Friday, March 22, 2019

Housing View – March 22, 2019

On cross-country:

- The Total Risk Premium Puzzle – NBER

- Book review: Order without Design: How Markets Shape Cities by Alain Bertaud – New Geography

- New driveway? Home improvements lead AI to hidden gentrification – Reuters

- Inclusionary Housing Policies in Gothenburg, Sweden, and Stuttgart, Germany: The importance of Norms and Institutions – Nordic Journal of Surveying and Real Estate Research

- We don’t have enough to buy a house. How can we invest with similar returns to real estate? – Globe and Mail

On the US:

- The Fed has exacerbated America’s new housing bubble – Financial Times

- The Affordable Home Crisis Continues, But Bold New Plans May Help – Citylab

- US new home sales fall more than forecast in January – Financial Times

- RE Lending Risks Monitor – Federal Reserve Bank of San Francisco

- Do Credit Conditions Move House Prices? – MIT

- Mortgage Loss Severities: What Keeps Them So High? – Federal Reserve Bank of Philadelphia

- Part 3: Renting Vs. Buying. How Important Is Owning A Home? – wbur

- Bay Area leads charge on fixing housing crisis. Will it work for the rest of California? – Los Angeles Times

- Storper Challenges Blanket Upzoning as Solution to Housing Crisis – UCLA

- How Do Homeowners Spend Their Remodeling Dollars? – Harvard Joint Center for Housing Studies

On other countries:

- [Australia] Property, Debt and Financial Stability – Reserve Bank of Australia

- [Australia] Australia’s falling home prices not yet a threat to banks: RBA – Reuters

- [Australia] Australian Housing Slide Deepens as RBA Worries About Consumers – Bloomberg

- [Australia] Australia’s Housing Slump Isn’t Fazing Mortgage Bond Investors – Bloomberg

- [Australia] How Do Crime Rates Affect Property Prices? – Infrastructure Victoria

- [Australia] Foreign investment in Australian residential properties: House prices and growth of housing construction sector – University of Technology, Melbourne

- [Canada] The Age of Leverage – Bank of Canada

- [Canada] Previous housing data understated amount of non-resident buyers in Vancouver and Toronto – Globe and Mail

- [Canada] Trudeau Targets Home-Buying Millennials With Equity Plan – Bloomberg

- [Canada] Not in my neighbour’s back yard? Laneway homes and neighbours’ property values – University of British Columbia

- [China] Housing Policy and Economic Growth in China – Reserve Bank of Australia

- [China] Deeper Cracks in China’s Housing Foundations – Wall Street Journal

- [China] China new house prices pick up pace in February – Financial Times

- [Czech Republic] Czech apartment price rise continues – ING

- [Iceland] Iceland’s house prices rises decelerating rapidly – Global Property Guide

- [India] As property prices rise, more Indian women claim inheritance – Reuters

- [Ireland] Irish house prices cool further as wider inflation remains muted – Reuters

- [Italy] Renaissance Venice had its own “Airbnb problem”—and a solution … – Quartz

- [Japan] Japan’s Regional Land Prices Rise for First Time Since Property Bubble Burst in ’90s – Bloomberg

- [Malaysia] Housing prices in peninsular Malaysia: supported by income, foreign inflow or speculation? – Tunku Abdul Rahman University College

- [Mexico] Mexico’s housing market is strengthening – Global Property Guide

- [Netherlands] Amsterdam Is Trying to Crack Down on Its Rentals Market – Bloomberg

- [Slovak Republic] Slovak Republic’s house price rises continue – Global Property Guide

- [Switzerland] World’s Lowest Interest Rate Brews Trouble for Swiss Property – Bloomberg

- [United Kingdom] Revealed: the fastest ‘double your money’ years for UK property – Financial Times

- [United Kingdom] Properties, prices and pesky Instagrammers – Financial Times

- [United Kingdom] Elephant and Castle shifts from social housing to ‘build to rent’ – Financial Times

- [United Kingdom] How does the land supply system affect the business of UK speculative housebuilding? – UK Collaborative Centre for Housing Evidence

