Friday, March 29, 2019

Work of the past, work of the future

From a new VOX post by David Autor:

“Labour markets in US cities today are vastly more educated and skill-intensive than they were 50 years ago, but urban non-college workers now perform much less skilled work than they did. This column shows that automation and international trade have eliminated many of the mid-skilled non-college jobs that were disproportionately based in cities. This has contributed to a secular fall in real non-college wages.”

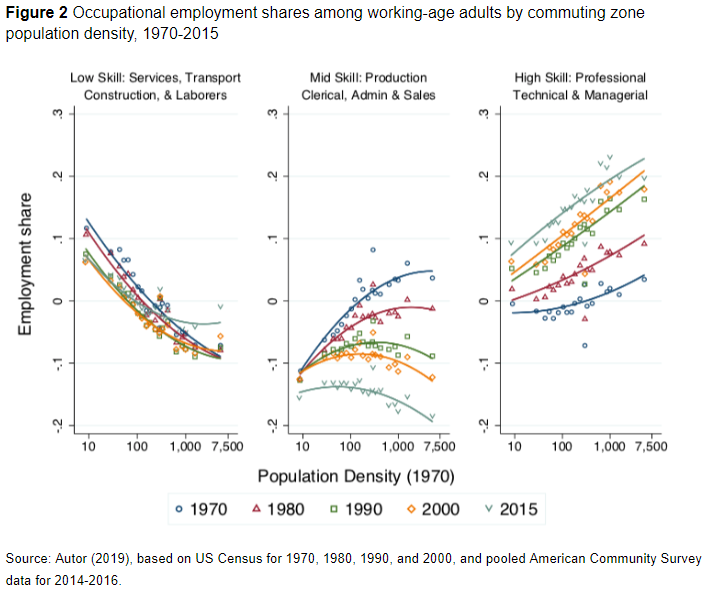

“Figure 2 depicts the aggregate relationship between population density and occupational structure at the level of 722 commuting zones (CZs) covering the contiguous US states between 1970 and 2015.

The three panels of this figure report the CZ-level share of employment among working-age adults into the three broad occupational categories described above: traditionally low-education, low-wage services, transportation, labourer, and construction workers; traditionally mid-education, middle-wage occupations made up of clerical, administrative support, sales, and production workers; and high-education, high-wage, professional, technical, and managerial workers.

The horizontal axis is the natural log of population density (the number of residents divided by CZ land area). For consistency, I used each zone’s population density in 1970 throughout, and the data are weighted by the count of working-age adults in each CZ. Each plotted point in the bin-scatter represents approximately 5% of all workers in each year.

The rising set of upward-sloping curves in the right panel show that while denser CZs have traditionally been more intensive in high-skill work, the level and slope of this relationship between density and skill-intensity has risen consistently over multiple decades. The overlapping downward-sloping curves in the left panel show that the fraction of workers engaged in low-skill occupations has historically been much smaller in high-density CZs, and this pattern has changed little over decades. In the middle panel, the fan-shaped set of curves show that the denser CZs were exceptional in the 1970s for having far more middle-skill work than suburban and rural CZs. But this exceptional feature attenuated. By 2015, the densest CZs had less middle-skill work than the suburbs or rural areas.”

From a new VOX post by David Autor:

“Labour markets in US cities today are vastly more educated and skill-intensive than they were 50 years ago, but urban non-college workers now perform much less skilled work than they did. This column shows that automation and international trade have eliminated many of the mid-skilled non-college jobs that were disproportionately based in cities. This has contributed to a secular fall in real non-college wages.”

Posted by at 10:13 AM

Labels: Inclusive Growth

Housing View – March 29, 2019

On cross-country:

- Scared of Stocks? Buy a House Instead – Bloomberg

- Can Upzoning Increase Housing Supply and Affordability? – Planetizen

- Changing the Housing Story – the Shaping Futures report – SF21

On the US:

- Why Housing Policy Is Climate Policy – New York Times

- Three Scenarios for Growth in Homeowner and Renter Households – Harvard Joint Center for Housing Studies

- How Poor Americans Get Exploited by Their Landlords – Citylab

- A Growing Problem in Real Estate: Too Many Too Big Houses – Wall Street Journal

- Rural America Faces a Housing Cost Crunch – Pew Charitable Trusts

- Zoned Out? The Determinants of Manufactured Housing Rents: Evidence from North Carolina – Journal of Housing Economics

- U.S. housing, consumer confidence data point to slowing economy – Reuters

- A Decade After the Housing Bust, the Exurbs Are Back – Wall Street Journal

On other countries:

- [Australia] Australia central bank research shows income, not just property weakness, key for policy – Reuters

- [Australia] Australia’s Property Stocks Are Ignoring the Housing Slump – Bloomberg

- [Canada] Trudeau housing plan ignores local drivers of affordability – Fraser Institute

- [Canada] The Big Short’s Steve Eisman raises bets against Canadian banks – Financial Times

- [Canada] Housing Is a Magnet for Money Launderers in Toronto: Study – Bloomberg

- [China] That Property Boom Could Be the Reason Employees Are Goofing Off – Bloomberg

- [Denmark] World’s Cheapest Mortgage May Be Around the Corner in Denmark – Bloomberg

- [Finland] Finland’s housing market remains weak – Global Property Guide

- [Italy] Italy House Price Drop Adds Woe for Economy in Recession – Bloomberg

- [Netherlands] Brexit Is Making It Even Harder to Find a Flat in Amsterdam – Bloomberg

- [United Arab Emirates] How Dubai can solve its lack of affordable housing – World Economic Forum

On cross-country:

- Scared of Stocks? Buy a House Instead – Bloomberg

- Can Upzoning Increase Housing Supply and Affordability? – Planetizen

- Changing the Housing Story – the Shaping Futures report – SF21

On the US:

- Why Housing Policy Is Climate Policy – New York Times

- Three Scenarios for Growth in Homeowner and Renter Households – Harvard Joint Center for Housing Studies

- How Poor Americans Get Exploited by Their Landlords – Citylab

- A Growing Problem in Real Estate: Too Many Too Big Houses – Wall Street Journal

- Rural America Faces a Housing Cost Crunch – Pew Charitable Trusts

- Zoned Out?

