Wednesday, March 9, 2022

How Can African Countries Avoid the Middle-Income Trap?

From Tony Blair Institute for Global Change:

“Since the early 2010s, economists and policymakers have noted that several countries are stuck in what has come to be known as the “middle-income trap”. Three main explanations are posited:

- Lack of structural transformation and weak industrial policies: the level of development of productive capacities, which includes the level of export sophistication, the change in their composition through comparative advantage and the state’s role in industrial upgrading.

- Lack of human-capital development and innovation: the unsuccessful transition to innovation-based growth (from factor-based growth), notably due to lack of investment in research and development (R&D) and education.

- Poor governance, weak institutions and an extractive political economy: the low quality of institutions and government effectiveness, and the role of political economy and political stability in explaining countries’ development paths.

While few countries have succeeded in their transition to the high-income level – based on gross national income (GNI) – including the East Asian “tiger economies” of South Korea, Taiwan, Hong Kong and Singapore, the development trajectory of several countries currently in the middle-income trap validates the explanations cited in the academic literature on the subject. In this paper, we highlight the development paths of successful countries like South Korea, and of middle-income countries that are in the trap or at risk of being trapped, such as Malaysia, Brazil, Tunisia, Morocco, Vietnam and Bangladesh.

There are three factors that have contributed to South Korea’s success: a well-planned and consistent government policy combined with effective implementation, conditional support to companies that ensured the reduction of the rent-seeking approach, and an effective channelling of public resources, together with an early transition towards innovation, including a focus on short-cycle technology-based sectors.

The experiences of Malaysia, Brazil, Tunisia, Morocco, Bangladesh and Vietnam highlight that economic growth is not enough to enable countries to move up the income ladder. It is essential to have a commitment to industrialisation, to strengthening the rule of law and to moving away from an extractive political economy, and this must be set against the backdrop of political stability and equality. In addition, the level of investment in both human-capital development and innovation is a significant variable in determining countries’ development paths and in explaining their middle-income trap.

Latin America – with the notable exception of Chile – has failed to make the transition from middle-income to high-income status. In this paper we take the example of Brazil which, in common with much of the region, had – in the 1960s – been predicted to achieve a level of growth that would ultimately have led to it reaching the high-income level. However, poor levels of investment, low take-up of tertiary education, political instability and high inflation have all conspired to leave Brazil mired in the middle-income trap for more than half a century.

Ghana and Kenya, both of which have the potential to become the dominant hubs in west and east Africa respectively, have witnessed relatively high economic growth over the past decade and have transitioned quite recently to the lower-middle-income status. Both countries have the capacity to become pre-eminent centres of innovation and to help drive growth and trade in neighbouring countries. However, their current growth is not geared towards economic transformation, and there are signs that both countries are at a high risk of remaining trapped at the middle-income level. Productivity in agriculture remains low and exports of goods are concentrated on natural resources (oil and gold in Ghana and unprocessed agricultural products in Kenya) with only a small number of technology-intensive products. Moreover, the level of human-capital development remains relatively low compared with other lower-middle-income countries such as Tunisia and Morocco. Services play an important role in both economies but most jobs are in low-productive service sectors such as wholesale and retail. The digital economy and other highly productive sectors such as financial services have significant potential for growth in both countries, given the emerging technology hubs in Accra and Nairobi, but they currently represent a small share of service exports and don’t create enough jobs fast enough.

It is essential for both countries to invest in industrialisation by focusing on agri-processing, manufacturing and high-value-added tradable services enabled by information and communications technology (ICT) and other innovations, following a consistent, pragmatic and visionary approach. For industrialisation to be successful, it is important for political leaders to consider it as a political project to transform the economy by building productive industries, rather than seeing it as a technocratic reform. This political project requires strong political coalitions, institutional capacity and alignment within government for effective implementation, areas where both Ghana and Kenya can significantly improve. In parallel, there is a need to improve critical enablers for industrialisation, including agriculture transformation, human-capital development, energy access and reliability, while ensuring macroeconomic stability and a business environment conducive to entrepreneurial activity.”

