Friday, September 2, 2022

Housing Market in Estonia

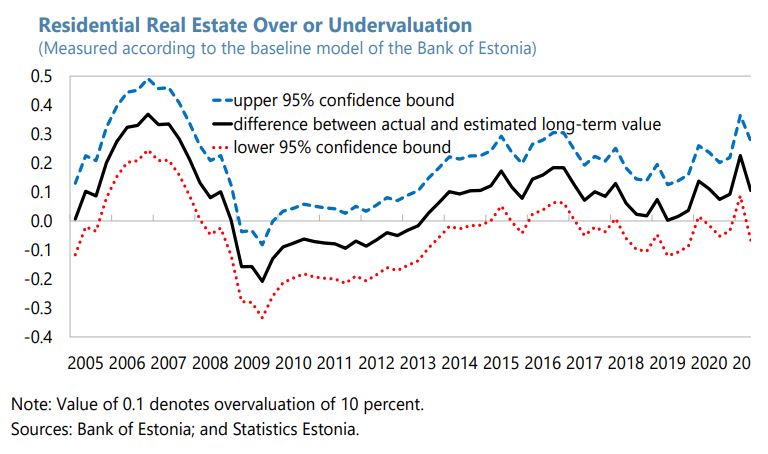

From the IMF’s latest report on Estonia:

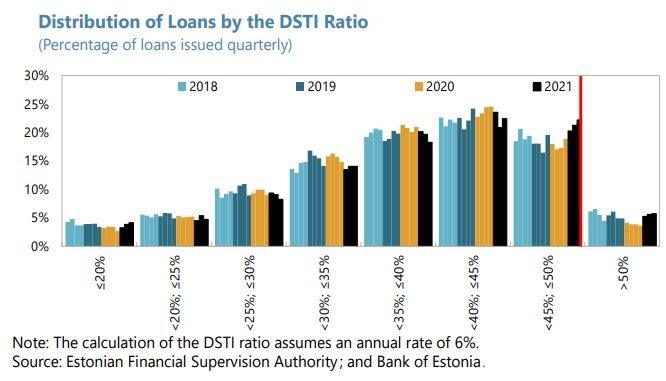

“The authorities estimate that the housing market was moderately overvalued in 2021, while house price growth accelerated further in early 2022, reflecting a combination of strong demand and limited supply. In March 2022, the government tightened the eligibility criteria of the housing loan support program to better target support. The central bank has announced an increase in the countercyclical capital buffer, moving it from zero to 1 percent effective in December 2022.

(…)

The macroprudential stance is appropriate, but careful monitoring of housing market developments is needed. The new countercyclical buffer framework, which will take effect in December 2022, entails a tighter effective stance. This appears appropriate given the continued upward momentum in house prices and credit, which was sustained even during the early phase of the war in Ukraine. The case for further macroprudential action should be continually re-assessed in line with cyclical and housing market conditions, which would depend on the evolution and impact of the war in Ukraine and for now is subject to large uncertainty. The monitoring of the housing market and related lending should pay particular attention to riskier loans such as those with debt-service-to-income ratios close to the regulatory limit. The government’s recent tightening of the eligibility criteria of the housing loan support program in March 2022 is a welcome step.”

From the IMF’s latest report on Estonia:

“The authorities estimate that the housing market was moderately overvalued in 2021, while house price growth accelerated further in early 2022, reflecting a combination of strong demand and limited supply. In March 2022, the government tightened the eligibility criteria of the housing loan support program to better target support. The central bank has announced an increase in the countercyclical capital buffer, moving it from zero to 1 percent effective in December 2022.

Posted by at 12:00 PM

Labels: Global Housing Watch

Housing View – September 2, 2022

On cross-country:

- As the U.S. Dollar Surges, American Buyers Splurge on European Homes. Favorable exchange rates and steady property prices have led to big interest in markets like London, Paris and Tuscany – Wall Street Journal

On the US—developments on house prices and rent:

- Case-Shiller National House Price Index “Decelerated” to 18.0% year-over-year increase in June. FHFA: “[A] deceleration has appeared in the June monthly data” – Calculated Risk

- The Huge Upward Momentum in House Prices is Gone – Check Your City – Real Estate Decoded

- Home Price Growth Eased in June – NAHB

- Inflation Adjusted House Prices Declined in June. House Price-to-Rent Ratio also Declined in June – Calculated Risk

- U.S. house price inflation to plunge in 2023, fair value still a distant dream – Reuters