Posted by at 10:05 AM

Labels: Global Housing Watch

Thursday, March 28, 2019

News-driven inflation expectations and information rigidities

From a new working paper:

“In most democracies the fourth estate, i.e., the news media, plays an important role in society. The media not only has the capacity of advocacy and implicit ability to frame political and economic issues, but it is also the primary source from which most people get information. In macroeconomics, expectations are center stage. But, expectations are shaped by information, and information does not travel unaffected through the ether. Rather, it is digested, filtered, and colored by the media. Surprisingly, however, the potential independent role of the media in the expectation formation process has received relatively little attention in macroeconomics, both in theory and in applied work.

In this paper we build on a growing literature providing evidence for a departure from the full information rational expectation (FIRE) assumption towards a theory of information rigidities (Coibion and Gorodnichenko (2012), Dovern et al. (2015), Coibion and Gorodnichenko (2015a), Armantier et al. (2016)), and investigate the potential role played by the media for households’ inflation expectations in this setting.”

From a new working paper:

“In most democracies the fourth estate, i.e., the news media, plays an important role in society. The media not only has the capacity of advocacy and implicit ability to frame political and economic issues, but it is also the primary source from which most people get information. In macroeconomics, expectations are center stage. But, expectations are shaped by information, and information does not travel unaffected through the ether.

Posted by at 4:38 PM

Labels: Forecasting Forum

Wednesday, March 27, 2019

The Return of the Policy That Shall Not Be Named: Principles of Industrial Policy

From a new IMF working paper by Reda Cherif and Fuad Hasanov:

“Industrial policy is tainted with bad reputation among policymakers and academics and is often viewed as the road to perdition for developing economies. Yet the success of the Asian Miracles with industrial policy stands as an uncomfortable story that many ignore or claim it cannot be replicated. Using a theory and empirical evidence, we argue that one can learn more from miracles than failures. We suggest three key principles behind their success: (i) the support of domestic producers in sophisticated industries, beyond the initial comparative advantage; (ii) export orientation; and (iii) the pursuit of fierce competition with strict accountability.”

From a new IMF working paper by Reda Cherif and Fuad Hasanov:

“Industrial policy is tainted with bad reputation among policymakers and academics and is often viewed as the road to perdition for developing economies. Yet the success of the Asian Miracles with industrial policy stands as an uncomfortable story that many ignore or claim it cannot be replicated. Using a theory and empirical evidence, we argue that one can learn more from miracles than failures.

Posted by at 8:19 AM

Labels: Inclusive Growth

Climate Change and the Federal Reserve

From Glenn D. Rudebusch at the Federal Reserve Bank of San Francisco:

“Climate change describes the current trend toward higher average global temperatures and accompanying environmental shifts such as rising sea levels and more severe storms, floods, droughts, and heat waves. In coming decades, climate change—and efforts to limit that change and adapt to it—will have increasingly important effects on the U.S. economy. These effects and their associated risks are relevant considerations for the Federal Reserve in fulfilling its mandate for macroeconomic and financial stability.

To help foster macroeconomic and financial stability, it is essential for Federal Reserve policymakers to understand how the economy operates and evolves over time. In this century, three key forces are transforming the economy: a demographic shift toward an older population, rapid advances in technology, and climate change. Climate change has direct effects on the economy resulting from various environmental shifts, including hotter temperatures, rising sea levels, and more frequent and extreme storms, floods, and droughts. It also has indirect effects resulting from attempts to adapt to these new conditions and from efforts to limit or mitigate climate change through a transition to a low-carbon economy. This Economic Letter describes how the consequences of climate change are relevant for the Fed’s monetary and financial policy.

Climate change and the transition to a low-carbon economy

Surface temperatures were first regularly recorded around the world in the late 1800s. Since then, the global average temperature has risen almost 2°F (Figure 1) with further increases projected (IPCC 2018). Based on extensive scientific theory and evidence, a consensus view among scientists is that global warming is the result of carbon emissions from burning coal, oil, and other fossil fuels. Indeed, as early as 1896, the Swedish chemist Svante Arrhenius showed that carbon emissions from human activities could cause global warming through a greenhouse effect. The underlying science is straightforward: Certain gases in the atmosphere, such as carbon dioxide and methane, capture the sun’s heat that is reflected off the Earth’s surface, thus blocking that heat from escaping into space. These greenhouse gases act like a blanket around the earth holding in heat. As more fossil fuels are burned, the blanket gets thicker, and global average temperatures increase. Other empirical measurements have confirmed many related adverse environmental changes such as rising sea levels and ocean acidity, shrinking glaciers and ice sheets, disappearing species, and more extreme storms (USGCRP 2018).

Continue reading here.

From Glenn D. Rudebusch at the Federal Reserve Bank of San Francisco:

“Climate change describes the current trend toward higher average global temperatures and accompanying environmental shifts such as rising sea levels and more severe storms, floods, droughts, and heat waves. In coming decades, climate change—and efforts to limit that change and adapt to it—will have increasingly important effects on the U.S. economy. These effects and their associated risks are relevant considerations for the Federal Reserve in fulfilling its mandate for macroeconomic and financial stability.

Posted by at 8:12 AM

Labels: Energy & Climate Change

Subscribe to: Posts