- [Venezuela] Crisis en Venezuela: la tentadora oferta de viviendas de lujo a precio de saldo (y qué tiene que ver el “efecto Guaidó”) – BBC

On cross-country:

- The Total Risk Premium Puzzle – NBER

- Book review: Order without Design: How Markets Shape Cities by Alain Bertaud – New Geography

- New driveway? Home improvements lead AI to hidden gentrification – Reuters

- Inclusionary Housing Policies in Gothenburg, Sweden, and Stuttgart, Germany: The importance of Norms and Institutions – Nordic Journal of Surveying and Real Estate Research

- We don’t have enough to buy a house.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, March 20, 2019

Fundamental and Speculative Demands for Housing

From a new IMF working paper by Weicheng Lian:

“This paper separates the roles of demand for housing services and belief about future house prices in a house price cycle, by utilizing a feature of user-cost-of-housing that it is sensitive to demand for housing services only. Optimality conditions of producing housing services determine user-cost-of-housing and the elasticity of substitution between land and structures in producing housing services. I find that the impact of demand for housing services on house prices is amplified by a small elasticity of substitution, and demand explained four fifths of the U.S. house price boom in the 2000s.”

From a new IMF working paper by Weicheng Lian:

“This paper separates the roles of demand for housing services and belief about future house prices in a house price cycle, by utilizing a feature of user-cost-of-housing that it is sensitive to demand for housing services only. Optimality conditions of producing housing services determine user-cost-of-housing and the elasticity of substitution between land and structures in producing housing services. I find that the impact of demand for housing services on house prices is amplified by a small elasticity of substitution,

Posted by at 9:03 AM

Labels: Global Housing Watch

Tuesday, March 19, 2019

The Total Risk Premium Puzzle

From a new NBER paper by Òscar Jordà, Moritz Schularick, Alan M. Taylor:

“The risk premium puzzle is worse than you think. Using a new database for the U.S. and 15 other advanced economies from 1870 to the present that includes housing as well as equity returns (to capture the full risky capital portfolio of the representative agent), standard calculations using returns to total wealth and consumption show that: housing returns in the long run are comparable to those of equities, and yet housing returns have lower volatility and lower covariance with consumption growth than equities. The same applies to a weighted total-wealth portfolio, and over a range of horizons. As a result, the implied risk aversion parameters for housing wealth and total wealth are even larger than those for equities, often by a factor of 2 or more. We find that more exotic models cannot resolve these even bigger puzzles, and we see little role for limited participation, idiosyncratic housing risk, transaction costs, or liquidity premiums.”

From a new NBER paper by Òscar Jordà, Moritz Schularick, Alan M. Taylor:

“The risk premium puzzle is worse than you think. Using a new database for the U.S. and 15 other advanced economies from 1870 to the present that includes housing as well as equity returns (to capture the full risky capital portfolio of the representative agent), standard calculations using returns to total wealth and consumption show that: housing returns in the long run are comparable to those of equities,

Posted by at 9:00 AM

Labels: Global Housing Watch

Assessing House Prices with Prudential and Valuation Measures

From a new IMF working paper by Michal Andrle:

“In this paper we provide tools for assessing the house prices and housing valuation. We develop two approaches: (i) borrowing capacity approach, and (ii) intrinsic value approach. The borrowing capacity of households, together with their down payment, implies how much housing they can attain. In the intrinsic value approach, property value is viewed as a discounted present value of adjusted net rental income. Our approach does not involve a complex econometric model and only widely available data are used. The proposed indicators can guide households, financial markets and macroprudential authorities in their understanding of house prices development. To illustrate the concepts, we analyze the housing prices in the Czech Republic and assess the degree of market over-and undervaluation.”

From a new IMF working paper by Michal Andrle:

“In this paper we provide tools for assessing the house prices and housing valuation. We develop two approaches: (i) borrowing capacity approach, and (ii) intrinsic value approach. The borrowing capacity of households, together with their down payment, implies how much housing they can attain. In the intrinsic value approach, property value is viewed as a discounted present value of adjusted net rental income.

