows that lenders who traditionally relied on non-deposit financing, such as CountryWide and Ameriquest Mortgage Company, suddenly boosted mortgage lending in the late summer of 2003, just as the PLS market accelerated.

To test the effect of this sudden increase in credit availability on the housing market, we exploit variation across geographic areas in the US in the location of these lenders as of 2002. Zip codes where lenders traditionally relied on non-deposit financing witnessed a sudden and large relative increase in mortgage lending just as the PLS market accelerated in 2003. Our study shows several results that suggest this is a clean experiment – the sudden and large expansion of mortgage lending in these zip codes was due to the acceleration of the PLS market, as opposed to some other factor such as a change in income prospects or beliefs about house prices among those living in these zip codes.”

Continue reading here.

From Atif Mian and Amir Sufi at VoxEU:

“Charles P. Kindleberger wrote that “asset price bubbles depend on the growth in credit”. This column looks at the acceleration of the US private label mortgage securitisation market in the US in the late summer of 2003, which disproportionately reduced the cost of financing by lenders that did not traditionally rely on deposit financing for mortgage lending. The sharp rise in lending in zip codes with greater exposure to such lenders generated a boom and bust in house prices.

Posted by at 9:12 AM

Labels: Global Housing Watch

Tuesday, August 21, 2018

Victories Against Air Pollution

From a new post by Timothy Taylor:

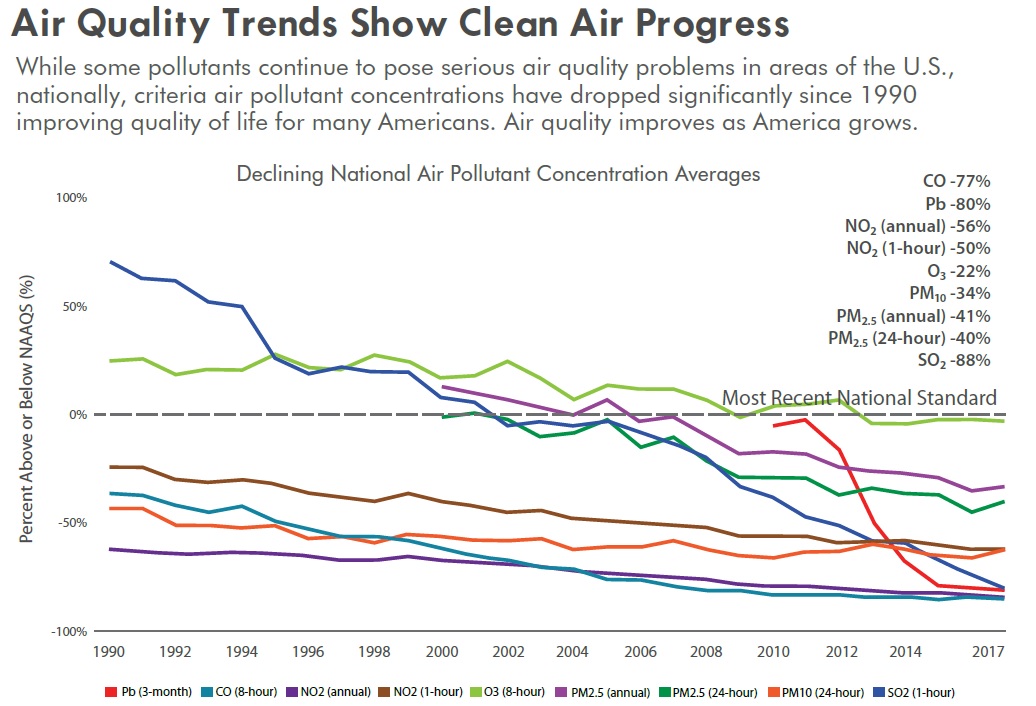

“There is a certain kind of environmentalist who seems unable to acknowledge any good news about the environment, because it might create complacency about remaining issues. I’m not a fan of this approach. When successes are denied, credibility diminishes. And if there’s never been an environmental success to celebrate, I’m more likely to be discouraged about the future than energized. In that spirit, here are some figures from an Environment Protection Agency annual report, Our Nation’s Air.”

“This figure shows the decline in what are often called the “criteria” air pollutants. The horizontal line shows the U.S. National Ambient Air Quality Standards. At a national level, all of the pollutants are below the dashed line. The percentages in the upper right corner of the figure show the decline in the concentration of each category of air pollution since 1990s.”

From a new post by Timothy Taylor:

“There is a certain kind of environmentalist who seems unable to acknowledge any good news about the environment, because it might create complacency about remaining issues. I’m not a fan of this approach. When successes are denied, credibility diminishes. And if there’s never been an environmental success to celebrate, I’m more likely to be discouraged about the future than energized. In that spirit,

Posted by at 5:58 PM

Labels: Energy & Climate Change

Subscribe to: Posts