Wednesday, January 19, 2022

[New Paper] Parameter-efficient deep probabilistic forecasting

New paper by Olivier Sprangers, Sebastian Schelter & Maartende Rijke

Abstract:

Probabilistic time series forecasting is crucial in many application domains, such as retail, ecommerce, finance, and biology. With the increasing availability of large volumes of data, a number of neural architectures have been proposed for this problem. In particular, Transformer-based methods achieve state-of-the-art performance on real-world benchmarks. However, these methods require a large number of parameters to be learned, which imposes high memory requirements on the computational resources for training such models. To address this problem, we introduce a novel bidirectional temporal convolutional network that requires an order of magnitude fewer parameters than a common Transformer-based approach. Our model combines two temporal convolutional networks: the first network encodes future covariates of the time series, whereas the second network encodes past observations and covariates. We jointly estimate the parameters of an output distribution via these two networks. Experiments on four real-world datasets show that our method performs on par with four state-of-the-art probabilistic forecasting methods, including a Transformer-based approach and WaveNet, on two point metrics (sMAPE and NRMSE) as well as on a set of range metrics (quantile loss percentiles) in the majority of cases. We also demonstrate that our method requires significantly fewer parameters than Transformer-based methods, which means that the model can be trained faster with significantly lower memory requirements, which as a consequence reduces the infrastructure cost for deploying these models.

Read more here.

New paper by Olivier Sprangers, Sebastian Schelter & Maartende Rijke

Abstract:

Probabilistic time series forecasting is crucial in many application domains, such as retail, ecommerce, finance, and biology. With the increasing availability of large volumes of data, a number of neural architectures have been proposed for this problem. In particular, Transformer-based methods achieve state-of-the-art performance on real-world benchmarks. However, these methods require a large number of parameters to be learned, which imposes high memory requirements on the computational resources for training such models.

Posted by at 5:37 PM

Labels: Forecasting Forum

New Evidence on the Measurement and Determinants of Poverty in the United States

From a new IMF Working Paper (2022) by Katharina Bergant, Miss Anke Weber, and Andrea Medici.

Summary:

“Using micro-data from household expenditure surveys, we document the evolution of consumption poverty in the United States over the last four decades. Employing a price index that appears appropriate for low-income households, we show that poverty has not declined materially since the 1980s and even increased for the young. We then analyze which social and economic factors help explain the extent of poverty in the U.S. using probit, tobit, and machine learning techniques. Our results are threefold. First, we identify the poor as more likely to be minorities, without a college education, never married, and living in the Midwest. Second, the importance of some factors, such as race and ethnicity, for determining poverty has declined over the last decades but they remain significant. Third, we find that social and economic factors can only partially capture the likelihood of being poor, pointing to the possibility that random factors (“bad luck”) could play a significant role.”

From a new IMF Working Paper (2022) by Katharina Bergant, Miss Anke Weber, and Andrea Medici.

Summary:

“Using micro-data from household expenditure surveys, we document the evolution of consumption poverty in the United States over the last four decades. Employing a price index that appears appropriate for low-income households, we show that poverty has not declined materially since the 1980s and even increased for the young. We then analyze which social and economic factors help explain the extent of poverty in the U.S.

Posted by at 7:39 AM

Labels: Inclusive Growth

Tuesday, January 18, 2022

Fraud and the financial crisis

From a paper by John M. Griffin:

“From the very start of the 2008 housing and financial crisis, close observers suspected widespread fraud lay behind the rapid meltdown in the US mortgage market. But even a decade after the fact, there was little consensus among economists as to whether that was the root cause.

In a paper in the Journal of Economic Literature, author John M. Griffin synthesizes the broad array of literature on the role of residential mortgage-backed securities (RMBS) securitization and finds that conflicts of interest among banks, ratings agencies, and other key players were a key driving force behind the financial crisis.

Griffin says that the process of creating and selling complex financial assets based on home loans was closely linked to the housing bubble—and shot through with malfeasance.