Posted by at 8:57 AM

Labels: Global Housing Watch

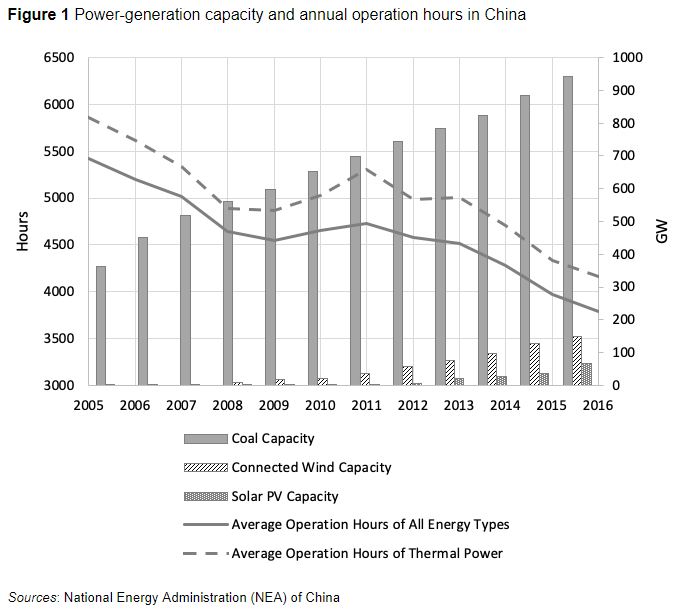

China’s investment in coal power

From VoxEU post by Mengjia Ren, Lee Branstetter, Brian Kovak, Daniel Armanios, Jiahai Yuan:

“Despite leading the world in clean energy investment in recent years, China continues to engage in massive expansion of coal power thanks to policies that effectively subsidise and (over)incentivise coal power investment. This column examines the effects of the 2014 devolution of authority from the central government to local governments on approvals for coal power projects. It finds that the approval rate for coal power projects is about three times higher when the approval authority is decentralised, and provinces with larger coal industries tend to approve more coal power.

After three decades of building up its capital stock, China has entered a phase where efficient allocation of capital resources is vitally important for sustained economic growth. However, due to governance problems and market distortions, many key industries in China have experienced serious capital misallocation and overcapacity issues in the past few years, with the energy industry being one of the most salient examples.

In line with high-profile government pledges to transform China’s energy system, China has led the world in investment in clean energy. In 2015 alone, China built a soccer field of solar panels every hour and one large wind turbine every hour (Carbon Tracker Initiative 2016), easily outpacing green energy investment in any other country. However, at the same time, China was building two coal plants per week. China approved nearly 200 gigawatts of new coal power capacity in 2015, even though the total capacity of the existing coal plants was 884 gigawatts (Ren et al. 2019). Competition from coal power has led to massive curtailment of wind and solar power generation because power grids were obligated to purchase a certain amount of coal power and thus had to reject much of the energy generated by China’s wind and solar power plants.

In the past five years, utilisation levels of all energy types fell sharply as growth in energy supply shot past energy demand (Figure 1 and Table 1). Nearly 50% of China’s coal power plants faced net financial loss in 2018 (Ji 2018). While policy efforts1 have been made to contain the coal overcapacity crisis, under the existing governance structure and market rules, coal power investment in China is unlikely to return in the near future to an equilibrium where plants can still profit under a competitive market price of electricity. It also seems likely that coal power will continue to crowd out solar and wind power for the foreseeable future, raising concerns that China’s vaunted transition to a less carbon-intensive economy will not be managed efficiently.

Continue reading here.

From VoxEU post by Mengjia Ren, Lee Branstetter, Brian Kovak, Daniel Armanios, Jiahai Yuan:

“Despite leading the world in clean energy investment in recent years, China continues to engage in massive expansion of coal power thanks to policies that effectively subsidise and (over)incentivise coal power investment. This column examines the effects of the 2014 devolution of authority from the central government to local governments on approvals for coal power projects.

Posted by at 8:55 AM

Labels: Energy & Climate Change

Subscribe to: Posts