- A ‘buyers’ market’ for homes is still elusive in the US. Home prices are falling with tighter monetary policy, but higher interest rates don’t fix shortages – FT

- American cities want rent control to rein in housing costs. Economists still think they are a bad idea – The Economist

- Pace of Rent Increases Continues to Slow. Higher Rents will continue to impact measures of inflation in 2022 – Calculated Risk

- July Rental Report: Nationwide Rent Holds Steady Despite Big-City Resurgence – Realtor

- Record-Breaking Rent Growth in Markets in the South and West – Harvard Joint Center for Housing Studies

- Stucco and Vinyl were the Most Common Siding Materials on New Homes in 2021 – NAHB

On the US—other developments:

- The Housing Market Is in Recession. What It Means For Home Buyers. – Barron’s

- Shorting Zillow Is Your Best Bet in Housing This Year. Think the real-estate market is in for a price cut? The biggest one could still come to Zillow’s stock – Wall Street Journal

- Andra Ghent: Salt Lake City should sell golf courses to provide affordable housing. It is a lot cheaper to prevent people from becoming homeless than to help them afterward. – Salt Lake Tribune

- American Real Estate Was a Money Launderer’s Dream. That’s Changing. – New York Times

- California rolls out a daring new housing policy to combat high home prices and increase supply – Fortune

- Big US mortgage lenders turn screws on smaller rivals as rates rise. United Wholesale and Rocket pursue aggressive strategies as others pull back or go out of business – FT

- Consumer Bankruptcy, Mortgage Default and Labor Supply – Philadelphia Fed

- 2022 Housing Markets Remain in Sellers Favor, but Conditions Are Changing. Home Sellers Are Contending with Slowing Real Estate Fundamentals – Realtor

- Everyone’s a Landlord—Small-Time Investors Snap Up Out-of-State Properties. With the help of recent technologies, laptop landlords are buying homes across the U.S. – Wall Street Journal

- Affordable Housing Developers Look to the White House for Help. Construction costs and labor shortages have made it harder to build affordable housing. Now the Biden administration is urging cities to use American Rescue Plan funds to boost supply. – Bloomberg

- Goldman Says US Housing Downturn Has Further to Go as Rates Rise – Bloomberg

- Why Obama-Era Economists Are So Mad About Student Debt Relief. It exposes their failed mortgage debt relief policies after the Great Recession. – The American Prospect

- Yes, your house is wealth. In order to fix our dysfunctional housing politics, we must confront this economic fact. – Noah Smith

- New Estimates of the US Homeless Population – NBER

- Active vs Total Existing Home Inventory – Calculated Risk

- Private Residential Spending Slides in July – NAHB

On China:

- China’s Property Market Has Slid Into Severe Depression, Real-Estate Giant Says. Country Garden, which for years ranked as China’s top real-estate developer, reports 96% drop in first-half profit – Wall Street Journal

- China’s largest banks show wounds from property sector crisis – Reuters

- China’s AgBank Says Overdue Loans From Mortgage Boycott Double. Lender posts 5.8% profit gain in first half on lending boost. Sector faces tumult from slowing economy, property crisis – Bloomberg

- Pinched by Housing Downturn, Chinese Families Rein In Spending. More homeowners in China are reckoning with shrinking wealth amid a nearly year-long home-price decline, adding another drag on consumption – Wall Street Journal

- China’s property-driven growth model is broken. Beijing should prepare for a long and difficult economic transformation – FT

- Hong Kong tycoon calls bottom of China’s property slump. Adrian Cheng says his New World Development group will spend $1.5bn to buy land in the next year – FT

- Point of no return: crunch time as China tries to fend off property crash. With the global economy also at a crossroads, Beijing’s leadership faces a perilous test of nerve on its lending crackdown and zero-Covid strategy – The Guardian

- Chinese borrowers pile pressure on banks with early mortgage payments. Affluent property owners cut leverage as liquidity crisis hammers property sector and economy sputters – FT

- As China’s property crisis grows, is the global economy at risk? China’s house prices are falling as Beijing reins in sector, raising fears for economic growth at home and globally. – Al Jazeera

On other countries:

- [Australia] Australia’s house prices take biggest dive in 40 years. Property prices drop 1.6 percent in August in sharpest fall since 1983. – Al Jazeera and The Guardian

- [Australia] Australia’s property downturn puts home buyers in double mortgage bind – The Guardian