In the run-up to the crisis, underwriters facilitated wide-scale fraud by knowingly misreporting key loan characteristics, credit rating agencies catered to investment banks by inflating their ratings on both mortgage-backed securities and collateralized debt obligations, originators engaged in mortgage fraud to increase market share, and real estate appraisers inflated their appraisals in order to gain business.

As credit was extended to those who could not afford loans, house prices boomed and subsequently crashed when homeowners started defaulting. However, this supply of fraudulent credit was not uniform across US zip codes.

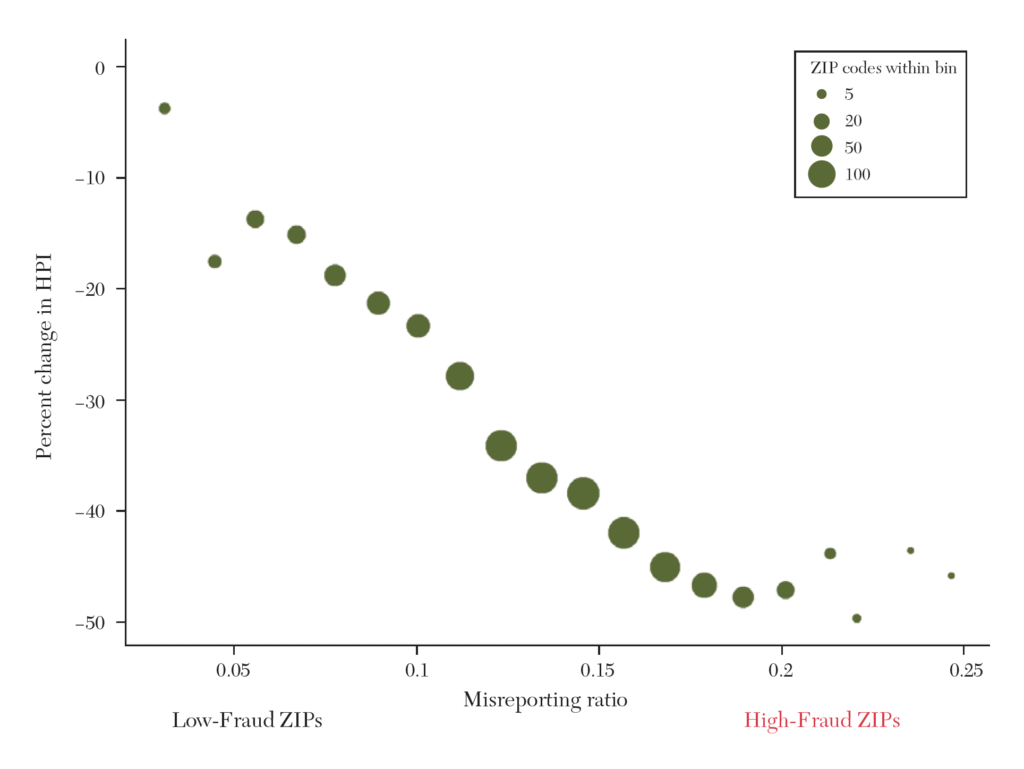

Griffin illustrated variation in mortgage fraud using zip code data from California, which had the greatest number of mortgage originations during the period. Figure 1 from his paper shows that the state’s housing prices decreased as loans from dubious originators increased.

The y-axis is the percent change in the Federal Housing Finance Agency house price index (HPI) per zip code from 2007 to 2010, and the x-axis is the fraction of misreported loans per zip code from 2003 to 2007. The size of each point represents the number of zip codes.

The chart shows a strong negative relationship between misreporting and the home price bust. California zip codes with more than 15 percent fraudulent origination experienced home price decreases of 44.6 percent on average, whereas zip codes with less than 3 percent fraudulent originators only experienced 5.4 percent price decreases.

While other factors such as excess credit and speculation could be drivers, Griffin says that numerous studies since the crisis point toward fraud as a central explanation.”

From a paper by John M. Griffin:

“From the very start of the 2008 housing and financial crisis, close observers suspected widespread fraud lay behind the rapid meltdown in the US mortgage market. But even a decade after the fact, there was little consensus among economists as to whether that was the root cause.