From Tony Blair Institute for Global Change:

“Since the early 2010s, economists and policymakers have noted that several countries are stuck in what has come to be known as the “middle-income trap”. Three main explanations are posited:

- Lack of structural transformation and weak industrial policies: the level of development of productive capacities, which includes the level of export sophistication, the change in their composition through comparative advantage and the state’s role in industrial upgrading.

Posted by at 9:08 AM

Labels: Macro Demystified

Tuesday, March 8, 2022

Housing Market in Hong Kong

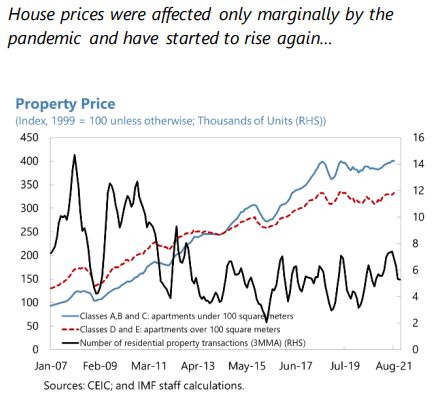

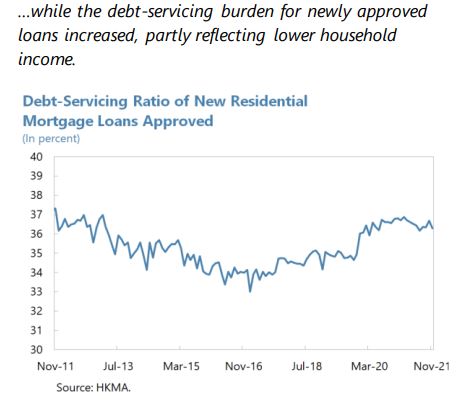

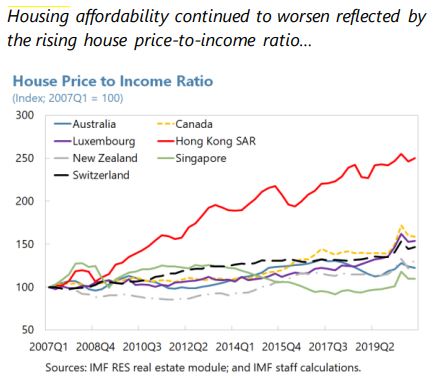

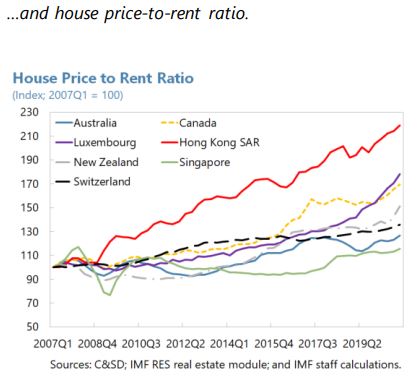

From the IMF’s latest report on Hong Kong:

“Residential house prices are on the rise again, contributing to a further increase in the already elevated level of household debt. The average debt-servicing ratio for new mortgages increased to 36.9 percent at its peak in February 2021 from 36.0 percent in December 2019, partly driven by the decline in household income. While household assets are large in aggregate—as reflected by the high household net worth-to-liabilities ratio of 11.2 times and safe assets-to-liabilities ratio of 2.9 times in 2019—the wealth distribution is skewed towards high-income households.

Given the stretched valuation, a disorderly adjustment in the property market could pose a risk to the economy. A sharp house price correction could trigger an adverse feedback loop between house prices, debt service capacity, household consumption, and growth, negatively affecting banks’ balance sheets. In addition, the FSAP analysis indicated that low-income households could be under significant financial stress when facing rising interest rates and falling income. To mitigate such risks, the authorities should continue to carefully monitor the household debt repayment capacity, particularly for low-income households.