- [Canada] Canadian Housing Outlook: Testing the Foundation – TD

- [Israel] Bank of Israel’s Yaron on Policy, Inflation, Housing – Bloomberg

- [Netherlands] The Netherlands’ housing market remains fundamentally strong – Global Property Guide

- [United Kingdom] Alarm Bells Ring for UK Housing as Signs Point to Falling Prices. Inflation surge and higher interest rates are taking a toll. Industry survey shows buyer interest and price optimism waning – Bloomberg

- [United Kingdom] Equity release loans surge as older homeowners raise funds. Borrowers appear undeterred by rising interest rates – FT

- [United Kingdom] UK house price surge to end as cost of living crisis bites: Reuters poll – Reuters

- [United Kingdom] UK House Prices Rise More Than Forecast But Slowdown Anticipated – Bloomberg

On cross-country:

- As the U.S. Dollar Surges, American Buyers Splurge on European Homes. Favorable exchange rates and steady property prices have led to big interest in markets like London, Paris and Tuscany – Wall Street Journal

On the US—developments on house prices and rent:

- Case-Shiller National House Price Index “Decelerated” to 18.0% year-over-year increase in June. FHFA: “[A] deceleration has appeared in the June monthly data” – Calculated Risk

- The Huge Upward Momentum in House Prices is Gone –

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, September 1, 2022

Yes, your house is wealth

From Noah Smith:

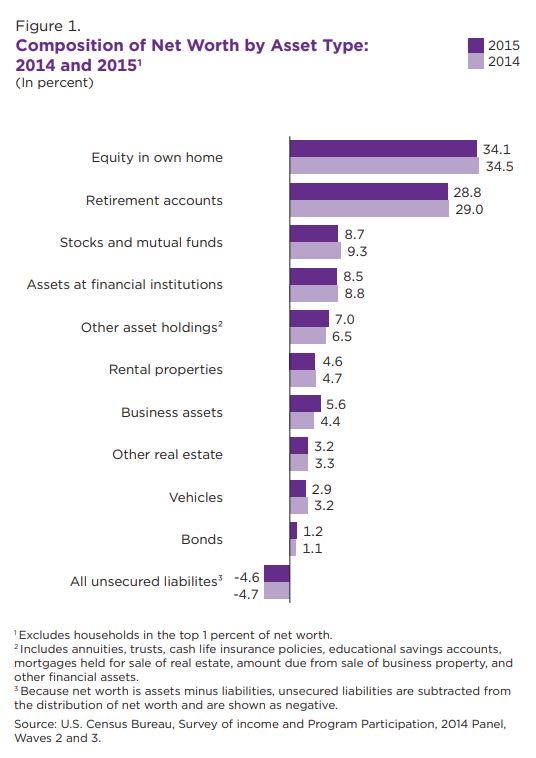

“Every so often I encounter the argument that owner-occupied housing isn’t a form of wealth. This would come as news to economists like Emmanuel Saez and Gabriel Zucman, who study wealth inequality for a living, and who definitely count owner-occupied home equity in their wealth numbers. It would also come as news to the U.S. Census Bureau, who finds that equity in owner-occupied housing represented the largest share of the wealth of households outside the top 1% as recently as 2015:

The definition of wealth here is just assets minus liabilities. An asset is anything you can sell for money. You can sell your house for money. Hence it is an asset. In fact, historically, it’s one of the assets with the best returns.

But I don’t want to make an argument from authority here. There are very good reasons we count owner-occupied housing as wealth, and they’re not too hard to understand.

To see why, first let’s make an analogy: a magic cupboard that gives you food.

The magic cupboard analogy

Suppose you had a magic cupboard that gave you three meals a day, free of charge. Furthermore, suppose there was a market for magic cupboards, and that you could sell your own for $1 million if you wanted to.

This magic cupboard represents a form of wealth. If you think it’s not, consider whether you would be poorer if your magic cupboard burned down or got stolen or stopped working. Yes, you would be poorer.

Some people might argue: “But you need food every day. If you sold your magic cupboard, you’d just have to use the money to buy food.” And indeed you would. You would have to go to the grocery store or go to restaurants, because you wouldn’t have a magic cupboard. You could use the cash from the sale of your magic cupboard to buy food at the store or at restaurants.

But now consider someone who doesn’t own a magic cupboard. They also have to eat every day. They have to go to the grocery store or go to restaurants. But unlike you if you sold your magic cupboard for cash, the person who didn’t start out with a magic cupboard has to work for the cash they need to buy food every day. Because they have to work for what you could just buy off of an asset sale, they’re poorer than you.

Thus, the magic cupboard is wealth.”