Posted by at 6:48 PM

Labels: Global Housing Watch

[New Paper] On the Macroeconomic Consequences of Over-Optimism

By Paul Beaudry & Tim Willems in AEJ: Macroeconomics

Abstract – Analyzing International Monetary Fund (IMF) data, we find that overly optimistic growth expectations for a country induce economic contractions a few years later. To isolate the causal effect, we take an instrumental variable approach—exploiting randomness in the country allocation of IMF mission chiefs. We first document that IMF mission chiefs differ in their individual degrees of forecast optimism, yielding quasi-experimental variation in the degree of forecast optimism at the country level. The mechanism appears to run through excessive accumulation of debt (public and private). Our findings illustrate the potency of unjustified optimism and underline the importance of basing economic forecasts upon realistic medium-term prospects.

Read more here.

By Paul Beaudry & Tim Willems in AEJ: Macroeconomics

Abstract – Analyzing International Monetary Fund (IMF) data, we find that overly optimistic growth expectations for a country induce economic contractions a few years later. To isolate the causal effect, we take an instrumental variable approach—exploiting randomness in the country allocation of IMF mission chiefs. We first document that IMF mission chiefs differ in their individual degrees of forecast optimism, yielding quasi-experimental variation in the degree of forecast optimism at the country level.

Posted by at 1:07 PM

Labels: Forecasting Forum

UN Report- World Economic Situation and Prospects 2022

Source: United Nations Department of Economic and Social Affairs

“Global economic recovery hinges on a delicate balance amid new waves of COVID-19 infections, persistent labour market challenges, lingering supply-chain constraints and rising inflationary pressures”, reads the recently released report by the UN. The world economy is projected to grow by 4 percent in 2022 and 3.5 percent in 2023. Some excerpts from the report are as presented underneath:

The good: Half of the world’s economies will exceed pre-pandemic levels of output by at least 7 percent in 2023. In East Asia and South Asia, the average gross domestic product (GDP) in 2023 is projected to be 18.4 percent above its 2019 level, compared to only 3.4 percent in Latin America and the Caribbean. Besides, global investment expanded by an estimated 7.5 percent in 2021 (after contracting by 2.7 percent in 2020) driven by growth in China and the United States. As regards poverty, the number of people living in extreme poverty globally is projected to decrease slightly to 876 million in 2022 but is expected to remain well above pre-pandemic levels. Fast-developing economies in East Asia and South Asia and developed economies are expected to experience some poverty reduction.

The not so good: Despite a robust recovery, East Asia and South Asia’s GDP in 2023 is projected to remain 1.7 percent below the levels forecast prior to the pandemic, while these figures stand at 5.5 and 4.2 percent for Africa, and Latin America and the Caribbean, respectively. Labour markets have contracted severely, and full recovery in developed economies is only projected to happen by 2023 or 2024.

The risks: Limited access to vaccines poses a particular challenge to most developing countries and transition economies. Rising inflationary pressures in major developed economies and a number of large developing countries present additional risks to recovery. Global headline inflation rose to an estimated 5.2 percent in 2021, more than 2 percentage points above its trend rate in the past 10 years. The inflationary pressure was particularly pronounced in the United States, the euro area and Latin America and the Caribbean. Higher levels of inequality within and between countries, and against vulnerable populations like women, is one of the greatest risks to the social fabric as suggested by the report.

Read the full report for in-depth forecasts on issues like the state of multilateralism, asset price bubbles, monetary policy, healthcare crises, and climate change.

Also Read:

Source: United Nations Department of Economic and Social Affairs

“Global economic recovery hinges on a delicate balance amid new waves of COVID-19 infections, persistent labour market challenges, lingering supply-chain constraints and rising inflationary pressures”, reads the recently released report by the UN. The world economy is projected to grow by 4 percent in 2022 and 3.5 percent in 2023. Some excerpts from the report are as presented underneath:

The good: Half of the world’s economies will exceed pre-pandemic levels of output by at least 7 percent in 2023.

Posted by at 12:30 PM

Labels: Inclusive Growth

Subscribe to: Posts