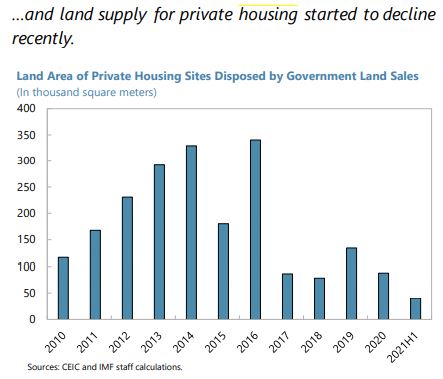

The three-pronged approach to increasing housing affordability and containing housing market risks remains valid, but more efforts are needed to raise housing supply.

*Increasing housing supply is critical to resolve the structural supply-demand imbalance. Housing supply has increased on average since 2015 with the implementation of the government’s Long-term Housing Strategy and the Hong Kong 2030+ Strategy, but has fallen short of target by about 30 percent on average. Staff welcomes the identification of the land to provide 330,000 public housing units within the next ten years and urges the authorities to bring the actual public housing production back to the target without further delays. To this end, a comprehensive approach is urgently needed, including increasing land supply for housing production (e.g., land resumption, reclamation, and re-zoning) while expediting and streamlining the process for land identification and production (e.g., environmental, transport, and other relevant assessments). The recently announced Northern Metropolis development strategy could boost housing supply over the longer-term period.

**The macroprudential stance for property markets should be maintained to safeguard financial stability. A series of macroprudential policies that have been introduced and tightened since 2009—such as ceilings on loan-to-value (LTV) ratio, caps on debt service-to-income ratio (DSR), and stress testing of the DSR against interest rate increases—have helped contain vulnerabilities in the banking system (…). Given resilient house prices and mortgage growth, the existing residential property-related macroprudential policies should be kept unchanged for now and any changes should be data-dependent with due attention to the emerging risk of regulatory leakages. Moreover, the Council of Financial Regulators (CFR) should take the lead in strengthening the regular surveillance and data collection on lending by non-bank lenders (e.g., property developers and non-bank financial institutions), and the authorities should regularly reassess the need to expand the regulatory perimeter to mitigate the leakages in macroprudential policies.

***Stamp duties have been effective in containing speculative activity and external demand. The government has introduced three types of stamp duties to curb excess demand by both residents and nonresidents. Although they have helped curb house price increases and contain household leverage and systemic risks, the New Residential Stamp Duty (NRSD) introduced since November 2016 (…) is a residency-based capital flow management measure and a macroprudential measure (CFM/MPM) levied at a higher rate on non-residents than on first-time resident home buyers. Therefore, staff recommends phasing it out once systemic risks from the non-resident inflow dissipate.

Authorities’ Views

The authorities agreed that increasing land supply remains the key to fundamentally resolving the structural imbalance between housing demand and supply. They emphasized that various measures had been taken to boost land supply for housing production, including by accelerating land resumption and expediting and streamlining the process of land production, and such efforts were starting to bear fruits. The authorities viewed the current tight macroprudential stance for housing market as appropriate given the elevated house prices, while noting that they will continue to closely monitor the housing market and stand ready to make necessary adjustments with a view to safeguarding financial stability. They noted that mortgage lending by non-banks has been closely monitored and has declined in recent years amid the authorities’ efforts to regulate banks’ lending to non-banks and the expansion in the mortgage insurance program.”

From the IMF’s latest report on Hong Kong:

“Residential house prices are on the rise again, contributing to a further increase in the already elevated level of household debt. The average debt-servicing ratio for new mortgages increased to 36.9 percent at its peak in February 2021 from 36.0 percent in December 2019, partly driven by the decline in household income. While household assets are large in aggregate—as reflected by the high household net worth-to-liabilities ratio of 11.2 times and safe assets-to-liabilities ratio of 2.9 times in 2019—the wealth distribution is skewed towards high-income households.