Continue reading here.

From Noah Smith:

“Every so often I encounter the argument that owner-occupied housing isn’t a form of wealth. This would come as news to economists like Emmanuel Saez and Gabriel Zucman, who study wealth inequality for a living, and who definitely count owner-occupied home equity in their wealth numbers. It would also come as news to the U.S. Census Bureau, who finds that equity in owner-occupied housing represented the largest share of the wealth of households outside the top 1% as recently as 2015:

The definition of wealth here is just assets minus liabilities.

Posted by at 8:46 AM

Labels: Global Housing Watch

Friday, August 26, 2022

Housing View – August 26, 2022

On cross-country:

- BIS residential property price statistics, Q1 2022 – BIS

On the US:

- Eviction and Poverty in American Cities – NBER

- The Fed Sees Housing Trouble Ahead. There have been conflicting signals in the housing market. And several factors may stop any slowdown from turning into a slump. – New York Times

- American dream of owning a home out of reach for many in tight markets. Many middle- and lower-income Americans are left with a dwindling number of options or forced into renting while supply increases for the wealthiest buyers – The Guardian

- It Was the Housing Crisis Epicenter. Now the Sun Belt Is an Inflation Vanguard. Inflation has been worse in Southern cities, burdening residents and prompting the question: What can it teach the rest of the country? – New York Times

- Early effects of COVID-19 pandemic-related state policies on housing market activity in the United States – Journal of Housing Economics

- New Home Sales Plummet in July – NAHB

- Rent Price Increased for Fifth Consecutive Quarter – NAHB

- The Rental Housing Crisis Is a Supply Problem That Needs Supply Solutions. Policymakers must prioritize improving housing access and affordability for low-income households through immediate and long-term investments. – Center for American Progress

- New Apartments at 50-Year High May Ease Pressure on US Rents. About 420,000 rental units expected this year: RentCafe study. Extra supply could help alleviate record rents in some cities – Bloomberg

- Home Sellers Are Slashing Prices in Pandemic Boomtowns. Redfin found that 70% of homes for sale in Boise, Idaho, had their price cut in July, the highest share of 97 metros. – Bloomberg

- U.S. new home sales tumble to 6-1/2-year low; prices still high – Reuters

- Housing supply and demand are beginning to balance – Washington Post

- Where will housing prices end 2022? New data predicts a 4% drop in 5 months—and homes with these two characteristics will be hardest hit – Fortune

- Home Prices Just Dipped—Does That Mean They’re Poised To Plummet This Fall? – Realtor

- White House Pledges ‘Stability’ Vouchers for Homeless and At-Risk People. New housing vouchers build on efforts by the Biden administration to focus on unsheltered and rural homelessness and drive aid to people suffering domestic violence. – Bloomberg

On China:

- China slashes 5-year mortgage rate as property crisis deepens. Central bank equals record rate cut in May but move unlikely to resolve crisis for developers, strategists say – FT

- China’s property market is in freefall. What does this mean for the world economy? The sector is dangerously overheated – but unlike the 2008 financial crisis, the global ripple effect is likely to be limited – The Guardian

- China Probes Property Executives for Possible Law Violations. Signals potential expansion of Xi’s crackdown on corruption. Campaign has focused on financial and technology sectors – Bloomberg

On other countries:

- [Australia] Australia’s Slumping Property Market Raises Risk of a Recession. Households’ record debt-to-income ratio squeezed by rate hikes. Major risk is fallout on consumption that makes up 60% of GDP – Bloomberg

- [Sweden] Swedish Construction Activity Slows Amid Slump in Housing Market – Bloomberg

- [United Arab Emirates] Dubai looks to restart mothballed luxury developments for wave of wealthy incomers. Volume of residential transactions is at its highest since peak of 2009, says real estate group CBRE – FT

- [United Kingdom] Where do landlords think the UK property market is going? – FT

On cross-country:

- BIS residential property price statistics, Q1 2022 – BIS

On the US:

- Eviction and Poverty in American Cities – NBER

- The Fed Sees Housing Trouble Ahead. There have been conflicting signals in the housing market. And several factors may stop any slowdown from turning into a slump. – New York Times

- American dream of owning a home out of reach for many in tight markets.