Posted by at 6:53 AM

Labels: Global Housing Watch

Monday, March 7, 2022

Learning from the East Asian Urbanization Model

Source: Centre for Global Development

For the many urbanized and rapidly urbanizing countries, the East Asian experience with and response to emerging challenges is a model to look up to. As high-income East Asian economies approach peaking urbanization, they are now plagued with several challenges. From service sector and export-led growth outstripping manufacturing to rising carbon levels in cities, aging populations, and infrastructure that struggles to catch up with advances in technology- the concerns are aplenty.

In this working paper for the think tank, CGDEV, author Shahid Yusuf writes about how EA countries can respond to these challenges with the use of strategic long-range planning, technological advances, broader implementation capacity, and better resource mobilization. With that, he draws larger inferences that can guide policymakers in tackling the challenges of urbanization elsewhere.

Source: Centre for Global Development

For the many urbanized and rapidly urbanizing countries, the East Asian experience with and response to emerging challenges is a model to look up to. As high-income East Asian economies approach peaking urbanization, they are now plagued with several challenges. From service sector and export-led growth outstripping manufacturing to rising carbon levels in cities, aging populations, and infrastructure that struggles to catch up with advances in technology- the concerns are aplenty.

Posted by at 10:37 AM

Labels: Inclusive Growth

Globalization and Factor Income Taxation

From a NBER paper by Pierre Bachas, Matthew H. Fisher-Post, Anders Jensen and Gabriel Zucman:

“How has globalization affected the relative taxation of labor and capital, and why? To address this question we build and analyze a new database of effective macroeconomic tax rates covering 150 countries since 1965, constructed by combining national accounts data with government revenue statistics. We obtain four main findings: (1) The effective tax rates on labor and capital converged globally since the 1960s, due to a 10 percentage-point increase in labor taxation and a 5 percentage-point decline in capital taxation. (2) The decline in capital taxation is concentrated in high-income countries. By contrast, capital taxation increased in developing countries since the 1990s, albeit from a low base. (3) Consistently across a variety of research designs, we find that the rise in capital taxation in developing countries can be explained by a tax-capacity effect of international trade: Trade openness leads to a concentration of economic activity in formal corporate structures, where capital taxes are easier to impose. (4) At the same time, international economic integration reduces statutory tax rates, due to increased tax competition. In high-income countries, this negative tax competition effect of trade has dominated, while in developing countries the positive tax-capacity effect of international trade appears to have prevailed.”

From a NBER paper by Pierre Bachas, Matthew H. Fisher-Post, Anders Jensen and Gabriel Zucman:

“How has globalization affected the relative taxation of labor and capital, and why? To address this question we build and analyze a new database of effective macroeconomic tax rates covering 150 countries since 1965, constructed by combining national accounts data with government revenue statistics. We obtain four main findings: (1) The effective tax rates on labor and capital converged globally since the 1960s,

Posted by at 7:04 AM

Labels: Macro Demystified

Friday, March 4, 2022

Short in Supply!

Source: Project Syndicate

In a recent column, John H. Cochrane of the Hoover Institution and Jon Hartley of Foundation for Research on Equal Opportunity write about the US’ long-ignored issue of supply-chain bottlenecks contributing to raging inflation today.

“The return of inflation is an economic cold shower”

They write how sclerotic growth in the country is not so much due to the “secular stagnation” of demand-side factors, but more due to clogging of the economy’s productive capacity. “The United States needs infrastructure. The problem is not money. The problem is that building anything in America has become almost impossible, owing to the thicket of regulations and lawsuits that will stop or drive up the costs of any project.” Barriers such as rocketing housing costs, deteriorating quality of public education, restrictive labor laws, trade protectionism, and other things all add to the problem. The authors also discuss some solutions to systematically eliminate such challenges.

Source: Project Syndicate

In a recent column, John H. Cochrane of the Hoover Institution and Jon Hartley of Foundation for Research on Equal Opportunity write about the US’ long-ignored issue of supply-chain bottlenecks contributing to raging inflation today.

“The return of inflation is an economic cold shower”

They write how sclerotic growth in the country is not so much due to the “secular stagnation” of demand-side factors,

Posted by at 10:32 AM

Labels: Inclusive Growth, Macro Demystified

Subscribe to: Posts