Posted by at 7:01 AM

Labels: Global Housing Watch

Tuesday, August 23, 2022

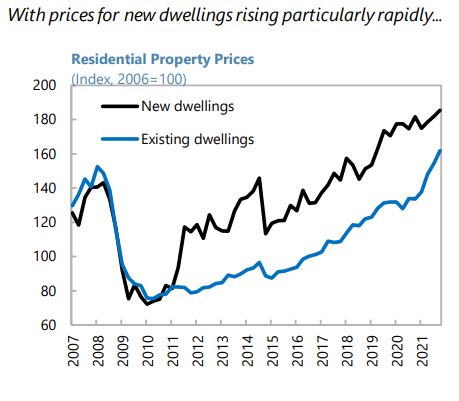

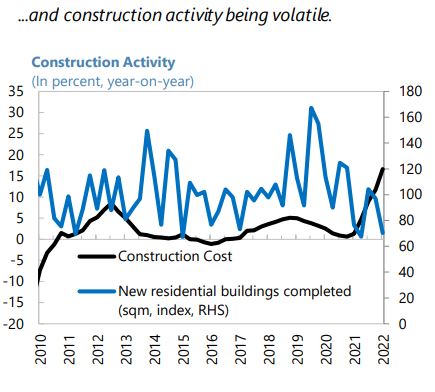

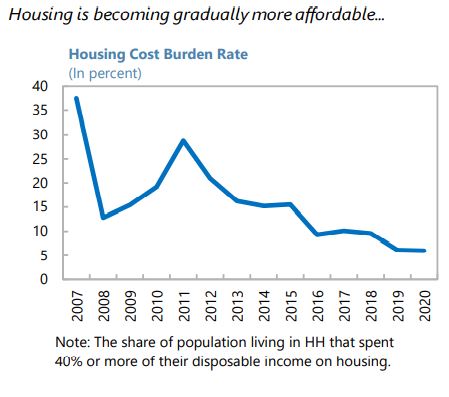

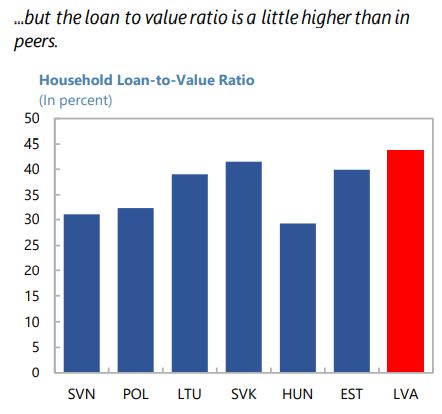

Housing Market in Latvia

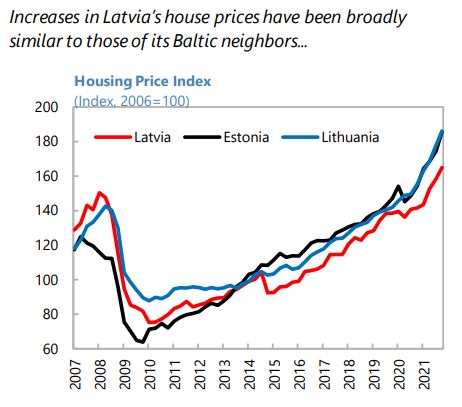

From the IMF’s latest report on Latvia:

“Macroprudential policy should remain flexible considering high uncertainty. After augmenting their macro-prudential toolkit in mid-2020 with several borrower-based measures, the authorities broadened the scope of these tools to cover credit institutions of other EU countries operating in Latvia with or without local branches. Although real estate prices increased, they appeared to be in line with wage growth and remained less buoyant than in the other Baltic countries. However, housing prices could surge, if the already-low supply of housing is further constrained by the rising costs of capital, labor and materials, and delays in the construction sector due the spillovers of the war. A close monitoring of these developments is warranted, so that macroprudential policy can be re-calibrated accordingly in a timely manner. Credit risks could emerge due to the elevated share of high variable-interest loans to both households and non-financial corporations (87 and 94 percent of outstanding loans respectively).

(…)

Macroprudential policy should stand ready to respond to changing housing market conditions. Given the new risks caused by the war, the frequent reviews of macroprudential measures should continue to ensure the right balance between financial stability and the need for credit in the economy.”

From the IMF’s latest report on Latvia:

“Macroprudential policy should remain flexible considering high uncertainty. After augmenting their macro-prudential toolkit in mid-2020 with several borrower-based measures, the authorities broadened the scope of these tools to cover credit institutions of other EU countries operating in Latvia with or without local branches. Although real estate prices increased, they appeared to be in line with wage growth and remained less buoyant than in the other Baltic countries.

Posted by at 5:57 PM

Labels: Global Housing Watch

Subscribe to: Posts